Vous aimerez peut-être aussi

- FA - ACCA Lecture NotesDocument115 pagesFA - ACCA Lecture NotesmosesmuomelitePas encore d'évaluation

- Accounting Concepts and Conventions ExplainedDocument115 pagesAccounting Concepts and Conventions ExplainedSomesh PalPas encore d'évaluation

- Accounting & Financial Systems MCPC 606: Service ExcellenceDocument90 pagesAccounting & Financial Systems MCPC 606: Service ExcellenceRight Karl-Maccoy HattohPas encore d'évaluation

- Financial Accounting: January 31, 2013 L&T MDC Vivek KrishnamoorthyDocument43 pagesFinancial Accounting: January 31, 2013 L&T MDC Vivek KrishnamoorthyAltaf AshrafPas encore d'évaluation

- Chapter 1Document40 pagesChapter 1Galata NugusaPas encore d'évaluation

- Basic ConceptsDocument26 pagesBasic ConceptsKaranPas encore d'évaluation

- Accounting Business and Management ABMDocument42 pagesAccounting Business and Management ABMJacky SereñoPas encore d'évaluation

- Introduction To Accounting Gp1 by Professor & Lawyer Puttu Guru PrasadDocument33 pagesIntroduction To Accounting Gp1 by Professor & Lawyer Puttu Guru PrasadPUTTU GURU PRASAD SENGUNTHA MUDALIARPas encore d'évaluation

- Lecture 1 - (Chapter 1) Accounting and The Business EnvironmentDocument8 pagesLecture 1 - (Chapter 1) Accounting and The Business EnvironmentCalin-Mihai RacotiPas encore d'évaluation

- Chapter 2 Fundamentals of AccountingDocument29 pagesChapter 2 Fundamentals of AccountingJohn Mark MaligaligPas encore d'évaluation

- Understanding Accounting PrinciplesDocument27 pagesUnderstanding Accounting PrinciplesRaahim NajmiPas encore d'évaluation

- Introduction To AccountingDocument27 pagesIntroduction To AccountingVibhat Chabra 225013Pas encore d'évaluation

- Lecture 6 Bus. MNGMNTDocument69 pagesLecture 6 Bus. MNGMNTAizhan BaimukhamedovaPas encore d'évaluation

- FOA I HandoutDocument88 pagesFOA I HandoutIbsa MohammedPas encore d'évaluation

- Introduction To Financial Accounting - Gp1 by Professor & Lawyer Puttu Guru PrasadDocument70 pagesIntroduction To Financial Accounting - Gp1 by Professor & Lawyer Puttu Guru PrasadPUTTU GURU PRASAD SENGUNTHA MUDALIARPas encore d'évaluation

- Accounting All ChaptersDocument155 pagesAccounting All ChaptersHasnain Ahmad KhanPas encore d'évaluation

- Accounting: The Language of BusinessDocument30 pagesAccounting: The Language of BusinessMuhammad AzamPas encore d'évaluation

- ACCOUNTINGDocument31 pagesACCOUNTINGCHARAK RAYPas encore d'évaluation

- Chapter 1 - Accounting As A Form of Communication (Notes)Document7 pagesChapter 1 - Accounting As A Form of Communication (Notes)Hareem Zoya WarsiPas encore d'évaluation

- Theory QuestionsDocument6 pagesTheory Questionsanky1555Pas encore d'évaluation

- AccountingDocument4 pagesAccountingKristine Marie ParalPas encore d'évaluation

- Raya University Business and Economics Accounting and Finance Program Course Title: Financial Accounting I By: Mr. Fantay AlemayehuDocument15 pagesRaya University Business and Economics Accounting and Finance Program Course Title: Financial Accounting I By: Mr. Fantay AlemayehuFantayPas encore d'évaluation

- FINANCE FOR NON-FINANCEDocument32 pagesFINANCE FOR NON-FINANCEZhuwenyuanPas encore d'évaluation

- C1 ACCOUNTING AND BOOKKEEPING FUNDAMENTALSDocument5 pagesC1 ACCOUNTING AND BOOKKEEPING FUNDAMENTALSIleana SendreaPas encore d'évaluation

- For ACCO 101 - Review of Accounting Concepts and Process (Part 1)Document32 pagesFor ACCO 101 - Review of Accounting Concepts and Process (Part 1)Fionna Rei DeGaliciaPas encore d'évaluation

- Accounting ProcessDocument17 pagesAccounting ProcessDurga Prasad100% (1)

- Accounting Concepts and Financial StatementsDocument47 pagesAccounting Concepts and Financial Statementsmukul3087_305865623Pas encore d'évaluation

- ACC 124 - Assignment 1Document7 pagesACC 124 - Assignment 1RuzuiPas encore d'évaluation

- Finance For Non FinanceDocument32 pagesFinance For Non FinanceAmol MJ100% (1)

- 1 Session: Introduction To AccountingDocument51 pages1 Session: Introduction To Accountingnilanjan_kar_2Pas encore d'évaluation

- Understanding Financial Statements - A Basic OverviewDocument49 pagesUnderstanding Financial Statements - A Basic OverviewSarith SagarPas encore d'évaluation

