Vous aimerez peut-être aussi

- CH 07Document104 pagesCH 07ranniaPas encore d'évaluation

- Corporate Financial Analysis with Microsoft ExcelD'EverandCorporate Financial Analysis with Microsoft ExcelÉvaluation : 5 sur 5 étoiles5/5 (1)

- Practice Transfer Pricing ExamplesDocument4 pagesPractice Transfer Pricing ExamplesHashmi Sutariya100% (1)

- Brief Exercises CHAPTER 7Document3 pagesBrief Exercises CHAPTER 7Trang LePas encore d'évaluation

- Revenue RecognitionDocument16 pagesRevenue Recognitionzee abadilla100% (1)

- CH 18-Revenue Recognition - KiesoDocument41 pagesCH 18-Revenue Recognition - Kiesofransiskawidya100% (1)

- CH 18 20 AKMDocument121 pagesCH 18 20 AKMDewanto Kusumo100% (1)

- CH16Document80 pagesCH16mahinPas encore d'évaluation

- Case 1 Dan Case 2 Job Order CostingDocument6 pagesCase 1 Dan Case 2 Job Order CostingChantika JustiaraPas encore d'évaluation

- FAR and AFAR Revenue Recognition IFRS 15Document121 pagesFAR and AFAR Revenue Recognition IFRS 15Craig Julian50% (2)

- Audit Chapter SolutionsDocument3 pagesAudit Chapter SolutionsJana WrightPas encore d'évaluation

- Goliath Transfer Pricing Case ArticleDocument13 pagesGoliath Transfer Pricing Case ArticleFridRachmanPas encore d'évaluation

- ADV ACC TBch04Document21 pagesADV ACC TBch04hassan nassereddine100% (2)

- Intercompany Inventory Transactions: Mcgraw-Hill/IrwinDocument123 pagesIntercompany Inventory Transactions: Mcgraw-Hill/IrwinsresaPas encore d'évaluation

- Rais12 SM ch13Document32 pagesRais12 SM ch13Edwin MayPas encore d'évaluation

- Desktop Solution IncDocument6 pagesDesktop Solution IncAmira Nur Afiqah Agus Salim0% (1)

- ch04 PDFDocument52 pagesch04 PDFerylpaez69% (13)

- SIA - Soal Dan JawabanDocument7 pagesSIA - Soal Dan JawabanRano Kardo SinambelaPas encore d'évaluation

- Accounts Payable ConceptsDocument3 pagesAccounts Payable ConceptsVAIBHAV PARABPas encore d'évaluation

- Revenue RecognitionDocument110 pagesRevenue Recognition586456021Pas encore d'évaluation

- Financial Planning and Analysis: The Master BudgetDocument57 pagesFinancial Planning and Analysis: The Master BudgetBig D100% (2)

- Body EmailDocument2 pagesBody Emailferry firmannaPas encore d'évaluation

- Question and Answer - 37Document31 pagesQuestion and Answer - 37acc-expert0% (1)

- Unit 12 Responsibility Accounting and Performance MeasuresDocument16 pagesUnit 12 Responsibility Accounting and Performance Measuresestihdaf استهدافPas encore d'évaluation

- Role of Financial Management in OrganizationDocument8 pagesRole of Financial Management in OrganizationTasbeha SalehjeePas encore d'évaluation

- CH 06Document50 pagesCH 06Dr-Bahaaeddin Alareeni100% (1)

- Bab 6 Intercompany Profit TransactionsDocument2 pagesBab 6 Intercompany Profit TransactionsAnonymous dMkY9G2Pas encore d'évaluation

- Unilever Revenue CycleDocument14 pagesUnilever Revenue CycleShinta Risandi100% (4)

- Accounting and Reporting For Foreign Currencies and Translation of Foreign Currency Financial Statements PDFDocument33 pagesAccounting and Reporting For Foreign Currencies and Translation of Foreign Currency Financial Statements PDFMeselech GirmaPas encore d'évaluation

