Vous aimerez peut-être aussi

- Buhlmann Credibility Homework SolutionsDocument11 pagesBuhlmann Credibility Homework Solutionschitechi sarah zakiaPas encore d'évaluation

- Practice 2Document4 pagesPractice 2bo chian chynPas encore d'évaluation

- Self-test 5 FN 211 matrices and regressionsDocument5 pagesSelf-test 5 FN 211 matrices and regressionsRaiNz SeasonPas encore d'évaluation

- Lecturer Name: MR Moyo: Radreck U. Maenzanise 01182038512Document4 pagesLecturer Name: MR Moyo: Radreck U. Maenzanise 01182038512Morris AloqrothPas encore d'évaluation

- Chapter 6 - Problem Solving (Risk)Document5 pagesChapter 6 - Problem Solving (Risk)Shresth KotishPas encore d'évaluation

- Chapter 7Document3 pagesChapter 7YINN YEE TANPas encore d'évaluation

- Summarizing Data - Statistical HydrologyDocument6 pagesSummarizing Data - Statistical HydrologyJavier Avila100% (1)

- Problem Set 1 SolutionsDocument32 pagesProblem Set 1 Solutionsale.ili.pauPas encore d'évaluation

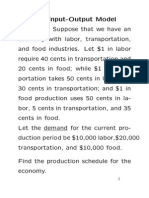

- Leontief 1Document24 pagesLeontief 1Tara BhusalPas encore d'évaluation

- ISOM 2500 Fa21 - Quiz - 2 - Ch8-Ch12 - SolDocument15 pagesISOM 2500 Fa21 - Quiz - 2 - Ch8-Ch12 - Solyantelau.Pas encore d'évaluation

- Standard Deviation on Individual Security = σ = √σ: Risk Return Problems Problem 1Document3 pagesStandard Deviation on Individual Security = σ = √σ: Risk Return Problems Problem 1jakia yasminPas encore d'évaluation

- Quiz 7Document3 pagesQuiz 7朱潇妤Pas encore d'évaluation

- Chapter Eight End of Chapter Useful Questions and SolutionsDocument18 pagesChapter Eight End of Chapter Useful Questions and SolutionsAbhinav AgarwalPas encore d'évaluation

- RTA HeterocDocument4 pagesRTA HeterocJaime Andres Chica PPas encore d'évaluation

- Business Statistics Topic 3 Tutorial Solutions (Q1-Q10)Document4 pagesBusiness Statistics Topic 3 Tutorial Solutions (Q1-Q10)Beryl ChanPas encore d'évaluation

- ANSWERS Expected Return and Standard Deviation For Individual Stocks and PortfoliosDocument3 pagesANSWERS Expected Return and Standard Deviation For Individual Stocks and PortfoliosKashifPas encore d'évaluation

- Decision ScienceDocument8 pagesDecision ScienceHimanshi YadavPas encore d'évaluation

- Analyzing correlation and regression of family expenditure dataDocument8 pagesAnalyzing correlation and regression of family expenditure dataNguyễn Tuấn AnhPas encore d'évaluation

- Research AssignmentDocument8 pagesResearch AssignmentAbdusalam IdirisPas encore d'évaluation

- FINM2003 - Mid Semester Exam Sem 1 2015 (Suggested Solutions)Document6 pagesFINM2003 - Mid Semester Exam Sem 1 2015 (Suggested Solutions)JasonPas encore d'évaluation

- Solution To Chapter 11 Assigned ProblemsDocument4 pagesSolution To Chapter 11 Assigned ProblemsBombitaPas encore d'évaluation

- Random Variables GuideDocument12 pagesRandom Variables Guidei am the greatest1Pas encore d'évaluation

- Stock Analysis and Portfolio DecisionsDocument5 pagesStock Analysis and Portfolio DecisionsPro TenPas encore d'évaluation

- LAB1 PhamTanThang s3635005Document7 pagesLAB1 PhamTanThang s3635005Terry PhamPas encore d'évaluation

- Tutorial - Investment and Financial AnalysisDocument40 pagesTutorial - Investment and Financial AnalysiskelvinplayzgamesPas encore d'évaluation

- CVG2181 Assignment 1 George&AbdullaDocument5 pagesCVG2181 Assignment 1 George&Abdullatajiw17001Pas encore d'évaluation

- Practice Question - Chaptr 4Document8 pagesPractice Question - Chaptr 4Pro TenPas encore d'évaluation

- Calculating portfolio beta, variance, standard deviation and expected returnsDocument5 pagesCalculating portfolio beta, variance, standard deviation and expected returnsManuel BoahenPas encore d'évaluation

