Vous aimerez peut-être aussi

- Plcy 08 IDocument3 pagesPlcy 08 ILam SameerPas encore d'évaluation

- PWC Shariah ReportDocument14 pagesPWC Shariah ReportTan Chay LingPas encore d'évaluation

- Libéralisation Du Compte CapitalDocument4 pagesLibéralisation Du Compte Capitalelyka.paintingPas encore d'évaluation

- TowerGroup CapMktsRegs Analystreport Nov 2009Document19 pagesTowerGroup CapMktsRegs Analystreport Nov 2009Upendra ChoudharyPas encore d'évaluation

- Assignment of FINANCIAL ManagementDocument5 pagesAssignment of FINANCIAL Managementjikkuabraham2Pas encore d'évaluation

- The Potential of The Bangladesh Capital MarketDocument6 pagesThe Potential of The Bangladesh Capital Marketসৌভিক দা'Pas encore d'évaluation

- Why Do Firms Invest in Foreign CountriesDocument9 pagesWhy Do Firms Invest in Foreign CountriesDelta YakinPas encore d'évaluation

- ASIC Senate Submission Update 3Document48 pagesASIC Senate Submission Update 3asxresearchPas encore d'évaluation

- Proposal For ReDocument3 pagesProposal For ReelvyannPas encore d'évaluation

- International Monetary ReformDocument4 pagesInternational Monetary ReformnaushitaPas encore d'évaluation

- Dirty DerivativesDocument8 pagesDirty DerivativesYan YanPas encore d'évaluation

- Structured Trade & Commodity Finance, The Future of Trade Finance / Transaction BankingDocument16 pagesStructured Trade & Commodity Finance, The Future of Trade Finance / Transaction BankingAmit Bhushan100% (3)

- The Importance of International Accounting StandardsDocument3 pagesThe Importance of International Accounting Standardssohansharma75Pas encore d'évaluation

- Capital Markets. Substantial Progress Has Been Made in Meeting The FourthDocument4 pagesCapital Markets. Substantial Progress Has Been Made in Meeting The FourthjsrfamilyPas encore d'évaluation

- JB2000 EmergingMarketsDocument51 pagesJB2000 EmergingMarketsTushar RastogiPas encore d'évaluation

- Effects of Strong or Weak EconomyDocument6 pagesEffects of Strong or Weak EconomyJawad Ul Hassan Shah100% (1)

- The Potential of The Bangladesh Capital MarketDocument14 pagesThe Potential of The Bangladesh Capital MarketMd. Ashraf Hossain SarkerPas encore d'évaluation

- Caleb M Fundanga: The Role of The Banking Sector in Combating Money LaunderingDocument5 pagesCaleb M Fundanga: The Role of The Banking Sector in Combating Money LaunderingHuyềnPas encore d'évaluation

- Capital Accounts - Liberalize or Not PDFDocument3 pagesCapital Accounts - Liberalize or Not PDFsiaaiaPas encore d'évaluation

- ReportDocument3 pagesReportnancysinglaPas encore d'évaluation

- The Islamic Financial Institutions (AAOIFI) Provides Guidance Standards That The Islamic Companies CanDocument4 pagesThe Islamic Financial Institutions (AAOIFI) Provides Guidance Standards That The Islamic Companies CanFarhaan MutturPas encore d'évaluation

- Capital Account Liberalisation in China: International PerspectivesDocument5 pagesCapital Account Liberalisation in China: International Perspectivesbantirocks_08Pas encore d'évaluation

- Barclays' Strategic Position Regarding New Financial Market RegulationsDocument21 pagesBarclays' Strategic Position Regarding New Financial Market Regulationskatarzena4228Pas encore d'évaluation

- The Potential of The Bangladesh Capital MarketDocument6 pagesThe Potential of The Bangladesh Capital MarketMd. Ashraf Hossain SarkerPas encore d'évaluation

- Focus On Market Maturity For Long Term GrowthDocument2 pagesFocus On Market Maturity For Long Term GrowthtntsilentPas encore d'évaluation

- CTA and Managed Futures Primer - Zero HedgeDocument6 pagesCTA and Managed Futures Primer - Zero HedgeAlexPas encore d'évaluation

- EMCompass Note+77 Creating+Domestic Cap Markets Dev CountriesDocument8 pagesEMCompass Note+77 Creating+Domestic Cap Markets Dev CountriesСаран ГэрэлPas encore d'évaluation

