Vous aimerez peut-être aussi

- Crisil: Performance HighlightsDocument9 pagesCrisil: Performance HighlightsAngel BrokingPas encore d'évaluation

- Federal Bank: Performance HighlightsDocument11 pagesFederal Bank: Performance HighlightsAngel BrokingPas encore d'évaluation

- DB Corp: Performance HighlightsDocument11 pagesDB Corp: Performance HighlightsAngel BrokingPas encore d'évaluation

- Infosys Result UpdatedDocument15 pagesInfosys Result UpdatedAngel BrokingPas encore d'évaluation

- ITC Result UpdatedDocument15 pagesITC Result UpdatedAngel BrokingPas encore d'évaluation

- Infosys Result UpdatedDocument14 pagesInfosys Result UpdatedAngel BrokingPas encore d'évaluation

- ITC Result UpdatedDocument15 pagesITC Result UpdatedAngel BrokingPas encore d'évaluation

- Infosys: Performance HighlightsDocument15 pagesInfosys: Performance HighlightsAngel BrokingPas encore d'évaluation

- Infosys: Performance HighlightsDocument15 pagesInfosys: Performance HighlightsAtul ShahiPas encore d'évaluation

- IDBI Bank: Performance HighlightsDocument13 pagesIDBI Bank: Performance HighlightsAngel BrokingPas encore d'évaluation

- GSK ConsumerDocument10 pagesGSK ConsumerAngel BrokingPas encore d'évaluation

- Dena Bank Result UpdatedDocument10 pagesDena Bank Result UpdatedAngel BrokingPas encore d'évaluation

- Bank of India Result UpdatedDocument12 pagesBank of India Result UpdatedAngel BrokingPas encore d'évaluation

- DB Corp: Performance HighlightsDocument11 pagesDB Corp: Performance HighlightsAngel BrokingPas encore d'évaluation

- Corporation Bank Result UpdatedDocument11 pagesCorporation Bank Result UpdatedAngel BrokingPas encore d'évaluation

- JP Associates Result UpdatedDocument12 pagesJP Associates Result UpdatedAngel BrokingPas encore d'évaluation

- Icici Bank: Performance HighlightsDocument15 pagesIcici Bank: Performance HighlightsAngel BrokingPas encore d'évaluation

- Persistent, 29th January 2013Document12 pagesPersistent, 29th January 2013Angel BrokingPas encore d'évaluation

- Yes Bank: Performance HighlightsDocument12 pagesYes Bank: Performance HighlightsAngel BrokingPas encore d'évaluation

- Moil 2qfy2013Document10 pagesMoil 2qfy2013Angel BrokingPas encore d'évaluation

- Persistent Systems Result UpdatedDocument11 pagesPersistent Systems Result UpdatedAngel BrokingPas encore d'évaluation

- DB Corp.: Performance HighlightsDocument11 pagesDB Corp.: Performance HighlightsAngel BrokingPas encore d'évaluation

- ICICI Bank Result UpdatedDocument16 pagesICICI Bank Result UpdatedAngel BrokingPas encore d'évaluation

- HCLTech 3Q FY13Document16 pagesHCLTech 3Q FY13Angel BrokingPas encore d'évaluation

- Bosch 3qcy2012ruDocument12 pagesBosch 3qcy2012ruAngel BrokingPas encore d'évaluation

- Hex AwareDocument14 pagesHex AwareAngel BrokingPas encore d'évaluation

- Tata Consultancy Services Result UpdatedDocument14 pagesTata Consultancy Services Result UpdatedAngel BrokingPas encore d'évaluation

- Glaxosmithkline Pharma: Performance HighlightsDocument11 pagesGlaxosmithkline Pharma: Performance HighlightsAngel BrokingPas encore d'évaluation

- HCL Technologies: Performance HighlightsDocument15 pagesHCL Technologies: Performance HighlightsAngel BrokingPas encore d'évaluation

- Ashoka Buildcon: Performance HighlightsDocument14 pagesAshoka Buildcon: Performance HighlightsAngel BrokingPas encore d'évaluation

- Jagran Prakashan: Performance HighlightsDocument10 pagesJagran Prakashan: Performance HighlightsAngel BrokingPas encore d'évaluation

