Vous aimerez peut-être aussi

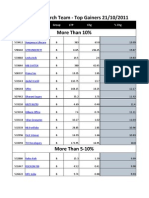

- A Group Top GainersDocument8 pagesA Group Top GainersMiserji MiserJiPas encore d'évaluation

- B Group GainersDocument6 pagesB Group GainersMiserji MiserJiPas encore d'évaluation

- A Group Top Gainers - 01/11/11Document3 pagesA Group Top Gainers - 01/11/11Miserji MiserJiPas encore d'évaluation

- A Group Top Gainers - 28/10/11 - Miserji Research DeskDocument3 pagesA Group Top Gainers - 28/10/11 - Miserji Research DeskMiserji MiserJiPas encore d'évaluation

- VisaDocument1 pageVisaMiserji MiserJiPas encore d'évaluation

- Mro TekDocument7 pagesMro TekMiserji MiserJiPas encore d'évaluation

- Shriram Epc LTD 241011 Sast1Document2 pagesShriram Epc LTD 241011 Sast1Miserji MiserJiPas encore d'évaluation

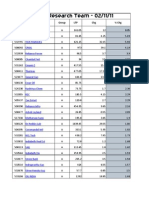

- Miserji Research Team: Scrip Code Company Group LTP CHG % CHGDocument7 pagesMiserji Research Team: Scrip Code Company Group LTP CHG % CHGMiserji MiserJiPas encore d'évaluation

- B Group Gainers - 28/10/11 - Miserji Research DeskDocument7 pagesB Group Gainers - 28/10/11 - Miserji Research DeskMiserji MiserJiPas encore d'évaluation

- Onmobile Buyback AdDocument1 pageOnmobile Buyback AdMiserji MiserJiPas encore d'évaluation

- AxisDocument1 pageAxisMiserji MiserJiPas encore d'évaluation

- Cholamandalam Investment and Finance Company LimitedDocument3 pagesCholamandalam Investment and Finance Company LimitedMiserji MiserJiPas encore d'évaluation

- Sat YamDocument2 pagesSat YamMiserji MiserJiPas encore d'évaluation

- Mukand LimitedDocument9 pagesMukand LimitedMiserji MiserJiPas encore d'évaluation

- Mahindra & Mahindra Financial Services LimitedDocument1 pageMahindra & Mahindra Financial Services LimitedMiserji MiserJiPas encore d'évaluation

- Grabal - CourtNotice - 25102011Document24 pagesGrabal - CourtNotice - 25102011Miserji MiserJiPas encore d'évaluation

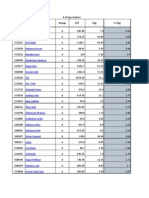

- A Group Gainers Top GainersDocument4 pagesA Group Gainers Top GainersMiserji MiserJiPas encore d'évaluation

- Gitanjali Gems LimitedDocument1 pageGitanjali Gems LimitedMiserji MiserJiPas encore d'évaluation

- Sonata Press Release - Miserji Research DeskDocument3 pagesSonata Press Release - Miserji Research DeskMiserji MiserJiPas encore d'évaluation

- THANGAMAYL - Miserji Research TeamDocument1 pageTHANGAMAYL - Miserji Research TeamMiserji MiserJiPas encore d'évaluation

- Union Bank of India1 241011Document2 pagesUnion Bank of India1 241011Miserji MiserJiPas encore d'évaluation

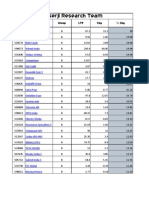

- B Group GainersDocument5 pagesB Group GainersMiserji MiserJiPas encore d'évaluation

- Miserji Research DeskDocument3 pagesMiserji Research DeskMiserji MiserJiPas encore d'évaluation

- Miserji Research DeskDocument3 pagesMiserji Research DeskMiserji MiserJiPas encore d'évaluation

- BajajCorp Updts 24102011Document30 pagesBajajCorp Updts 24102011Miserji MiserJiPas encore d'évaluation

- Miserji Research DeskDocument2 pagesMiserji Research DeskMiserji MiserJiPas encore d'évaluation

- WWIL Reg 24102011Document5 pagesWWIL Reg 24102011Miserji MiserJiPas encore d'évaluation

- WWIL Reg 24102011Document5 pagesWWIL Reg 24102011Miserji MiserJiPas encore d'évaluation

- Nse Timings - 24 - Oct - 2011Document4 pagesNse Timings - 24 - Oct - 2011Miserji MiserJiPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- VMD Tech Systems PVT LTDDocument41 pagesVMD Tech Systems PVT LTDrohiniPas encore d'évaluation