- 2857 - Accounting For Governmental and Non-Profit Organizations-203203-Chapter 3Document70 pages2857 - Accounting For Governmental and Non-Profit Organizations-203203-Chapter 3shital_vyas1987Pas encore d'évaluation

- IntroductionDocument53 pagesIntroductionhippop kPas encore d'évaluation

- Chapter-1 Accounting For NgoDocument70 pagesChapter-1 Accounting For Ngoshital_vyas1987100% (1)

- 1 Introduction Financial Accounting 1 (Cuacm105)Document17 pages1 Introduction Financial Accounting 1 (Cuacm105)priviledgeshambare2004Pas encore d'évaluation

- Introduction To Financial AccountingDocument64 pagesIntroduction To Financial AccountingGurkirat Singh100% (1)

- Finance For Non Finance Professionals Statements and RatiosDocument32 pagesFinance For Non Finance Professionals Statements and Ratioskrithika1288Pas encore d'évaluation

- Introdution To AccountingDocument56 pagesIntrodution To Accountingrezel joyce catloanPas encore d'évaluation

- 1.1. AccountingDocument5 pages1.1. AccountingAnwar AdemPas encore d'évaluation

- Advanced Corporate AccountingDocument242 pagesAdvanced Corporate AccountingMuskan GuptaPas encore d'évaluation

- Accounting For Manager: Accounting Period April and Ends On 31 March Every Year Unless Otherwise Specifically MentionedDocument66 pagesAccounting For Manager: Accounting Period April and Ends On 31 March Every Year Unless Otherwise Specifically Mentionedbaburao1762Pas encore d'évaluation

- BM Unit 3.4 Final Accounts HLDocument81 pagesBM Unit 3.4 Final Accounts HLJacqueline Levana HuliselanPas encore d'évaluation

- Discuss The Users of Financial Information Internal UsersDocument6 pagesDiscuss The Users of Financial Information Internal UsersStephen Pilar PortilloPas encore d'évaluation

- Financial Accounting & AnalysisDocument146 pagesFinancial Accounting & AnalysisGagan ChoudharyPas encore d'évaluation

- Balance Sheet: What Do You Mean by Corporate Financial Statements?Document3 pagesBalance Sheet: What Do You Mean by Corporate Financial Statements?maabachaPas encore d'évaluation

- Analyzing TransactionsDocument3 pagesAnalyzing TransactionsMark SantosPas encore d'évaluation

- Accounting Fundamentals for Decision MakersDocument65 pagesAccounting Fundamentals for Decision MakersElwin Michaelraj VictorPas encore d'évaluation

- Activities and Assessment 1Document4 pagesActivities and Assessment 1Mante, Josh Adrian Greg S.Pas encore d'évaluation

- CSEC Principles of Accounts NotesDocument66 pagesCSEC Principles of Accounts NotesAbdullah Ali97% (31)

- Introduction To AccountingDocument5 pagesIntroduction To AccountingMardy DahuyagPas encore d'évaluation

- ACC406 - Topic 1 IntroDocument25 pagesACC406 - Topic 1 IntroSahfirah FirahPas encore d'évaluation

- FRA-NewDocument31 pagesFRA-NewAbhishek DograPas encore d'évaluation

- Acc Fundamentals IntroductionDocument18 pagesAcc Fundamentals IntroductionManisha DeyPas encore d'évaluation

- BA100FMREVIEWERDocument8 pagesBA100FMREVIEWERMadelyn GayolPas encore d'évaluation

- Chapter 1Document23 pagesChapter 1mahiramazoon mazoonPas encore d'évaluation

- ACAD - EDGE Edition 1 (Financial Accounting)Document25 pagesACAD - EDGE Edition 1 (Financial Accounting)Sarthak GuptaPas encore d'évaluation

- Introduction To Financial Accounting LECTURE ONEDocument30 pagesIntroduction To Financial Accounting LECTURE ONEziajehanPas encore d'évaluation

- Chapter (1) Accounting Concepts and Framework: (ALL IAS or IFRS Based On One or More of These Concepts)Document16 pagesChapter (1) Accounting Concepts and Framework: (ALL IAS or IFRS Based On One or More of These Concepts)Shwe TharPas encore d'évaluation

- Accountancy Profession and DevelopmentDocument6 pagesAccountancy Profession and DevelopmentGwyneth EdicaPas encore d'évaluation

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"D'Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Pas encore d'évaluation

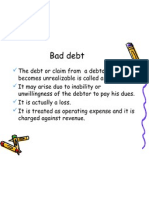

- Bad DebtDocument16 pagesBad DebtWasim AkramPas encore d'évaluation

- Bad DebtDocument16 pagesBad DebtWasim AkramPas encore d'évaluation

- EPS-unit 2aDocument53 pagesEPS-unit 2aWasim AkramPas encore d'évaluation

- Accounting and Economic Decisions: Sharad Bhattacharya Faculty, AIMKDocument40 pagesAccounting and Economic Decisions: Sharad Bhattacharya Faculty, AIMKWasim AkramPas encore d'évaluation