- Financing Risks Can Be Managed - Mining JournalDocument7 pagesFinancing Risks Can Be Managed - Mining JournalOwm Close CorporationPas encore d'évaluation

- Gatan - Critique PaperDocument5 pagesGatan - Critique PaperTimothy ValenciaPas encore d'évaluation

- Why Companies Engage in International Business Also Discuss Different Modes of Operations in International BusinessDocument16 pagesWhy Companies Engage in International Business Also Discuss Different Modes of Operations in International BusinessHassan IkhlaqPas encore d'évaluation

- Global Financial Crisis and Restructuring Strategies: Executive SummaryDocument11 pagesGlobal Financial Crisis and Restructuring Strategies: Executive Summaryus24787Pas encore d'évaluation

- Commentary: Richard Karl Goeltz OnDocument5 pagesCommentary: Richard Karl Goeltz Onbjudit97_885557958Pas encore d'évaluation

- Impact of Global Is at IonDocument7 pagesImpact of Global Is at IonsnehaPas encore d'évaluation

- BA 220-Starting International Operations-Keith BuduanDocument15 pagesBA 220-Starting International Operations-Keith BuduanScribd UserPas encore d'évaluation

- Walmart in UAEDocument13 pagesWalmart in UAESafa S. Ali0% (2)

- Benefits and CostsDocument5 pagesBenefits and CostsRuth Na MunyahPas encore d'évaluation

- Trade Finance AssignmentDocument5 pagesTrade Finance AssignmentEnoch BoafoPas encore d'évaluation

- Entry Mode - Docx IB ExamDocument8 pagesEntry Mode - Docx IB ExammonikaPas encore d'évaluation

- Reinventing The San Miguel Corporation ADocument3 pagesReinventing The San Miguel Corporation AJon Neri RosimoPas encore d'évaluation

- Goldman Sachs Presentation To The Sanford Bernstein Strategic Decisions Conference Comments by Gary Cohn, President & COODocument7 pagesGoldman Sachs Presentation To The Sanford Bernstein Strategic Decisions Conference Comments by Gary Cohn, President & COOapi-102917753Pas encore d'évaluation

- Chapter Six International Transparency and DisclosureDocument11 pagesChapter Six International Transparency and DisclosuremonikPas encore d'évaluation

- Deepening Capital Markets in The Philippines - McKinseyDocument7 pagesDeepening Capital Markets in The Philippines - McKinseyRohit BadavePas encore d'évaluation

- From The On-Ramp To The Freeway - Refueling Job Creation and Growth by Reconnecting Investors With Small-Cap CompaniesDocument31 pagesFrom The On-Ramp To The Freeway - Refueling Job Creation and Growth by Reconnecting Investors With Small-Cap CompaniesVanessa SchoenthalerPas encore d'évaluation

- Stock Market BubbleDocument34 pagesStock Market Bubbledefence007Pas encore d'évaluation

- Other ASX Research 4Document92 pagesOther ASX Research 4asxresearchPas encore d'évaluation

- Moving Toward Transparency: Capital Market in Indonesia: Stephen WellsDocument42 pagesMoving Toward Transparency: Capital Market in Indonesia: Stephen WellsAnggi PrawitasariPas encore d'évaluation

- Business Climate and Competitiveness of Moroccan CompaniesDocument21 pagesBusiness Climate and Competitiveness of Moroccan CompaniesOussama MimoPas encore d'évaluation

- Speech 140110Document6 pagesSpeech 140110ratiPas encore d'évaluation

- Teaching Notes FMI 342Document162 pagesTeaching Notes FMI 342Hemanth KumarPas encore d'évaluation

- Islamic Securitisation: Practical Aspects: Mr. Suleiman ABDI DUALEHDocument10 pagesIslamic Securitisation: Practical Aspects: Mr. Suleiman ABDI DUALEHtteckkaiPas encore d'évaluation

- Globalisation of Financial MarketDocument17 pagesGlobalisation of Financial MarketPiya SharmaPas encore d'évaluation

- Regulatory BankerDocument5 pagesRegulatory BankerFrnzie FrndzPas encore d'évaluation

- Financial Institution CH-5Document6 pagesFinancial Institution CH-5Gadisa TarikuPas encore d'évaluation

- FMGT6259 - Financial MarketsDocument156 pagesFMGT6259 - Financial Marketsp67kn6kfjvPas encore d'évaluation

- IfffDocument47 pagesIfffARJUN VPas encore d'évaluation

- The TerminologyDocument2 pagesThe TerminologyKriztel Loriene TribianaPas encore d'évaluation

