Vous aimerez peut-être aussi

- IBM ProjectDocument77 pagesIBM ProjectakshatPas encore d'évaluation

- Step by Step Process For Material Master ArchivingDocument20 pagesStep by Step Process For Material Master ArchivingV K Mohan PuppalaPas encore d'évaluation

- AMME5912 Assignment 3Document12 pagesAMME5912 Assignment 3Duc TuPas encore d'évaluation

- 242 Assignment 1 Interview ProtocolDocument6 pages242 Assignment 1 Interview ProtocolMarlo Anthony BurgosPas encore d'évaluation

- Mortality Schedule of 1961, 1976, 1996 and 2016: Age GroupDocument4 pagesMortality Schedule of 1961, 1976, 1996 and 2016: Age Groupcindy lamPas encore d'évaluation

- Excel Skills - Cashbook & Bank Reconciliation Template: InstructionsDocument28 pagesExcel Skills - Cashbook & Bank Reconciliation Template: InstructionsSaghirPas encore d'évaluation

- Flipkart Labels 18 Oct 2022-10-48Document5 pagesFlipkart Labels 18 Oct 2022-10-48Sahil KochharPas encore d'évaluation

- BPR Analysis of Helpdesk ProcessDocument25 pagesBPR Analysis of Helpdesk ProcessSimon Ruoro100% (1)

- SC 20220816-2022916Document5 pagesSC 20220816-2022916Line XiaoPas encore d'évaluation

- Research 1Document17 pagesResearch 1yrriuPas encore d'évaluation

- MM Introduction Material MasterDocument18 pagesMM Introduction Material MasterRamesh ReddyPas encore d'évaluation

- Bpo CSR - Bpo PerspectiveDocument10 pagesBpo CSR - Bpo PerspectiveyogasanaPas encore d'évaluation

- Functional Requirements Matrix - Accounts PayableDocument58 pagesFunctional Requirements Matrix - Accounts PayableEden Solutions LtdPas encore d'évaluation

- Maru - Application of The Mckinsey 7s Model in StrategyDocument59 pagesMaru - Application of The Mckinsey 7s Model in StrategyNawacita KonsultanPas encore d'évaluation

- Policy Guidelines HDFCDocument3 pagesPolicy Guidelines HDFCkwangdidPas encore d'évaluation

- BP AFS Function ListDocument10 pagesBP AFS Function Listsubandiwahyudi08Pas encore d'évaluation

- 6a Prepare and Process Banking DocumentsDocument3 pages6a Prepare and Process Banking Documentsapi-27922856750% (2)

- Introduction To Islamic Finance QuizDocument3 pagesIntroduction To Islamic Finance QuizSaad Nadeem 090100% (4)

- Business Process Re Engineering at Exim Bank LTDDocument17 pagesBusiness Process Re Engineering at Exim Bank LTDFred Raphael IlomoPas encore d'évaluation

- Business Maths Cha - 1Document45 pagesBusiness Maths Cha - 1Bereket ZerihunPas encore d'évaluation

- Direct Deposit TutorialDocument10 pagesDirect Deposit TutorialKabano Co100% (1)

- Financial Performance Evaluation PDFDocument109 pagesFinancial Performance Evaluation PDFshahulsuccess100% (1)

- Case Study ToyotaDocument5 pagesCase Study ToyotaMugi Sahadevan100% (1)

- Message File Report HeaderDocument2 pagesMessage File Report HeaderYash EmrithPas encore d'évaluation

- Use Case Diagrams (SDLab)Document15 pagesUse Case Diagrams (SDLab)Aravindha Kumar100% (1)

- Cash and Receivables ReviewDocument45 pagesCash and Receivables ReviewAdul Luda100% (1)

- Banking Website SynopsisDocument8 pagesBanking Website SynopsisAbodh KumarPas encore d'évaluation

- NP WD 2-1 TarinSearleDocument2 pagesNP WD 2-1 TarinSearleTarin SearlePas encore d'évaluation

- DB2 9.7 For LUW New Feature - Index CompressionDocument26 pagesDB2 9.7 For LUW New Feature - Index Compressionandrey_krasovskyPas encore d'évaluation

- Diploma in Management: Interpersonal CommunicationDocument15 pagesDiploma in Management: Interpersonal CommunicationAIMAN ISKANDAR BIN AZMAN SHAH STUDENTPas encore d'évaluation

- AFM 273 F2021 Midterm W AnswersDocument31 pagesAFM 273 F2021 Midterm W AnswersAustin BijuPas encore d'évaluation

- Hotel Management System and Their Modern ApproachesDocument7 pagesHotel Management System and Their Modern ApproachesInternational Journal of Innovative Science and Research TechnologyPas encore d'évaluation

- Online Hotel Management System Synopsis ReportDocument33 pagesOnline Hotel Management System Synopsis Reportbatman2407Pas encore d'évaluation

- CV YohannesDocument5 pagesCV YohannesYohannis AshagrewPas encore d'évaluation

- Financial Documentation FormDocument2 pagesFinancial Documentation FormjusttrickingPas encore d'évaluation

