Vous aimerez peut-être aussi

- Common Size Analysis CIPLA & Dr. Reddy's LabDocument8 pagesCommon Size Analysis CIPLA & Dr. Reddy's LabhahirePas encore d'évaluation

- Masters of Business Administration-Intelligent Data Science Academic Year: 2019-20Document21 pagesMasters of Business Administration-Intelligent Data Science Academic Year: 2019-20Tania PoddarPas encore d'évaluation

- Management & Financial AccountingDocument6 pagesManagement & Financial AccountingAnamitra SenPas encore d'évaluation

- This Study Resource Was: Level of ConsumptionDocument8 pagesThis Study Resource Was: Level of ConsumptionbumisriPas encore d'évaluation

- Financial Analysis of Indian Pharma Industry: Management Accounting ProjectDocument28 pagesFinancial Analysis of Indian Pharma Industry: Management Accounting ProjectRashmi RaniPas encore d'évaluation

- HUL N P&GDocument9 pagesHUL N P&GVikram KeswaniPas encore d'évaluation

- Indian DTH Industry: A Strategic Analysis: Dheeraj GirhotraDocument15 pagesIndian DTH Industry: A Strategic Analysis: Dheeraj GirhotraPratik JamsandekarPas encore d'évaluation

- Oscm AssignmentDocument2 pagesOscm AssignmentSakshi GuptaPas encore d'évaluation

- Financial Statement AnalysisDocument4 pagesFinancial Statement AnalysisHạnh PhạmPas encore d'évaluation

- Dr. Reddy's Annual Report 2008-09Document204 pagesDr. Reddy's Annual Report 2008-09biswajitdPas encore d'évaluation

- Financial Analysis of Cipla, Dr. Reddy and LupinDocument14 pagesFinancial Analysis of Cipla, Dr. Reddy and LupinParth GuptaPas encore d'évaluation

- Consumer BehaviourDocument6 pagesConsumer BehaviourDivya OgotiPas encore d'évaluation

- Management and Financial Accounting: (Assignment-2)Document10 pagesManagement and Financial Accounting: (Assignment-2)kashish Agarwal100% (1)

- HUL and P&GDocument19 pagesHUL and P&GRitesh KumarPas encore d'évaluation

- ABC Analysis in The Hospitality Sector: A Case Study: January 2017Document4 pagesABC Analysis in The Hospitality Sector: A Case Study: January 2017Sarello AssenavPas encore d'évaluation

- Basics of Digital Marketing - Unit 1 - WEEK 1Document3 pagesBasics of Digital Marketing - Unit 1 - WEEK 1Nostalgic NullPas encore d'évaluation

- Project: Case Study 1Document2 pagesProject: Case Study 1trishanuPas encore d'évaluation

- Law of Diminishing Manageral EconomicsDocument5 pagesLaw of Diminishing Manageral Economicsrajamech30Pas encore d'évaluation

- Individual AssignmentDocument4 pagesIndividual Assignmentsrinivas ceoPas encore d'évaluation

- HUL Vs P&GDocument17 pagesHUL Vs P&GManvi GoyalPas encore d'évaluation

- EpiPen CaseDocument5 pagesEpiPen CaseTanvi RastogiPas encore d'évaluation

- Financial Analysis - Assignment 1Document14 pagesFinancial Analysis - Assignment 1kashish AgarwalPas encore d'évaluation

- Cash Flow: Financial Management & AnalysisDocument3 pagesCash Flow: Financial Management & AnalysisVickytedPas encore d'évaluation

- SIC - Sunpharma Ranbaxy M&ADocument16 pagesSIC - Sunpharma Ranbaxy M&AAmitrojitPas encore d'évaluation

- HulDocument14 pagesHulAmit B0% (1)

- Business Report Assesment 2-1Document13 pagesBusiness Report Assesment 2-1VickytedPas encore d'évaluation

- E&I AssesmentDocument6 pagesE&I Assesmentgayathri rajanPas encore d'évaluation

- Group 6 Section A MKTMG Clean EdgeDocument5 pagesGroup 6 Section A MKTMG Clean EdgeAtri RoyPas encore d'évaluation

- Research Report - Dr. Reddy'sDocument8 pagesResearch Report - Dr. Reddy'sDishant KhanejaPas encore d'évaluation

- Conquering The Chaos PDFDocument3 pagesConquering The Chaos PDFiiuiuuiPas encore d'évaluation

- Management and Financial Accounting-Assessment - 2 VidharshanaDocument6 pagesManagement and Financial Accounting-Assessment - 2 Vidharshanavidharshana esakkiPas encore d'évaluation

- Discussion Forum - 2Document3 pagesDiscussion Forum - 2Srinivasan Narasimman100% (1)

- Pestel Analysis of UnileverDocument37 pagesPestel Analysis of UnileverAnas khanPas encore d'évaluation

- Dr. Reddy's Lab - New Product PromotionDocument30 pagesDr. Reddy's Lab - New Product PromotionGauravPandeyPas encore d'évaluation