- SFE1.4.2 - UDJ - (SOL) Exam of Mar 2013, For Practice - SOLUTIONSDocument2 pagesSFE1.4.2 - UDJ - (SOL) Exam of Mar 2013, For Practice - SOLUTIONSGonçalo RibeiroPas encore d'évaluation

- AEM 3e Chapter 06Document6 pagesAEM 3e Chapter 06AKIN ERENPas encore d'évaluation

- Mean, Variance, Standard DeviationDocument3 pagesMean, Variance, Standard DeviationCielo DimayugaPas encore d'évaluation

- Statistics and Probability Module 2Document3 pagesStatistics and Probability Module 2Cielo DimayugaPas encore d'évaluation

- UntitledDocument6 pagesUntitlednawalPas encore d'évaluation

- Quantitative Risk Management: CourseworkDocument14 pagesQuantitative Risk Management: CourseworkMichaelWongPas encore d'évaluation

- Lab Report 03 - Edm CalibrationDocument2 pagesLab Report 03 - Edm CalibrationShivam ShuklaPas encore d'évaluation

- Risk and Return A - SolutionsDocument3 pagesRisk and Return A - SolutionsmilotikyuPas encore d'évaluation

- Report 12 InstrumentalDocument3 pagesReport 12 InstrumentalKim Yến PhùngPas encore d'évaluation

- EES 404Document10 pagesEES 404beemuriithi24Pas encore d'évaluation

- Econometrics 2013 MidtermDocument9 pagesEconometrics 2013 MidtermreddrosePas encore d'évaluation

- ISOM2500Practice - Quiz 2 SolDocument5 pagesISOM2500Practice - Quiz 2 SoljayceeshuiPas encore d'évaluation

- Introduction:-: Graph#1: Showing The Relation Between The Average Heights The Bounce NumberDocument3 pagesIntroduction:-: Graph#1: Showing The Relation Between The Average Heights The Bounce Numberb76xxn4rdjPas encore d'évaluation

- DETERMINE THICKNESS OF MICA SHEET USING INTERFERENCE FRINGESDocument5 pagesDETERMINE THICKNESS OF MICA SHEET USING INTERFERENCE FRINGESSagar Rawal100% (1)

- Name:Emmanuel Morgan Tembo NUMBER:201702046 Program:Accounting and Finance Course:Financial Management and Risk AppraisalDocument11 pagesName:Emmanuel Morgan Tembo NUMBER:201702046 Program:Accounting and Finance Course:Financial Management and Risk AppraisalEmmanuel Ēzscod TemboPas encore d'évaluation

- Calculate Expected Returns and Standard Deviation of Investment PortfoliosDocument4 pagesCalculate Expected Returns and Standard Deviation of Investment PortfoliosKashifPas encore d'évaluation

- Portfolio QuestionsDocument3 pagesPortfolio QuestionsMeshack MatePas encore d'évaluation

- Course3 1100Document69 pagesCourse3 1100Camila Andrea Sarmiento BetancourtPas encore d'évaluation

- Midterm Exam Investments May 2010 InstructionsDocument5 pagesMidterm Exam Investments May 2010 Instructions张逸Pas encore d'évaluation

- Time Series Analysis and ForecastingDocument5 pagesTime Series Analysis and ForecastingMusa KhanPas encore d'évaluation

- W2 II C12 Systematic Risk and Equity Risk PremiumDocument12 pagesW2 II C12 Systematic Risk and Equity Risk PremiumSophie LimPas encore d'évaluation

- Calculations TFP260S AssignmentDocument5 pagesCalculations TFP260S AssignmentKelly AbrahamsPas encore d'évaluation

- Report Moment Influence LinesDocument30 pagesReport Moment Influence LinesismailPas encore d'évaluation

- Introduction to Risk, Return, and The Opportunity Cost of Capital Answers to Practice QuestionsDocument9 pagesIntroduction to Risk, Return, and The Opportunity Cost of Capital Answers to Practice QuestionsShireen QaiserPas encore d'évaluation

- Practice 3 Multiple Regression 2023 03-16-09!06!38Document5 pagesPractice 3 Multiple Regression 2023 03-16-09!06!38PavonisPas encore d'évaluation

- Momento CurvaturaDocument7 pagesMomento Curvaturaarmando.garciaPas encore d'évaluation

- Practice 1Document3 pagesPractice 1bo chian chynPas encore d'évaluation

- Assignment On Chapter 11Document3 pagesAssignment On Chapter 11SarveshSailPas encore d'évaluation

- Lab 6 ResultDocument2 pagesLab 6 Result立敬Pas encore d'évaluation

- From The Table D4 1.777 and D3 0.233: Answer: AnswerDocument2 pagesFrom The Table D4 1.777 and D3 0.233: Answer: Answernada abdelrahmanPas encore d'évaluation