- A Study On The Importance of Corporate Restructuring Approches in MalaysiaDocument13 pagesA Study On The Importance of Corporate Restructuring Approches in MalaysiaValerie SintiPas encore d'évaluation

- Backdoor ListingsDocument3 pagesBackdoor ListingsIndra PutraPas encore d'évaluation

- International MarketingDocument3 pagesInternational MarketingShivaPas encore d'évaluation

- Traditional KYC Process PDFDocument5 pagesTraditional KYC Process PDFvivxtractPas encore d'évaluation

- Vadi 3Document1 pageVadi 3vivxtractPas encore d'évaluation

- Public and Private KeyDocument5 pagesPublic and Private KeyvivxtractPas encore d'évaluation

- Vadi 1Document1 pageVadi 1vivxtractPas encore d'évaluation

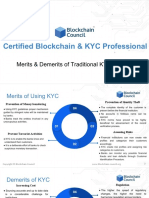

- Merits - Demerits of Traditional KYC Process PDFDocument4 pagesMerits - Demerits of Traditional KYC Process PDFvivxtractPas encore d'évaluation

- Vadi 2Document1 pageVadi 2vivxtractPas encore d'évaluation

- 1 - Exam OverviewDocument1 page1 - Exam OverviewvivxtractPas encore d'évaluation

- Amazon NG Photo Ark Book Invoice PDFDocument1 pageAmazon NG Photo Ark Book Invoice PDFvivxtractPas encore d'évaluation

- What Is KYC - PDFDocument6 pagesWhat Is KYC - PDFvivxtractPas encore d'évaluation

- Wstss Video InstructionsWSTSS Video InstructionsDocument5 pagesWstss Video InstructionsWSTSS Video InstructionsRobert PladetPas encore d'évaluation

- A4 Brochure-Updated-24jan2018 PDFDocument4 pagesA4 Brochure-Updated-24jan2018 PDFvivxtractPas encore d'évaluation

- WelcomeDocument13 pagesWelcomeUdai ValluruPas encore d'évaluation

- Introduction To CERTIFIED BLOCKCHAIN - KYC PROFESSIONAL PDFDocument14 pagesIntroduction To CERTIFIED BLOCKCHAIN - KYC PROFESSIONAL PDFvivxtractPas encore d'évaluation

- CAMS Practice ExamDocument37 pagesCAMS Practice Examvivxtract100% (1)

- Military PFIDocument81 pagesMilitary PFIvivxtractPas encore d'évaluation

- 0 - Welcome LetterDocument1 page0 - Welcome LettervivxtractPas encore d'évaluation

- Six Sigma Society: Exam Topics by BeltDocument2 pagesSix Sigma Society: Exam Topics by BeltvivxtractPas encore d'évaluation

- FATF Recommendations 2012 PDFDocument134 pagesFATF Recommendations 2012 PDFFxTraderBrazilPas encore d'évaluation

- 35 Imf Aml-CftDocument2 pages35 Imf Aml-CftvivxtractPas encore d'évaluation

- 5 - Job TipsDocument2 pages5 - Job TipsvivxtractPas encore d'évaluation

- ATT00001Document1 pageATT00001vivxtractPas encore d'évaluation

- Impt TopicsDocument1 pageImpt TopicsvivxtractPas encore d'évaluation

- Problem Structuring: The Process of Soda ModellingDocument4 pagesProblem Structuring: The Process of Soda ModellingvivxtractPas encore d'évaluation

- My YouTube PlaylistDocument1 pageMy YouTube PlaylistvivxtractPas encore d'évaluation

- 165451819Document7 pages165451819vivxtractPas encore d'évaluation

- How Useful Is QRA - George ApostolakisDocument0 pageHow Useful Is QRA - George ApostolakisvivxtractPas encore d'évaluation

- Sights and Attractions Near London Eye - LondonTownDocument4 pagesSights and Attractions Near London Eye - LondonTownvivxtractPas encore d'évaluation

- Efficiency Hypothesis of The Stock Exchange Project Presented by MR CAMARA MOHAMED BINTOUDocument113 pagesEfficiency Hypothesis of The Stock Exchange Project Presented by MR CAMARA MOHAMED BINTOUCamara Mohamed Bintou100% (1)

- HHHJJDocument6 pagesHHHJJNiks MonzantoPas encore d'évaluation

- Indian Aluminium IndustryDocument6 pagesIndian Aluminium IndustryAmrisha VermaPas encore d'évaluation

