Vous aimerez peut-être aussi

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSPas encore d'évaluation

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Capili vs. PeopleDocument11 pagesCapili vs. PeopleIñigo Mathay RojasPas encore d'évaluation

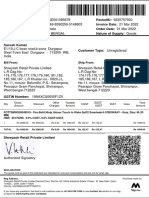

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountIndrajit RanaPas encore d'évaluation

- RemediesDocument45 pagesRemediesCzarina100% (1)

- Fernan JR Vs People G.R No. 145927Document1 pageFernan JR Vs People G.R No. 145927EJ SantosPas encore d'évaluation

- Reasonable Restrictions Under Article 19Document20 pagesReasonable Restrictions Under Article 19ROHITGAURAVCNLUPas encore d'évaluation

- 24 Francisco v. TRB, SupraDocument4 pages24 Francisco v. TRB, SupraJul A.Pas encore d'évaluation

- D.D.C. 16-cv-01460 DCKT 000216 - 000 Filed 2020-08-24Document36 pagesD.D.C. 16-cv-01460 DCKT 000216 - 000 Filed 2020-08-24charlie minatoPas encore d'évaluation

- Ethics in Re. SottoDocument1 pageEthics in Re. SottoLayla-Tal Medina100% (2)

- Case Folder For Falsification of DocumentsDocument8 pagesCase Folder For Falsification of Documentsjanecil bonzaPas encore d'évaluation

- COMELEC Resolution No. 9523Document9 pagesCOMELEC Resolution No. 9523Karlo Dialogo100% (3)

- Proceedings of The District Educational Officer, Anantapur Present: Sri V.Premanandam, M.A., M.Ed.Document1 pageProceedings of The District Educational Officer, Anantapur Present: Sri V.Premanandam, M.A., M.Ed.Chaitanya KumarPas encore d'évaluation

- MC 01Document2 pagesMC 01dndkonigPas encore d'évaluation

- RTI Sec4 (1) (B) CS SectionDocument251 pagesRTI Sec4 (1) (B) CS SectionSANTHOSH KUMAR T MPas encore d'évaluation

- Karnataka Employers' AssociationDocument4 pagesKarnataka Employers' Associationmajor raveendraPas encore d'évaluation

- Republic v. YuDocument4 pagesRepublic v. YuAira Marie M. AndalPas encore d'évaluation

- Daniel-Criminal Law Review DigestDocument88 pagesDaniel-Criminal Law Review Digestdaniel besina jrPas encore d'évaluation

- Precedential: Circuit JudgesDocument44 pagesPrecedential: Circuit JudgesScribd Government DocsPas encore d'évaluation

- Aman Deep Sharan BA0170006Document2 pagesAman Deep Sharan BA0170006Aman D SharanPas encore d'évaluation

- (1.) People of The Philippines Vs Lambid (Digest)Document2 pages(1.) People of The Philippines Vs Lambid (Digest)Obin Tambasacan Baggayan100% (1)

- For NBW Cancellation Presence of Accused Not Required Before MagistrateDocument5 pagesFor NBW Cancellation Presence of Accused Not Required Before MagistrateapndesaiPas encore d'évaluation

- Constitutional Law II Reviewer (Part 2)Document9 pagesConstitutional Law II Reviewer (Part 2)Shasharu Fei-fei LimPas encore d'évaluation

- Proof That The Congressional Research Service Is NotDocument8 pagesProof That The Congressional Research Service Is Notmivo68Pas encore d'évaluation

- Torts OutlineDocument79 pagesTorts OutlineJanay Clougherty100% (1)

- Zuffa's Motion For Attorney Fees and CostsDocument10 pagesZuffa's Motion For Attorney Fees and CostsMMA Payout100% (1)

- Legal Profession Group Assignment September 3 2019Document6 pagesLegal Profession Group Assignment September 3 2019Marco RenaciaPas encore d'évaluation

- Booking 03 11Document2 pagesBooking 03 11Bryan FitzgeraldPas encore d'évaluation

- Pioneer Concrete Philippines Inc Vs TodaroDocument3 pagesPioneer Concrete Philippines Inc Vs TodaroRochelle Othin Odsinada MarquesesPas encore d'évaluation

- FACTS: Benito and Private Respondent Pagayawan Were 2 of 8 Candidates Vying For TheDocument2 pagesFACTS: Benito and Private Respondent Pagayawan Were 2 of 8 Candidates Vying For TheCharles Roger RayaPas encore d'évaluation

- A2025 (CRIMPRO) (Preliminary Investigation) - Mina v. Court of Appeals, January 18, 2019Document2 pagesA2025 (CRIMPRO) (Preliminary Investigation) - Mina v. Court of Appeals, January 18, 2019Karina Bette RuizPas encore d'évaluation

- Intro To Torts CH 18Document24 pagesIntro To Torts CH 18api-264755370Pas encore d'évaluation