- Hw5 Mfe Au14 SolutionDocument8 pagesHw5 Mfe Au14 SolutionWenn Zhang100% (2)

- Digital Electronics For Engineering and Diploma CoursesD'EverandDigital Electronics For Engineering and Diploma CoursesPas encore d'évaluation

- wk3 PDFDocument25 pageswk3 PDFrodmagatPas encore d'évaluation

- Account Statement: MR - Shyamal Kumar ChatterjeeDocument2 pagesAccount Statement: MR - Shyamal Kumar ChatterjeeBikram ChatterjeePas encore d'évaluation

- Yes Bank 2004-05Document133 pagesYes Bank 2004-05Sagar ShawPas encore d'évaluation

- MCS-Responsibility Centres & Profit CentresDocument24 pagesMCS-Responsibility Centres & Profit CentresAnand KansalPas encore d'évaluation

- Capital Gains Tax (CGT) RatesDocument15 pagesCapital Gains Tax (CGT) RatesMargaretha PaulinaPas encore d'évaluation

- Excel Solutions - CasesDocument25 pagesExcel Solutions - CasesJerry Ramos CasanaPas encore d'évaluation

- Wipro Consolidated Balance SheetDocument2 pagesWipro Consolidated Balance SheetKarthik KarthikPas encore d'évaluation

- Pag-IBIG Fund Public Auction Properties in Cavite, Laguna, Bulacan & Metro ManilaDocument24 pagesPag-IBIG Fund Public Auction Properties in Cavite, Laguna, Bulacan & Metro ManilaSilvino CatipanPas encore d'évaluation

- Chapter 3.auditing Princples and Tools RevDocument122 pagesChapter 3.auditing Princples and Tools RevyebegashetPas encore d'évaluation

- Kuwait's Flag and Its Historical MeaningsDocument10 pagesKuwait's Flag and Its Historical Meaningsrichmond magantePas encore d'évaluation

- Soft Offer Iron Ore 64.5Document3 pagesSoft Offer Iron Ore 64.5BernhardPas encore d'évaluation

- Bclte Part 2Document141 pagesBclte Part 2Jennylyn Favila Magdadaro96% (25)

- Strategic Management at Infosys (Business Strategy)Document19 pagesStrategic Management at Infosys (Business Strategy)Madhusudan22Pas encore d'évaluation

- Chap 04 and 05 (Mini Case)Document18 pagesChap 04 and 05 (Mini Case)ricky setiawan100% (1)

- Common Mistake and Exam TipsDocument16 pagesCommon Mistake and Exam TipsNguyễn Hồng NgọcPas encore d'évaluation

- Ringkasan Saham-20201120Document64 pagesRingkasan Saham-2020112012gogPas encore d'évaluation

- IFRIC 12 Service Concession AgreementDocument48 pagesIFRIC 12 Service Concession Agreementbheja2fryPas encore d'évaluation

- Foreign Capital and ForeignDocument11 pagesForeign Capital and Foreignalu_tPas encore d'évaluation

- Mitigating Control: 1. General InformationDocument2 pagesMitigating Control: 1. General InformationRavi KumarPas encore d'évaluation

- Ch05-Accounting PrincipleDocument9 pagesCh05-Accounting PrincipleEthanAhamed100% (2)

- Mock Reviewer in Management AccountingDocument6 pagesMock Reviewer in Management AccountingJA VicentePas encore d'évaluation

- Company Limited: Claim For Reimbursement of Motor Car Running ExpensesDocument1 pageCompany Limited: Claim For Reimbursement of Motor Car Running ExpensesRahul RawatPas encore d'évaluation

- Playing To Win: in The Business of SportsDocument8 pagesPlaying To Win: in The Business of SportsAshutosh JainPas encore d'évaluation

- ADAMS - 2021 Adam Sugar Mills Limited BalancesheetDocument6 pagesADAMS - 2021 Adam Sugar Mills Limited BalancesheetAfan QayumPas encore d'évaluation

- Sbi 8853 Dec 23 RecoDocument9 pagesSbi 8853 Dec 23 RecoShivam pandeyPas encore d'évaluation

- Book Invoice PDFDocument1 pageBook Invoice PDFnoamaanPas encore d'évaluation

- All 760953Document13 pagesAll 760953David CheishviliPas encore d'évaluation

- Materi PayLaterDocument18 pagesMateri PayLaterJonathan Martin LimbongPas encore d'évaluation

- CH 02Document3 pagesCH 02Osama Zaidiah100% (1)

- Cost-Volume-Profit Relationships: Management Accountant 1 and 2Document85 pagesCost-Volume-Profit Relationships: Management Accountant 1 and 2Bianca IyiyiPas encore d'évaluation