- Agreement To Be Printed On Stamp Paper: Agreement For Undertaking Collaborative R&D ProjectDocument47 pagesAgreement To Be Printed On Stamp Paper: Agreement For Undertaking Collaborative R&D ProjectPreding M MarakPas encore d'évaluation

- It Student / Junior Developer: Kasetsart University, 2015 Bangkok, ThailandDocument2 pagesIt Student / Junior Developer: Kasetsart University, 2015 Bangkok, ThailandNantawan GantongPas encore d'évaluation

- Accounts Receivable Management ExplainedDocument12 pagesAccounts Receivable Management ExplainedPurushottam KumarPas encore d'évaluation

- Adjusting Entries and Adjusted Trial BalanceDocument8 pagesAdjusting Entries and Adjusted Trial Balancetgibson621Pas encore d'évaluation

- PHI 17A-Dec 2018 PAL Fin Statement 2018Document162 pagesPHI 17A-Dec 2018 PAL Fin Statement 2018makane100% (1)

- Intermediate Microeconomics Recitation Material Key ConceptsDocument10 pagesIntermediate Microeconomics Recitation Material Key ConceptsstudiessPas encore d'évaluation

- Copy-Forms & Formats For Bell Desk OperationDocument8 pagesCopy-Forms & Formats For Bell Desk OperationINFO STATIONERSPas encore d'évaluation

- A Study On Prospects and Challenges of Mobile Banking in IndiaDocument10 pagesA Study On Prospects and Challenges of Mobile Banking in IndiaAkshay PawarPas encore d'évaluation

- Advantages and Disadvantages of Online BankingDocument10 pagesAdvantages and Disadvantages of Online Bankingamir_saheedPas encore d'évaluation

- SQL Practice Exercises RelevanceDocument4 pagesSQL Practice Exercises RelevanceNUBG GamerPas encore d'évaluation

- Contact Details: BSP DirectoryDocument4 pagesContact Details: BSP DirectoryPondo AsensoPas encore d'évaluation

- Certificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)Document52 pagesCertificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)jeaniePas encore d'évaluation

- Merchant Banking An OverviewDocument23 pagesMerchant Banking An OverviewSushant Kumar MishraPas encore d'évaluation

- Vice President Director Tax in NYC Resume Peter MohanDocument2 pagesVice President Director Tax in NYC Resume Peter MohanPeterMohanPas encore d'évaluation

- Effect of Accounting Information System On Financial Performance of FirmsDocument3 pagesEffect of Accounting Information System On Financial Performance of FirmsAytenfisu YehualashetPas encore d'évaluation

- Feasibility StudyDocument1 pageFeasibility Studykalu420Pas encore d'évaluation

- Ferrer-Study Notes-Chapter 4Document4 pagesFerrer-Study Notes-Chapter 4Ciara FerrerPas encore d'évaluation

- A Study On Factors Influencing Finance Business Partnering Capabilities For Improved Organisational PerformanceDocument125 pagesA Study On Factors Influencing Finance Business Partnering Capabilities For Improved Organisational PerformanceArchchana Vek Suren100% (1)

- Resume Sample Financial ManagementDocument2 pagesResume Sample Financial ManagementSitiSyawaliaPas encore d'évaluation

- 1 PDFDocument9 pages1 PDFAriane Mae VillarealPas encore d'évaluation

- 10 General Interview QuestionsDocument6 pages10 General Interview QuestionsIvan Jggc - ccPas encore d'évaluation

- Managing Creativity and InnovationDocument15 pagesManaging Creativity and InnovationAdnan HadziibrahimovicPas encore d'évaluation

- E-Commerce File, Amritpal, 6th SemDocument33 pagesE-Commerce File, Amritpal, 6th Semrohit singh100% (1)

- Hospital Management SystemDocument4 pagesHospital Management Systemirfan_chand_mianPas encore d'évaluation

- 01 - Clearing ActivtiesDocument14 pages01 - Clearing ActivtiesBarjesh_Lamba_2009Pas encore d'évaluation

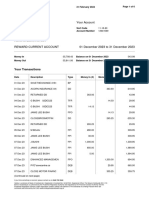

- Account Statement From 1 Jan 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 1 Jan 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceManishDikshitPas encore d'évaluation

- Stakeholder AnalysisDocument20 pagesStakeholder AnalysisTesfaye Noko100% (1)

- Bps CV Healthcare ITDocument4 pagesBps CV Healthcare ITBadariprashanth SastryPas encore d'évaluation

- Data Mining Is A Business Process For Exploring Large Amounts of Data To Discover Meaningful Patterns and RulesDocument4 pagesData Mining Is A Business Process For Exploring Large Amounts of Data To Discover Meaningful Patterns and Rulesfindurvoice2003100% (1)

- Sies School of Business Studies, Nerul, Navi Mumbai - 400 706Document3 pagesSies School of Business Studies, Nerul, Navi Mumbai - 400 706PutinPas encore d'évaluation