- Reliance Communication: Performance HighlightsDocument11 pagesReliance Communication: Performance HighlightsAngel BrokingPas encore d'évaluation

- S. Kumars Nationwide: Performance HighlightsDocument19 pagesS. Kumars Nationwide: Performance HighlightsmarathiPas encore d'évaluation

- Jyoti Structures: Performance HighlightsDocument12 pagesJyoti Structures: Performance HighlightsAngel BrokingPas encore d'évaluation

- HDFC Result UpdatedDocument12 pagesHDFC Result UpdatedAngel BrokingPas encore d'évaluation

- Mphasis Result UpdatedDocument12 pagesMphasis Result UpdatedAngel BrokingPas encore d'évaluation

- UCO Bank: Performance HighlightsDocument11 pagesUCO Bank: Performance HighlightsAngel BrokingPas encore d'évaluation

- Hexaware Result UpdatedDocument14 pagesHexaware Result UpdatedAngel BrokingPas encore d'évaluation

- Motherson Sumi Systems Result UpdatedDocument14 pagesMotherson Sumi Systems Result UpdatedAngel BrokingPas encore d'évaluation

- Indraprasth Gas Result UpdatedDocument10 pagesIndraprasth Gas Result UpdatedAngel BrokingPas encore d'évaluation

- Rallis India Result UpdatedDocument10 pagesRallis India Result UpdatedAngel BrokingPas encore d'évaluation

- Subros Result UpdatedDocument10 pagesSubros Result UpdatedAngel BrokingPas encore d'évaluation

- Finolex Cables: Performance HighlightsDocument10 pagesFinolex Cables: Performance HighlightsAngel BrokingPas encore d'évaluation

- Performance Highlights: NeutralDocument10 pagesPerformance Highlights: NeutralAngel BrokingPas encore d'évaluation

- Infosys Result UpdatedDocument14 pagesInfosys Result UpdatedAngel BrokingPas encore d'évaluation

- HCL Technologies 3QFY2011 Result Update | Strong Growth Momentum ContinuesDocument16 pagesHCL Technologies 3QFY2011 Result Update | Strong Growth Momentum Continueskrishnakumarsasc1Pas encore d'évaluation

- DB Corp 4Q FY 2013Document11 pagesDB Corp 4Q FY 2013Angel BrokingPas encore d'évaluation

- IRB Infrastructure: Performance HighlightsDocument13 pagesIRB Infrastructure: Performance HighlightsAndy FlowerPas encore d'évaluation

- Axis Bank Result UpdatedDocument13 pagesAxis Bank Result UpdatedAngel BrokingPas encore d'évaluation

- Bajaj Electricals: Performance HighlightsDocument10 pagesBajaj Electricals: Performance HighlightsAngel BrokingPas encore d'évaluation

- Ll& FS Transportation NetworksDocument14 pagesLl& FS Transportation NetworksAngel BrokingPas encore d'évaluation

- Hexaware Result UpdatedDocument13 pagesHexaware Result UpdatedAngel BrokingPas encore d'évaluation

- Dena BankDocument11 pagesDena BankAngel BrokingPas encore d'évaluation

- Crompton Greaves: Performance HighlightsDocument12 pagesCrompton Greaves: Performance HighlightsAngel BrokingPas encore d'évaluation

- Union Bank of India Result UpdatedDocument11 pagesUnion Bank of India Result UpdatedAngel BrokingPas encore d'évaluation

- Allcargo Global Logistics LTD.: CompanyDocument5 pagesAllcargo Global Logistics LTD.: CompanyjoycoolPas encore d'évaluation

- Aventis Pharma Result UpdatedDocument10 pagesAventis Pharma Result UpdatedAngel BrokingPas encore d'évaluation

- KEC International Result UpdatedDocument11 pagesKEC International Result UpdatedAngel BrokingPas encore d'évaluation

- Bank of BarodaDocument12 pagesBank of BarodaAngel BrokingPas encore d'évaluation

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsD'EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsPas encore d'évaluation

- WPIInflation August2013Document5 pagesWPIInflation August2013Angel BrokingPas encore d'évaluation

- Technical & Derivative Analysis Weekly-14092013Document6 pagesTechnical & Derivative Analysis Weekly-14092013Angel Broking100% (1)

- Ranbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertDocument4 pagesRanbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertAngel BrokingPas encore d'évaluation

- Metal and Energy Tech Report November 12Document2 pagesMetal and Energy Tech Report November 12Angel BrokingPas encore d'évaluation

- Commodities Weekly Tracker 16th Sept 2013Document23 pagesCommodities Weekly Tracker 16th Sept 2013Angel BrokingPas encore d'évaluation

- Daily Agri Tech Report September 14 2013Document2 pagesDaily Agri Tech Report September 14 2013Angel BrokingPas encore d'évaluation

- Daily Agri Report September 16 2013Document9 pagesDaily Agri Report September 16 2013Angel BrokingPas encore d'évaluation

- Special Technical Report On NCDEX Oct SoyabeanDocument2 pagesSpecial Technical Report On NCDEX Oct SoyabeanAngel BrokingPas encore d'évaluation

- Oilseeds and Edible Oil UpdateDocument9 pagesOilseeds and Edible Oil UpdateAngel BrokingPas encore d'évaluation

- International Commodities Evening Update September 16 2013Document3 pagesInternational Commodities Evening Update September 16 2013Angel BrokingPas encore d'évaluation

- Commodities Weekly Outlook 16-09-13 To 20-09-13Document6 pagesCommodities Weekly Outlook 16-09-13 To 20-09-13Angel BrokingPas encore d'évaluation

- Daily Technical Report: Sensex (19733) / NIFTY (5851)Document4 pagesDaily Technical Report: Sensex (19733) / NIFTY (5851)Angel BrokingPas encore d'évaluation

- Daily Metals and Energy Report September 16 2013Document6 pagesDaily Metals and Energy Report September 16 2013Angel BrokingPas encore d'évaluation

- Currency Daily Report September 16 2013Document4 pagesCurrency Daily Report September 16 2013Angel BrokingPas encore d'évaluation

- Daily Agri Tech Report September 16 2013Document2 pagesDaily Agri Tech Report September 16 2013Angel BrokingPas encore d'évaluation

- Derivatives Report 16 Sept 2013Document3 pagesDerivatives Report 16 Sept 2013Angel BrokingPas encore d'évaluation

- Technical Report 13.09.2013Document4 pagesTechnical Report 13.09.2013Angel BrokingPas encore d'évaluation

- Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook: Dealer's DiaryAngel BrokingPas encore d'évaluation

- Sugar Update Sepetmber 2013Document7 pagesSugar Update Sepetmber 2013Angel BrokingPas encore d'évaluation

- Press Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressDocument1 pagePress Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressAngel BrokingPas encore d'évaluation

- IIP CPIDataReleaseDocument5 pagesIIP CPIDataReleaseAngel BrokingPas encore d'évaluation

- Market Outlook 13-09-2013Document12 pagesMarket Outlook 13-09-2013Angel BrokingPas encore d'évaluation

- TechMahindra CompanyUpdateDocument4 pagesTechMahindra CompanyUpdateAngel BrokingPas encore d'évaluation

- Derivatives Report 8th JanDocument3 pagesDerivatives Report 8th JanAngel BrokingPas encore d'évaluation

- Tata Motors: Jaguar Land Rover - Monthly Sales UpdateDocument6 pagesTata Motors: Jaguar Land Rover - Monthly Sales UpdateAngel BrokingPas encore d'évaluation

- MarketStrategy September2013Document4 pagesMarketStrategy September2013Angel BrokingPas encore d'évaluation

- MetalSectorUpdate September2013Document10 pagesMetalSectorUpdate September2013Angel BrokingPas encore d'évaluation

- Metal and Energy Tech Report Sept 13Document2 pagesMetal and Energy Tech Report Sept 13Angel BrokingPas encore d'évaluation

- Daily Agri Tech Report September 06 2013Document2 pagesDaily Agri Tech Report September 06 2013Angel BrokingPas encore d'évaluation

- Jaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechDocument4 pagesJaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechAngel BrokingPas encore d'évaluation

- Final Accounts Without AdjustmentsDocument22 pagesFinal Accounts Without AdjustmentsFaizan MisbahuddinPas encore d'évaluation