- SYBMS Case StudyDocument3 pagesSYBMS Case StudyKarishma SarodePas encore d'évaluation

- Apple Iphone Life Cycle ManagementDocument8 pagesApple Iphone Life Cycle Managementrazvan6b49Pas encore d'évaluation

- Assessment - 1 - Pfizer & Sunpharma - Group 09Document4 pagesAssessment - 1 - Pfizer & Sunpharma - Group 09AnanthkrishnanPas encore d'évaluation

- Assignment On Business PlanDocument28 pagesAssignment On Business PlanFauzia AfrozaPas encore d'évaluation

- MFA Assessment 1Document6 pagesMFA Assessment 1rajeshkinger_1994Pas encore d'évaluation

- Cepton Strategic Outsourcing Across The Pharmaceuticals Value ChainDocument9 pagesCepton Strategic Outsourcing Across The Pharmaceuticals Value ChainFrenzy FrenesisPas encore d'évaluation

- This Study Resource Was: Sathish L RDocument7 pagesThis Study Resource Was: Sathish L RBhoomi GoyalPas encore d'évaluation

- 3.strategic Management Q 9,10,11Document4 pages3.strategic Management Q 9,10,11AnanthkrishnanPas encore d'évaluation

- Brand Quiz 3Document2 pagesBrand Quiz 3Dr. Shailendra Kumar SrivastavaPas encore d'évaluation

- CBSE CLass 10 Mathematics Standard Answer Key 2023 Set 1 30 4 1Document23 pagesCBSE CLass 10 Mathematics Standard Answer Key 2023 Set 1 30 4 1A KennedyPas encore d'évaluation

- DADM Q7,8 and 9 ReportDocument4 pagesDADM Q7,8 and 9 ReportgreatlakesPas encore d'évaluation

- Clean Edge Razor-Case PPT-SHAREDDocument10 pagesClean Edge Razor-Case PPT-SHAREDPoorvi SinghalPas encore d'évaluation

- MedicinMan - November 2012Document27 pagesMedicinMan - November 2012Anup Soans100% (1)

- Brand Extension For BisleriDocument16 pagesBrand Extension For BisleriPratik SoniPas encore d'évaluation

- Healthcare Jan 2019Document34 pagesHealthcare Jan 2019kiranPas encore d'évaluation

- Business Statistics Project 2010Document21 pagesBusiness Statistics Project 2010Aayush AkhauriPas encore d'évaluation

- An Organization Study at Strides Pharma Limited 2Document59 pagesAn Organization Study at Strides Pharma Limited 2Harshith KPas encore d'évaluation

- SMM NotesDocument139 pagesSMM NotesALIEPas encore d'évaluation

- CRISIL Research - Ier Report Apollo Hospitals Enterprise LTD 2016Document32 pagesCRISIL Research - Ier Report Apollo Hospitals Enterprise LTD 2016Vivek AnandanPas encore d'évaluation

- Entreprenuership AssignmentDocument15 pagesEntreprenuership AssignmentBhavyata VermaPas encore d'évaluation

- Product and Brand ManagementDocument19 pagesProduct and Brand ManagementayushdixitPas encore d'évaluation

- Research Insights 2 Infosys LimitedDocument6 pagesResearch Insights 2 Infosys Limited2K20DMBA53 Jatin suriPas encore d'évaluation

- Sun Pharma ReportDocument10 pagesSun Pharma ReportVijayalakshmi Kannan100% (1)

- AOL.com (Review and Analysis of Swisher's Book)D'EverandAOL.com (Review and Analysis of Swisher's Book)Pas encore d'évaluation

- Meet Mate INTM ProjectDocument22 pagesMeet Mate INTM ProjectSrikanth Kumar KonduriPas encore d'évaluation

- FSABV Final ReportDocument3 pagesFSABV Final ReportSrikanth Kumar KonduriPas encore d'évaluation

- Final PPT of MarutiDocument21 pagesFinal PPT of MarutiSrikanth Kumar KonduriPas encore d'évaluation

- Wintel AnalysisDocument11 pagesWintel AnalysisSrikanth Kumar Konduri100% (2)

- Panel Data Analysis: Indian Pharmacy IndustryDocument11 pagesPanel Data Analysis: Indian Pharmacy IndustrySrikanth Kumar KonduriPas encore d'évaluation

- LPO in IndiaDocument14 pagesLPO in IndiaSrikanth Kumar KonduriPas encore d'évaluation

- IB - Doing Business in China - 2011Document27 pagesIB - Doing Business in China - 2011Srikanth Kumar KonduriPas encore d'évaluation

- Trading StrategyDocument1 pageTrading StrategySrikanth Kumar KonduriPas encore d'évaluation

- BC-2 Interaction With Foreign ClientsDocument24 pagesBC-2 Interaction With Foreign ClientsSrikanth Kumar KonduriPas encore d'évaluation

- UK - SureInsureDocument14 pagesUK - SureInsureSrikanth Kumar KonduriPas encore d'évaluation