- BPR Overview: Reengineering Business ProcessesDocument48 pagesBPR Overview: Reengineering Business ProcessesvjranajPas encore d'évaluation

- Online Matrimony PortalDocument13 pagesOnline Matrimony PortalGargy ShekharPas encore d'évaluation

- 67 - Sylabus Final - 1st SemesterDocument71 pages67 - Sylabus Final - 1st SemesterGargy ShekharPas encore d'évaluation

- Brand Strategies - Dabur India: Submitted ToDocument8 pagesBrand Strategies - Dabur India: Submitted ToGargy ShekharPas encore d'évaluation

- Withdrawal Register 2020Document65 pagesWithdrawal Register 2020Ellastrous Gogo NathanPas encore d'évaluation

- SWOT and Technical Analysis of Top Indian BanksDocument10 pagesSWOT and Technical Analysis of Top Indian BanksSahil DahiyaPas encore d'évaluation

- CH 3Document15 pagesCH 3Gizaw BelayPas encore d'évaluation

- Profitability Analysis of Sanima Bank Limited: A Project ReportDocument40 pagesProfitability Analysis of Sanima Bank Limited: A Project ReportSurya Satore0% (1)

- Vaish College of Education, Rohtak: PPT On BankingDocument10 pagesVaish College of Education, Rohtak: PPT On BankingSuraj NagpalPas encore d'évaluation

- September Payroll TransactionsDocument2 pagesSeptember Payroll Transactionsrizky ubaidillahPas encore d'évaluation

- 26th Floor, Annexe Block, Menara Takaful Malaysia, No 4, Jalan Sultan Sulaiman, 50000 Kuala Lumpur, P.O. Box 11483, 50746 Kuala LumpurDocument4 pages26th Floor, Annexe Block, Menara Takaful Malaysia, No 4, Jalan Sultan Sulaiman, 50000 Kuala Lumpur, P.O. Box 11483, 50746 Kuala LumpurIlove MiyamuraPas encore d'évaluation

- Management of Short Term Assets and Liabilities by P.rai87@gmailDocument22 pagesManagement of Short Term Assets and Liabilities by P.rai87@gmailPRAVEEN RAI100% (4)

- Challan Form SPSCDocument1 pageChallan Form SPSCFahad NaeemPas encore d'évaluation

- Banking Finance Tax Test SK2019 - 1Document4 pagesBanking Finance Tax Test SK2019 - 1Vishwas JPas encore d'évaluation

- Non-Banking Finance Companies in India's Financial LandscapeDocument18 pagesNon-Banking Finance Companies in India's Financial Landscapeshubham moonPas encore d'évaluation

- Chapter 6 - Business Transactions Their AnalysisDocument10 pagesChapter 6 - Business Transactions Their Analysisgeyb awayPas encore d'évaluation

- KDCC Bank ATM Debit Card ApplicationDocument4 pagesKDCC Bank ATM Debit Card ApplicationramPas encore d'évaluation

- I-Byte Banking March 2021Document86 pagesI-Byte Banking March 2021IT ShadesPas encore d'évaluation

- Deposit Insurance and Credit Guarantee Corporation Act 1961Document10 pagesDeposit Insurance and Credit Guarantee Corporation Act 1961Debayan GhoshPas encore d'évaluation

- Digital Banking in Indonesia: Building Loyalty and Generating GrowthDocument6 pagesDigital Banking in Indonesia: Building Loyalty and Generating GrowthPolitics RedefinedPas encore d'évaluation

- Fortune Institute of International Business: Team Project ON Citi GroupDocument12 pagesFortune Institute of International Business: Team Project ON Citi GroupRuchi SambhariaPas encore d'évaluation

- Debit Card Replacement and Regen of PIN MailerDocument1 pageDebit Card Replacement and Regen of PIN Mailerryan.asibautistaPas encore d'évaluation

- What is an NBFC MFI? Key processes and documentsDocument38 pagesWhat is an NBFC MFI? Key processes and documentsJashim AhammedPas encore d'évaluation

- Statement 12 2023Document6 pagesStatement 12 2023bgazi4888Pas encore d'évaluation

- The evolution of the Romanian banking system 2007-2015Document16 pagesThe evolution of the Romanian banking system 2007-2015TV Series RoPas encore d'évaluation

- KPMG Ory - Insights - 27 - October - 2023 - Rbi - Issues - Master - Direction - Non - Banking - Company - Scale - Based - RegulationDocument27 pagesKPMG Ory - Insights - 27 - October - 2023 - Rbi - Issues - Master - Direction - Non - Banking - Company - Scale - Based - RegulationRangerPas encore d'évaluation

- FM Charts by ICAI PDFDocument19 pagesFM Charts by ICAI PDFAditya Raut100% (1)

- W14494 PDF EngDocument6 pagesW14494 PDF EngJason RoyPas encore d'évaluation

- Shriram Transport Presentation December 2020Document50 pagesShriram Transport Presentation December 2020Gaurav BorsePas encore d'évaluation