- Legal Opinion Johnsan Blue Industrial Suspension AmendmentDocument2 pagesLegal Opinion Johnsan Blue Industrial Suspension AmendmentRudiver Jungco JrPas encore d'évaluation

- Retail Management: A Strategic Approach: 11th EditionDocument9 pagesRetail Management: A Strategic Approach: 11th EditionMohamed El KadyPas encore d'évaluation

- Handbook of Value Added Tax by Farid Mohammad NasirDocument15 pagesHandbook of Value Added Tax by Farid Mohammad NasirSamia SultanaPas encore d'évaluation

- Buku2 Ref Ujian WMIDocument3 pagesBuku2 Ref Ujian WMIEndy JupriansyahPas encore d'évaluation

- NEC Contracts - One Stop ShopDocument3 pagesNEC Contracts - One Stop ShopHarish NeelakantanPas encore d'évaluation

- Chloe's ClosetDocument17 pagesChloe's ClosetCheeze cake100% (1)

- Costing for FDLC JDE and brightERP ProjectsDocument4 pagesCosting for FDLC JDE and brightERP ProjectsanoopPas encore d'évaluation

- The Impact of Effective Public Relations On Organizational Performance in Micmakin Nigeria LimitedDocument8 pagesThe Impact of Effective Public Relations On Organizational Performance in Micmakin Nigeria LimitedBajegbo OluwadamilarePas encore d'évaluation

- Demantra and ASCP Presentation PDFDocument54 pagesDemantra and ASCP Presentation PDFvenvimal1Pas encore d'évaluation

- Problem Solving: 1. Relay Corp. Manufactures Batons. Relay Can Manufacture 300,000 Batons A Year at ADocument2 pagesProblem Solving: 1. Relay Corp. Manufactures Batons. Relay Can Manufacture 300,000 Batons A Year at AMa Teresa B. CerezoPas encore d'évaluation

- Baby Food IndustryDocument13 pagesBaby Food IndustryPragati BhartiPas encore d'évaluation

- Case 3 4Document2 pagesCase 3 4Salvie Angela Clarette UtanaPas encore d'évaluation

- COA 016 Audit Checklist For Coal Operation Health and Safety Management Systems PDFDocument43 pagesCOA 016 Audit Checklist For Coal Operation Health and Safety Management Systems PDFMaia FitzgeraldPas encore d'évaluation

- Accounting For Special Transaction and Business Combinations Multiple Choice - Problem SolvingDocument5 pagesAccounting For Special Transaction and Business Combinations Multiple Choice - Problem SolvingJustine Reine CornicoPas encore d'évaluation

- Project of T.Y BbaDocument49 pagesProject of T.Y BbaJeet Mehta0% (1)

- ISO 14000 Understanding, Documenting and Implementing Slides R8.02.05Document195 pagesISO 14000 Understanding, Documenting and Implementing Slides R8.02.05Tanuj MadaanPas encore d'évaluation

- Exercises w7+8Document3 pagesExercises w7+8TâmPas encore d'évaluation

- Airport Urbanism Max HirshDocument4 pagesAirport Urbanism Max HirshMukesh WaranPas encore d'évaluation

- Supply Chain Management Part 1 Lecture OutlineDocument17 pagesSupply Chain Management Part 1 Lecture OutlineEmmanuel Cocou kounouhoPas encore d'évaluation

- POMOFFICIALLECTUREDocument919 pagesPOMOFFICIALLECTURER A GelilangPas encore d'évaluation

- GROSS INCOME and DEDUCTIONSDocument10 pagesGROSS INCOME and DEDUCTIONSMHERITZ LYN LIM MAYOLAPas encore d'évaluation

- Footwear Industry in NepalDocument76 pagesFootwear Industry in Nepalsubham jaiswalPas encore d'évaluation

- Jio January Invoice Receipt-Arvind Kumar SharmaDocument4 pagesJio January Invoice Receipt-Arvind Kumar SharmaArvind SharmaPas encore d'évaluation

- Csa z1600 Emergency and Continuity Management Program - Ron MeyersDocument23 pagesCsa z1600 Emergency and Continuity Management Program - Ron MeyersDidu DaduPas encore d'évaluation

- (N-Ab) (1-A) : To Tariffs)Document16 pages(N-Ab) (1-A) : To Tariffs)Amelia JPas encore d'évaluation

- Haystack Syndrome (Eliyahu M. Goldratt) (Z-Library)Document270 pagesHaystack Syndrome (Eliyahu M. Goldratt) (Z-Library)jmulder1100% (3)

- WEEK 10-Compensating Human Resources and Employee Benfeits and ServicesDocument8 pagesWEEK 10-Compensating Human Resources and Employee Benfeits and ServicesAlfred John TolentinoPas encore d'évaluation

- CH 04Document9 pagesCH 04jaysonPas encore d'évaluation

- JO - AkzoNobel - Intern HSE HDocument2 pagesJO - AkzoNobel - Intern HSE HudbarryPas encore d'évaluation

- DevelopmentThatPays Scrumban CheatSheet 3 - 0Document1 pageDevelopmentThatPays Scrumban CheatSheet 3 - 0Hamed KamelPas encore d'évaluation