Vous aimerez peut-être aussi

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Income Tax - 2 AssignmentDocument4 pagesIncome Tax - 2 AssignmentAnkit AgrawalPas encore d'évaluation

- Accounting Concepts Assignment August 2022Document5 pagesAccounting Concepts Assignment August 2022SoiniPas encore d'évaluation

- 11th Accountancy EM Half Yearly Exam 2023 Question Paper With Answer Keys Madurai District English Medium PDF DownloadDocument13 pages11th Accountancy EM Half Yearly Exam 2023 Question Paper With Answer Keys Madurai District English Medium PDF DownloadDr.ManogaranPas encore d'évaluation

- Fabm 1-PTDocument10 pagesFabm 1-PTClay MaaliwPas encore d'évaluation

- ch5 Test BankDocument41 pagesch5 Test BankTôn Nữ Hương GiangPas encore d'évaluation

- Financial Modeling of TCS LockDocument62 pagesFinancial Modeling of TCS LocksharadkulloliPas encore d'évaluation

- Dwnload Full Fundamental Accounting Principles Canadian Vol 1 Canadian 14th Edition Larson Solutions Manual PDFDocument35 pagesDwnload Full Fundamental Accounting Principles Canadian Vol 1 Canadian 14th Edition Larson Solutions Manual PDFexiguity.siroc.r1zj100% (13)

- Lecture 1Document23 pagesLecture 1John TomPas encore d'évaluation

- Din Textile MillsDocument41 pagesDin Textile MillsZainab Abizer MerchantPas encore d'évaluation

- 06 Activity 1Document9 pages06 Activity 1Sol Luna100% (3)

- Seat Work 02 - DingcongDocument3 pagesSeat Work 02 - DingcongJheilson S. DingcongPas encore d'évaluation

- Research Paper On Qualifying ActivitiesDocument48 pagesResearch Paper On Qualifying ActivitiesResearch and Development Tax Credit Magazine; David Greenberg PhD, MSA, EA, CPA; TGI; 646-705-2910100% (1)

- Chithambara College Past Students Association AccountsDocument61 pagesChithambara College Past Students Association Accountsapi-140426513Pas encore d'évaluation

- Best Practices in Hotel Financial ManagementDocument3 pagesBest Practices in Hotel Financial ManagementDhruv BansalPas encore d'évaluation

- AG Office AccountingDocument165 pagesAG Office AccountingabadeshPas encore d'évaluation

- 1120s PDFDocument5 pages1120s PDFBreann MorrisPas encore d'évaluation

- M5&M6 SC - Other AJE & WorksheetDocument47 pagesM5&M6 SC - Other AJE & WorksheetLady Ysabel HechanovaPas encore d'évaluation

- Tally AssignmentDocument9 pagesTally AssignmentShivam GuptaPas encore d'évaluation

- PNG Rules 2008Document30 pagesPNG Rules 2008sunshine dreamPas encore d'évaluation

- Lesson No. 3: Cities of Mandaluyong and PasigDocument37 pagesLesson No. 3: Cities of Mandaluyong and PasigRenelle Habac100% (1)

- Financial Statements As at 31st Dec, 2019 - 0 PDFDocument1 pageFinancial Statements As at 31st Dec, 2019 - 0 PDFMsuyaPas encore d'évaluation

- Accounting Business Case 2Document6 pagesAccounting Business Case 2doshizzlePas encore d'évaluation

- Case StudyDocument34 pagesCase Studymarksman_para90% (10)

- Tcode Favorites Sap AaDocument10 pagesTcode Favorites Sap AaKrali MarkoPas encore d'évaluation

- Axis Bank AR 2021-22 - Standalone Financial StatementsDocument81 pagesAxis Bank AR 2021-22 - Standalone Financial StatementsMathar100% (1)

- Project ProposalDocument5 pagesProject ProposalJornie Duallo100% (1)

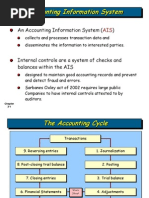

- Wiley - Chapter 3: The Accounting Information SystemDocument36 pagesWiley - Chapter 3: The Accounting Information SystemIvan BliminsePas encore d'évaluation

- Equities Cllase 1 Junio 2020Document209 pagesEquities Cllase 1 Junio 2020NGOC NHIPas encore d'évaluation

- Interactive Study Material Class-Xi Accountancy 2022-23Document86 pagesInteractive Study Material Class-Xi Accountancy 2022-23LafranPas encore d'évaluation

- Chapter 4Document38 pagesChapter 4Haidee Sumampil67% (3)