- Cipla Vs Dr1Document10 pagesCipla Vs Dr1Srikanth Kumar KonduriPas encore d'évaluation

- Portfolio Management of Reliance SecuritiesDocument29 pagesPortfolio Management of Reliance SecuritiesVasavi DaramPas encore d'évaluation

- Beaver, W 1968. The Information Content of Annual Earnings AnnouncementsDocument15 pagesBeaver, W 1968. The Information Content of Annual Earnings Announcementsgagakatalaga100% (1)

- Iloilo Bid Bulletin and Requirement ChecklistDocument11 pagesIloilo Bid Bulletin and Requirement ChecklistRamil S. ArtatesPas encore d'évaluation

- Bond & Interest Rates - The 54 Year CycleDocument19 pagesBond & Interest Rates - The 54 Year CycleElliott Wave Technician100% (1)

- S&C - Candlesticks and Intraday Market Analysis PDFDocument14 pagesS&C - Candlesticks and Intraday Market Analysis PDFAntonio ZikosPas encore d'évaluation

- Lecture16 PDFDocument30 pagesLecture16 PDFkate ngPas encore d'évaluation

- Cooperative BookkeepingDocument41 pagesCooperative Bookkeepingjaydeeado50% (4)

- Hull OFOD11 e Solutions CH 03Document6 pagesHull OFOD11 e Solutions CH 03Vaibhav KocharPas encore d'évaluation

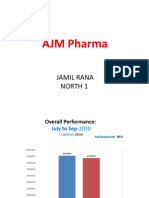

- AJM Pharma: Jamil Rana North 1Document18 pagesAJM Pharma: Jamil Rana North 1Adil ShahzadPas encore d'évaluation

- ForexSecrets15min enDocument19 pagesForexSecrets15min enAtif ChaudhryPas encore d'évaluation

- Jodhpur Vidyut Vitaran Nigam Limited A Govt. of Rajasthan Undertaking (For E-Tendering)Document19 pagesJodhpur Vidyut Vitaran Nigam Limited A Govt. of Rajasthan Undertaking (For E-Tendering)Santhosh V RaajendiranPas encore d'évaluation

- Kieso 15ed Chapter 23 PresentationDocument79 pagesKieso 15ed Chapter 23 PresentationIdioms100% (1)

- Primer 2015Document18 pagesPrimer 2015pierrefrancPas encore d'évaluation

- Formative Test in Stocks and BondsDocument1 pageFormative Test in Stocks and Bondsarris sulitPas encore d'évaluation

- Evolution of Insider TradingDocument6 pagesEvolution of Insider TradingVicente Rodriguez ArandaPas encore d'évaluation

- Commerce & Management Pre-Ph.D SyllabiDocument16 pagesCommerce & Management Pre-Ph.D SyllabiSugan PragasamPas encore d'évaluation

- London Stock ExchangeDocument37 pagesLondon Stock ExchangeJyasmine Aura V. Agustin100% (1)

- Private Impact ArtifactsDocument5 pagesPrivate Impact ArtifactsCaua MarcondesPas encore d'évaluation

- Development of The Institutional Structure of Financial AccountingDocument23 pagesDevelopment of The Institutional Structure of Financial AccountingfirmanPas encore d'évaluation

- Gillette Pakistan Limited: Analysis of Financial StatementDocument19 pagesGillette Pakistan Limited: Analysis of Financial StatementElhemJavedPas encore d'évaluation

- The Value of An Option To Exchange One Asset For Another - Margrabe PDFDocument10 pagesThe Value of An Option To Exchange One Asset For Another - Margrabe PDFArlette_rlzPas encore d'évaluation

- Credit Suisse-Escenarios para La ArgentinaDocument8 pagesCredit Suisse-Escenarios para La ArgentinaCronista.comPas encore d'évaluation

- Chapter 11 Fundamental AnalysisDocument37 pagesChapter 11 Fundamental AnalysisSamuel DwumfourPas encore d'évaluation

- Phil. Trust Co. v. Rivera, 44 Phil. 469 (1923)Document4 pagesPhil. Trust Co. v. Rivera, 44 Phil. 469 (1923)inno KalPas encore d'évaluation

- Tata Power HistoryDocument14 pagesTata Power Historyvinit2801Pas encore d'évaluation

- Bond ValuationDocument50 pagesBond Valuationrenu3rdjanPas encore d'évaluation

- Thesis Summary Week 8Document3 pagesThesis Summary Week 8api-278033882Pas encore d'évaluation

- The Philippine Stock ExchangeDocument3 pagesThe Philippine Stock ExchangeJay Gallardo AmadorPas encore d'évaluation

- Btx2000 Week 2 自改1 Tutorial QuestionDocument3 pagesBtx2000 Week 2 自改1 Tutorial Question朱潇妤Pas encore d'évaluation

- Mutual Funds Monthly February 2023 - YESSDocument6 pagesMutual Funds Monthly February 2023 - YESSAnkit PandePas encore d'évaluation