- Ch04 Consolidation TechniquesDocument54 pagesCh04 Consolidation TechniquesRizqita Putri Ramadhani0% (1)

- Chapter 4Document16 pagesChapter 4Girma NegashPas encore d'évaluation

- DFD Dub 5Document2 pagesDFD Dub 5Niken Ayu PermandaraniPas encore d'évaluation

- Ch01 Introduction To Business Combinations and The Conceptual FrameworkDocument51 pagesCh01 Introduction To Business Combinations and The Conceptual Frameworkmariko1234100% (1)

- On January 1 2014 Palmer Company Acquired A 90 InterestDocument1 pageOn January 1 2014 Palmer Company Acquired A 90 InterestCharlottePas encore d'évaluation

- TB Ch12Document36 pagesTB Ch12AhmadYaseenPas encore d'évaluation

- Tugas 5 (Kelompok 5)Document9 pagesTugas 5 (Kelompok 5)Silviana Ika Susanti67% (3)

- Business Vision and MissionDocument18 pagesBusiness Vision and Missionria ainun rozikaPas encore d'évaluation

- Cost-Volume-Profit Analysis: A Managerial Planning Tool: Discussion QuestionsDocument41 pagesCost-Volume-Profit Analysis: A Managerial Planning Tool: Discussion Questionshoodron22100% (1)

- Consignments Ch6 DrebbinDocument12 pagesConsignments Ch6 DrebbinindahmuliasariPas encore d'évaluation

- Chap 11 SolutionsDocument6 pagesChap 11 SolutionsMiftahudin Miftahudin100% (2)

- Tutorial 1 (For Student)Document2 pagesTutorial 1 (For Student)dee davyanPas encore d'évaluation

- Chapter 7 Problem 7.3 Nathali, Jeffrey, TasyaDocument6 pagesChapter 7 Problem 7.3 Nathali, Jeffrey, Tasyavtech netPas encore d'évaluation

- Tugas Variable Costing and The Measurement of ESG and Quality Costs (Irga Ayudias Tantri - 120301214100011)Document2 pagesTugas Variable Costing and The Measurement of ESG and Quality Costs (Irga Ayudias Tantri - 120301214100011)irga ayudias0% (1)

- Sujit 1-134-380 PDFDocument247 pagesSujit 1-134-380 PDFŞâh ŠůmiťPas encore d'évaluation

- Bookoff Case AnalysisDocument7 pagesBookoff Case AnalysisLeo SanjayaPas encore d'évaluation

- Accounting For Derivatives and Hedging Activities: Answers To QuestionsDocument22 pagesAccounting For Derivatives and Hedging Activities: Answers To QuestionsGabyVionidyaPas encore d'évaluation

- Akl 1-5Document5 pagesAkl 1-5Eka Resti Kinasih100% (1)

- Beams Aa13e PPT 13Document36 pagesBeams Aa13e PPT 13ki100% (1)

- Tugas 5 - AKL 1Document3 pagesTugas 5 - AKL 1Geroro D'PhoenixPas encore d'évaluation

- Working 3Document6 pagesWorking 3Hà Lê DuyPas encore d'évaluation

- Patricia Eklund's participative budgeting proceduresDocument11 pagesPatricia Eklund's participative budgeting proceduresirga ayudiasPas encore d'évaluation

- Mund Manufacturing Inc Started Operations at The Beginning of TheDocument1 pageMund Manufacturing Inc Started Operations at The Beginning of TheLet's Talk With HassanPas encore d'évaluation

- Audit of Liabilities: Audit Program For Accounts Payable Audit ObjectivesDocument18 pagesAudit of Liabilities: Audit Program For Accounts Payable Audit ObjectivesSarah PuspawatiPas encore d'évaluation