- FM Chapter 9Document8 pagesFM Chapter 9Bebean AninangPas encore d'évaluation

- Tax Invoice: Billing Address Installation Address Invoice DetailsDocument1 pageTax Invoice: Billing Address Installation Address Invoice DetailsKuladeep Naidu PatibandlaPas encore d'évaluation

- Angelo Chua 庄向志 PETA 1 Financial StatementsDocument4 pagesAngelo Chua 庄向志 PETA 1 Financial Statements채문길Pas encore d'évaluation

- 014 - Acceptance For Value A4vDocument2 pages014 - Acceptance For Value A4vDavid E Robinson95% (43)

- FFM 9 Im 13Document15 pagesFFM 9 Im 13Ernest NyangiPas encore d'évaluation

- Capital Structure - Bharati CementDocument14 pagesCapital Structure - Bharati CementMohmmedKhayyumPas encore d'évaluation

- Commercial Paper: (Industrial Paper, Finance Paper, Corporate Paper)Document27 pagesCommercial Paper: (Industrial Paper, Finance Paper, Corporate Paper)shivakumar N100% (1)

- PFRS 9Document1 pagePFRS 9Ella MaePas encore d'évaluation

- Pakistan Stock Exchange Limited: Internet Trading Subscribers ListDocument3 pagesPakistan Stock Exchange Limited: Internet Trading Subscribers ListMuhammad AhmedPas encore d'évaluation

- Revenue Code 2023Document113 pagesRevenue Code 2023Mark Andrei GubacPas encore d'évaluation

- Money ManagementDocument12 pagesMoney ManagementRachelle Gunderson SmithPas encore d'évaluation

- TVM and No-Arbitrage Principle: Practice Questions and ProblemsDocument2 pagesTVM and No-Arbitrage Principle: Practice Questions and ProblemsMavisPas encore d'évaluation

- 57b2e7d35a4d40b8b460abe4914d711a.docxDocument6 pages57b2e7d35a4d40b8b460abe4914d711a.docxZohaib HajizubairPas encore d'évaluation

- Statement - 271185814 - Juan Camilo Cardenas AguirreDocument12 pagesStatement - 271185814 - Juan Camilo Cardenas AguirrePedro Ant. Núñez UlloaPas encore d'évaluation

- Problem 1 1245Document3 pagesProblem 1 1245Rhanda BernardoPas encore d'évaluation

- LOAN REQUIREMENTS OF BANKS AND NONBANKSDocument84 pagesLOAN REQUIREMENTS OF BANKS AND NONBANKSPhill SamontePas encore d'évaluation

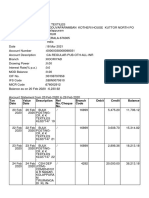

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument4 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceJaseem MonuPas encore d'évaluation

- Background of The StudyDocument2 pagesBackground of The StudyAdonis GaoiranPas encore d'évaluation

- Project Proposal On The EstablishmentDocument35 pagesProject Proposal On The Establishmentwendemu100% (1)

- Tax Free ExchangeDocument4 pagesTax Free ExchangeLara YuloPas encore d'évaluation

- JPM Annual ReportDocument50 pagesJPM Annual ReportSummaiya BarkatPas encore d'évaluation

- CF (MBF131) Exam QDocument13 pagesCF (MBF131) Exam QSai Set NaingPas encore d'évaluation

- S. Strange InternationalDocument28 pagesS. Strange InternationalMircea Muresan100% (1)

- Terms and Conditions of The Loan AgreementsDocument2 pagesTerms and Conditions of The Loan AgreementsCLATOUS CHAMAPas encore d'évaluation

- Investment BankingDocument4 pagesInvestment BankingNirajGBhaduwalaPas encore d'évaluation

- Working Capital ManagementDocument39 pagesWorking Capital ManagementRebelliousRascalPas encore d'évaluation

- Sample Problems Solutions Sections 2.3 & 2.4.: R P P M A R MDocument5 pagesSample Problems Solutions Sections 2.3 & 2.4.: R P P M A R MTerry Clarice DecatoriaPas encore d'évaluation

- JPMorgan Chase Bank statement summaryDocument6 pagesJPMorgan Chase Bank statement summaryytprem agu100% (2)

- Agricultural Business ManagementDocument5 pagesAgricultural Business ManagementAreicra NutPas encore d'évaluation