Vous aimerez peut-être aussi

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

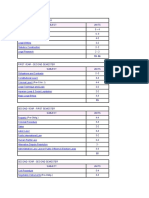

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- BLR 211 - FdeDocument23 pagesBLR 211 - FdeDjunah Arellano100% (1)

- Quo WarrantoDocument15 pagesQuo WarrantoRessie June PedranoPas encore d'évaluation

- Incompatible and Forbidden Offices and Restrictions On Other Offices and Officer of The GovernmentDocument10 pagesIncompatible and Forbidden Offices and Restrictions On Other Offices and Officer of The GovernmentRaff GonzalesPas encore d'évaluation

- Art. III, Sec. 5-8 Case Digest CompilationDocument7 pagesArt. III, Sec. 5-8 Case Digest Compilationrjpogikaayo100% (1)

- 207611-2017-Manggagawa NG Komunikasyon Sa Pilipinas v.20170615-911-1g498x0 PDFDocument18 pages207611-2017-Manggagawa NG Komunikasyon Sa Pilipinas v.20170615-911-1g498x0 PDFIsabella GamuloPas encore d'évaluation

- What Is Artificial Intelligence and Why Does It Matter For: 4ip Council Research Award Winner 2018Document17 pagesWhat Is Artificial Intelligence and Why Does It Matter For: 4ip Council Research Award Winner 2018Ana Maria RusuPas encore d'évaluation

- CV Divya PandeyDocument1 pageCV Divya PandeydivyaPas encore d'évaluation

- A Party Must Be Ready To Submit Evidence Upon Filing of The Complaint or AnswerDocument8 pagesA Party Must Be Ready To Submit Evidence Upon Filing of The Complaint or AnswerMay Conde AguilarPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- 5 6179095781476139217Document240 pages5 6179095781476139217Ãã Kā ShPas encore d'évaluation

- Notes On Accountability of Public OfficersDocument8 pagesNotes On Accountability of Public OfficersGeelleanne L UbaldePas encore d'évaluation

- Maritime Transport Security (Kenneth)Document26 pagesMaritime Transport Security (Kenneth)manohar killiPas encore d'évaluation

- Confirmation For Booking ID # 676714400Document1 pageConfirmation For Booking ID # 676714400dante arcigalPas encore d'évaluation

- Sta. Rosa - Certification - Senior CitizenDocument1 pageSta. Rosa - Certification - Senior CitizenJohny VillanuevaPas encore d'évaluation

- HRL CH11 ImplementationDocument86 pagesHRL CH11 ImplementationJonathan Ivan OroPas encore d'évaluation

- ArellanoDocument3 pagesArellanoSusie VanguardiaPas encore d'évaluation

- BLP-Transactions (Contracts) - Types and FormsDocument28 pagesBLP-Transactions (Contracts) - Types and FormsaiteginPas encore d'évaluation

- Historical Origin of HRDocument6 pagesHistorical Origin of HRA2 Sir Fan PagePas encore d'évaluation

- Full Download Elements of Ecology 8th Edition Smith Test BankDocument35 pagesFull Download Elements of Ecology 8th Edition Smith Test Bankschmitzerallanafx100% (35)

- Drugs and Alcohol EssayDocument5 pagesDrugs and Alcohol Essayolylmqaeg100% (1)

- CASE DIGEST TOBI - CASE DIGEST - Pamil Vs TeleronDocument2 pagesCASE DIGEST TOBI - CASE DIGEST - Pamil Vs Teleronrunish venganzaPas encore d'évaluation

- W.P (C) - No. 8090 & 5956 2006 Reliance PDFDocument38 pagesW.P (C) - No. 8090 & 5956 2006 Reliance PDFakloihassnPas encore d'évaluation

- EC - 2019 A Different Kind of Formal Bottom-Up State-Making in Small-Scale Gold Mining Regions in Chocó, ColombiaDocument11 pagesEC - 2019 A Different Kind of Formal Bottom-Up State-Making in Small-Scale Gold Mining Regions in Chocó, ColombiaAna PaulaPas encore d'évaluation

- Inter-State RelationsDocument9 pagesInter-State RelationsVanam TejasviPas encore d'évaluation

- Aggabao V ParulanDocument8 pagesAggabao V ParulanArnaldo DomingoPas encore d'évaluation

- 24th May Train TicketDocument3 pages24th May Train TicketRahul DeshpandePas encore d'évaluation

- Delegation Financial PowersDocument8 pagesDelegation Financial PowersPRASHANT RAWALPas encore d'évaluation

- Criminal Procedure and Court Testimony: Study Guide No. 6Document6 pagesCriminal Procedure and Court Testimony: Study Guide No. 6Kasumi AlbaPas encore d'évaluation

- University of New Mexico Divestment ComplaintDocument63 pagesUniversity of New Mexico Divestment ComplaintAlbuquerque JournalPas encore d'évaluation

- S A. F P: Ienna Lores RopertyDocument5 pagesS A. F P: Ienna Lores RopertyMedj Broke Law StudentPas encore d'évaluation

- INZ 1020 - Application For Variation of Conditions (INZ 1020)Document9 pagesINZ 1020 - Application For Variation of Conditions (INZ 1020)Dragoslav Dzolic0% (1)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)D'EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Évaluation : 4.5 sur 5 étoiles4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)D'EverandFinance Basics (HBR 20-Minute Manager Series)Évaluation : 4.5 sur 5 étoiles4.5/5 (32)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindD'EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindÉvaluation : 5 sur 5 étoiles5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)D'EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (13)

- Getting to Yes: How to Negotiate Agreement Without Giving InD'EverandGetting to Yes: How to Negotiate Agreement Without Giving InÉvaluation : 4 sur 5 étoiles4/5 (652)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantD'EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantÉvaluation : 4.5 sur 5 étoiles4.5/5 (146)