- KASUS KECURANGAN MCKESSON & ROBBINS DAN ZZZ BEST COMPANYDocument34 pagesKASUS KECURANGAN MCKESSON & ROBBINS DAN ZZZ BEST COMPANYreynaldiePas encore d'évaluation

- Advanced Accounting Chapter 16Document3 pagesAdvanced Accounting Chapter 16sutan fanandiPas encore d'évaluation

- Chapter 19, Modern Advanced Accounting-Review Q & ExrDocument17 pagesChapter 19, Modern Advanced Accounting-Review Q & Exrrlg4814100% (2)

- Contoh Eliminasi Lap - Keu KonsolidasiDocument44 pagesContoh Eliminasi Lap - Keu KonsolidasiLuki DewayaniPas encore d'évaluation

- Long-Term Construction Contract Revenue RecognitionDocument7 pagesLong-Term Construction Contract Revenue RecognitionGab IgnacioPas encore d'évaluation

- Miljane Perdizo - Quiz 2Document2 pagesMiljane Perdizo - Quiz 2Miljane PerdizoPas encore d'évaluation

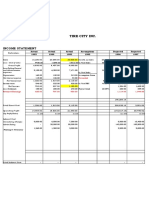

- Tire City IncDocument18 pagesTire City IncSoumyajitPas encore d'évaluation

- Acct4290 (IT Audit) - Final Exam ReviewDocument23 pagesAcct4290 (IT Audit) - Final Exam ReviewRaquel VandermeulenPas encore d'évaluation

- Intacc Review Questions Micha 1Document3 pagesIntacc Review Questions Micha 1Christian ContadorPas encore d'évaluation

- Bookkeeping questions on accounts receivable, payable and net salesDocument2 pagesBookkeeping questions on accounts receivable, payable and net salesRural Bank CauayanPas encore d'évaluation

- Cash and Cash EquivalentDocument2 pagesCash and Cash EquivalentJovani Laña100% (1)

- Chapter 10Document35 pagesChapter 10Joanna GarciaPas encore d'évaluation

- Merchant Banking Roles and FunctionsDocument18 pagesMerchant Banking Roles and Functionssunita prabhakarPas encore d'évaluation

- This Study Resource Was: AnswerDocument6 pagesThis Study Resource Was: AnswerKen SannPas encore d'évaluation

- Audit of Accounts Receivable and Related Accounts ComDocument3 pagesAudit of Accounts Receivable and Related Accounts ComCJ alandyPas encore d'évaluation

- 03 Financial AnalysisDocument55 pages03 Financial Analysisselcen sarıkayaPas encore d'évaluation

- Unit II Lesson 5 and 6 ADJUSTING ENTRIES and FSDocument25 pagesUnit II Lesson 5 and 6 ADJUSTING ENTRIES and FSAlezandra SantelicesPas encore d'évaluation

- Bac MQ2 1Document3 pagesBac MQ2 1JESSON VILLAPas encore d'évaluation

- AUD02 - 03 Cash and Accrual BasisDocument16 pagesAUD02 - 03 Cash and Accrual BasisMark BajacanPas encore d'évaluation

- Simulates Midterm Exam. IntAcc1 PDFDocument11 pagesSimulates Midterm Exam. IntAcc1 PDFA NuelaPas encore d'évaluation

- Accounting: For AllDocument673 pagesAccounting: For AllSimphiwe NandoPas encore d'évaluation

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaKyrie Gwynette OlarvePas encore d'évaluation

- Boxsoft Super Quickbooks-Export TemplatesDocument64 pagesBoxsoft Super Quickbooks-Export Templateszpoturica569Pas encore d'évaluation

- Wed-FABM2-Fundamentals of Accountancy Business Management 2-ABM-LoveDocument3 pagesWed-FABM2-Fundamentals of Accountancy Business Management 2-ABM-LoveAdoree Ramos100% (1)

- Prac1: Multiple ChoiceDocument9 pagesPrac1: Multiple ChoiceROMAR A. PIGAPas encore d'évaluation