- Journal of Business Valuation 2016 Final PDFDocument93 pagesJournal of Business Valuation 2016 Final PDFOren BouzagloPas encore d'évaluation

- Bonds CallableDocument52 pagesBonds CallablekalyanshreePas encore d'évaluation

- Top 10 Fixed Return Option Trading Strategies by Kavita MehataniDocument53 pagesTop 10 Fixed Return Option Trading Strategies by Kavita Mehatanitarun gautam78% (9)

- Treasury Investment Policy - Lecture - Session 4 PDFDocument36 pagesTreasury Investment Policy - Lecture - Session 4 PDFQamber AliPas encore d'évaluation

- Finance Thesis BBA PakistanDocument73 pagesFinance Thesis BBA Pakistanhotprince100% (5)

- Mynamar InvestmentDocument22 pagesMynamar InvestmentSebastian ZwphPas encore d'évaluation

- A Guide To Joe Dinapoli'S D-Levels™ Studies Using GFT'S Dealbook FX® 2Document20 pagesA Guide To Joe Dinapoli'S D-Levels™ Studies Using GFT'S Dealbook FX® 2Nei Lima100% (1)

- Risk in Capital Structure Arbitrage 2006Document46 pagesRisk in Capital Structure Arbitrage 2006jinwei2011Pas encore d'évaluation

- F & S InvestmentsDocument16 pagesF & S Investments7aadkhan100% (2)

- Ambee Pharmaceuticals Limited: First Quarter Financial Statement (Un-Audited)Document1 pageAmbee Pharmaceuticals Limited: First Quarter Financial Statement (Un-Audited)James BlackPas encore d'évaluation

- Forex Fundamental AnalysisDocument2 pagesForex Fundamental Analysistejasvigopal100% (1)

- Samara CapitalDocument1 pageSamara CapitalALLtyPas encore d'évaluation

- Barron 39 S 01 June 2020 PDFDocument80 pagesBarron 39 S 01 June 2020 PDFastarini EndahPas encore d'évaluation

- IAS 12 Income TaxDocument40 pagesIAS 12 Income TaxfurqanPas encore d'évaluation

- Portfolio Manager's Review: The Magic Formula Issue, by The Manual of IdeasDocument401 pagesPortfolio Manager's Review: The Magic Formula Issue, by The Manual of IdeasThe Manual of Ideas100% (2)

- Beams10e - Ch09 Indirect and Mutual HoldingsDocument36 pagesBeams10e - Ch09 Indirect and Mutual HoldingsLeini Tan100% (1)

- Fxtradermagazine 1 EgDocument61 pagesFxtradermagazine 1 EgDoncov EngenyPas encore d'évaluation

- Econ 261: Principles of Finance Quiz 2-40 Marks: InstructionsDocument2 pagesEcon 261: Principles of Finance Quiz 2-40 Marks: InstructionsRehan HasanPas encore d'évaluation

- Behind The Performance of Equally Weighted Indices PDFDocument7 pagesBehind The Performance of Equally Weighted Indices PDFGanesh ShresthaPas encore d'évaluation

- TremblantDocument5 pagesTremblantdeep211Pas encore d'évaluation

- Chapter 3: Forward and Futures Prices: Continuous CompoundingDocument7 pagesChapter 3: Forward and Futures Prices: Continuous Compoundingsunilp14Pas encore d'évaluation

- MOP-Capital Theory Assignment-020310Document4 pagesMOP-Capital Theory Assignment-020310charnu1988Pas encore d'évaluation

- Aspeon Sparkling Water, Inc. Capital Structure Policy: Case 10Document16 pagesAspeon Sparkling Water, Inc. Capital Structure Policy: Case 10Alla LiPas encore d'évaluation

- Secondary MarketDocument13 pagesSecondary MarketKanchan GuptaPas encore d'évaluation

- Interview With A Stock BrokerDocument8 pagesInterview With A Stock Brokertarachandmara100% (3)

- Icf LCF A BookletDocument20 pagesIcf LCF A BookletDhwanik DoshiPas encore d'évaluation

- CAPITAL ASSET PRICING MODEL - A Study On Indian Stock MarketsDocument78 pagesCAPITAL ASSET PRICING MODEL - A Study On Indian Stock Marketsnikhincc100% (1)

- Alpha and The Paradox of Skill (MMauboussin - July '13)Document12 pagesAlpha and The Paradox of Skill (MMauboussin - July '13)Alexander LuePas encore d'évaluation