- Ultratech Annual ReportDocument49 pagesUltratech Annual ReportMax ScanPas encore d'évaluation

- Titan Company Ltd. (India) : SourceDocument6 pagesTitan Company Ltd. (India) : SourceDivyagarapatiPas encore d'évaluation

- Accsys Group Annual Report 2017Document116 pagesAccsys Group Annual Report 2017sharkl123Pas encore d'évaluation

- Lecture 33 Credit+Analysis+-+Corporate+Credit+Analysis+ (Ratios)Document33 pagesLecture 33 Credit+Analysis+-+Corporate+Credit+Analysis+ (Ratios)Taan100% (1)

- Horizontal & Vertical Analysis of Maruti Suzuki India LtdDocument17 pagesHorizontal & Vertical Analysis of Maruti Suzuki India LtdBerkshire Hathway coldPas encore d'évaluation

- Bayer Annual Report 2013Document351 pagesBayer Annual Report 2013Barath R BaskaranPas encore d'évaluation

- ADRO 20190408 - Laporan Tahunan 2018 - Web PDFDocument415 pagesADRO 20190408 - Laporan Tahunan 2018 - Web PDFKomiker MangaPas encore d'évaluation

- Working Capital Terminology Primer SNC WC SimulationDocument2 pagesWorking Capital Terminology Primer SNC WC SimulationMohit SahPas encore d'évaluation

- ADF Foods Limited - Report - 17th June 2008 - DhananjayanDocument2 pagesADF Foods Limited - Report - 17th June 2008 - Dhananjayanapi-3702531Pas encore d'évaluation

- Fixed cost analysis and break even calculation with sales growth projectionsDocument8 pagesFixed cost analysis and break even calculation with sales growth projectionsEvelyn MonzonPas encore d'évaluation

- Gallagher 5e.c4Document27 pagesGallagher 5e.c4Stacy LanierPas encore d'évaluation

- Lecture 1A Introduction and Understanding Cash FlowsDocument20 pagesLecture 1A Introduction and Understanding Cash FlowsJohnPas encore d'évaluation

- New Heritage Doll Company Financial AnalysisDocument31 pagesNew Heritage Doll Company Financial AnalysisSoundarya AbiramiPas encore d'évaluation

- Finance 351 NotesDocument14 pagesFinance 351 NotesCindy YinPas encore d'évaluation

- Company X forecasts financial impact of launching mobile handset leasing plansDocument10 pagesCompany X forecasts financial impact of launching mobile handset leasing plansbura100% (1)

- Valuing and Acquiring A Business: Hawawini & Viallet 1Document53 pagesValuing and Acquiring A Business: Hawawini & Viallet 1Kishore ReddyPas encore d'évaluation

- Revenue Recognition Challenges For Disruptive InnovationDocument21 pagesRevenue Recognition Challenges For Disruptive InnovationRishiraj Sisodiya100% (1)

- TB CHDocument44 pagesTB CHMai PhamPas encore d'évaluation

- Crisis and Debt Restructuring at Kingfisher AirlinesDocument5 pagesCrisis and Debt Restructuring at Kingfisher AirlinesAnk's SinghPas encore d'évaluation

- Annual Report Samindo Final 2014 (MYOH)Document129 pagesAnnual Report Samindo Final 2014 (MYOH)Siti Nur KomalaPas encore d'évaluation

- Equidam Valuation Report SampleDocument17 pagesEquidam Valuation Report SampleKram Jam100% (1)

- EFM Classic Business Free TrialDocument290 pagesEFM Classic Business Free TrialadildastiPas encore d'évaluation

- CH 5.palepuDocument34 pagesCH 5.palepuRavi OlaPas encore d'évaluation

- Financial Analysis of ONGCDocument70 pagesFinancial Analysis of ONGCBhavya100% (6)

- Asian Electronics LimitedDocument14 pagesAsian Electronics Limiteddownloadman1973Pas encore d'évaluation

- Strategic Assignment - EtihadDocument115 pagesStrategic Assignment - EtihadGeorgiana BiancaPas encore d'évaluation

- How Companies Can Flourish After a RecessionDocument14 pagesHow Companies Can Flourish After a RecessionJack HuseynliPas encore d'évaluation

- Conference Call Results January - September 2014: WelcomeDocument21 pagesConference Call Results January - September 2014: WelcomeToni HercegPas encore d'évaluation

- Mercury Athletic Historical Income StatementsDocument18 pagesMercury Athletic Historical Income StatementskarthikawarrierPas encore d'évaluation