- Chapter 3 - Income Flows VerDocument30 pagesChapter 3 - Income Flows Ver3bazoPas encore d'évaluation

- Receivables QuizDocument3 pagesReceivables QuizAshianna KimPas encore d'évaluation

- Accounting For Receivables: Learning ObjectivesDocument63 pagesAccounting For Receivables: Learning ObjectivesBayaderPas encore d'évaluation

- Merchandising Operations Income StatementDocument8 pagesMerchandising Operations Income StatementMondy MondyPas encore d'évaluation

- Module 3 - EA03Document30 pagesModule 3 - EA03Vaseline QtipsPas encore d'évaluation

- Partnership Liquidation Chapter 4 QuizDocument3 pagesPartnership Liquidation Chapter 4 QuizKimberly Quin CañasPas encore d'évaluation

- Business Finance Introduction To Financial Management 07Document41 pagesBusiness Finance Introduction To Financial Management 07Melvin J. ReyesPas encore d'évaluation

- Kunci PT Adijaya-Paket 1Document9 pagesKunci PT Adijaya-Paket 1nasrulloh_spd100% (4)

- Accounting 18Document7 pagesAccounting 18Kenshin HayashiPas encore d'évaluation

- ACCO 3150 Tarea 1.1Document4 pagesACCO 3150 Tarea 1.1Mirelis QuiñonesPas encore d'évaluation

- Chapter 1: Cash Manager OverviewDocument10 pagesChapter 1: Cash Manager Overviewparrae22Pas encore d'évaluation

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)D'EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (12)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindD'EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindÉvaluation : 5 sur 5 étoiles5/5 (231)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantD'EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantÉvaluation : 4.5 sur 5 étoiles4.5/5 (146)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetD'EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetPas encore d'évaluation

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)D'EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Évaluation : 4.5 sur 5 étoiles4.5/5 (5)

- Joy of Agility: How to Solve Problems and Succeed SoonerD'EverandJoy of Agility: How to Solve Problems and Succeed SoonerÉvaluation : 4 sur 5 étoiles4/5 (1)

- Profit First for Therapists: A Simple Framework for Financial FreedomD'EverandProfit First for Therapists: A Simple Framework for Financial FreedomPas encore d'évaluation

- Financial Accounting For Dummies: 2nd EditionD'EverandFinancial Accounting For Dummies: 2nd EditionÉvaluation : 5 sur 5 étoiles5/5 (10)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistD'EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistÉvaluation : 4.5 sur 5 étoiles4.5/5 (73)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesD'EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesPas encore d'évaluation

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!D'EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Évaluation : 4.5 sur 5 étoiles4.5/5 (14)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItD'EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItÉvaluation : 5 sur 5 étoiles5/5 (13)

- Finance Basics (HBR 20-Minute Manager Series)D'EverandFinance Basics (HBR 20-Minute Manager Series)Évaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanD'EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanÉvaluation : 4.5 sur 5 étoiles4.5/5 (79)

- Value: The Four Cornerstones of Corporate FinanceD'EverandValue: The Four Cornerstones of Corporate FinanceÉvaluation : 4.5 sur 5 étoiles4.5/5 (18)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisD'EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisÉvaluation : 5 sur 5 étoiles5/5 (6)

- Basic Accounting: Service Business Study GuideD'EverandBasic Accounting: Service Business Study GuideÉvaluation : 5 sur 5 étoiles5/5 (2)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?D'EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Évaluation : 5 sur 5 étoiles5/5 (1)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyD'EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyÉvaluation : 5 sur 5 étoiles5/5 (1)

- Product-Led Growth: How to Build a Product That Sells ItselfD'EverandProduct-Led Growth: How to Build a Product That Sells ItselfÉvaluation : 5 sur 5 étoiles5/5 (1)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesD'EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesÉvaluation : 4.5 sur 5 étoiles4.5/5 (30)