Vous aimerez peut-être aussi

- Lec 10 - Dealers and Liquid Security MarketsDocument7 pagesLec 10 - Dealers and Liquid Security MarketsDaniel 'Ted' UrdanetaPas encore d'évaluation

- Referencias Bibliográficas Trabajo Especial de Grado - Daniel UrdanetaDocument2 pagesReferencias Bibliográficas Trabajo Especial de Grado - Daniel UrdanetaDaniel 'Ted' UrdanetaPas encore d'évaluation

- Pozsar, Adrian, Ashcraft & Boetsky, "Shadow Banking" (Federal Reserve Bank of New York Staff Reports, #458, July 2010)Document38 pagesPozsar, Adrian, Ashcraft & Boetsky, "Shadow Banking" (Federal Reserve Bank of New York Staff Reports, #458, July 2010)Daniel 'Ted' UrdanetaPas encore d'évaluation

- Seignorage, Money Supply and InflationDocument8 pagesSeignorage, Money Supply and InflationSukumar Nandi100% (2)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Holocaust Ed LRB 2308 P 4Document4 pagesHolocaust Ed LRB 2308 P 4Webster MilwaukeePas encore d'évaluation

- Ang Tibay Vs CIRDocument2 pagesAng Tibay Vs CIRNyx PerezPas encore d'évaluation

- JAIME GAPAYAO vs. JAIME FULODocument3 pagesJAIME GAPAYAO vs. JAIME FULOBert NazarioPas encore d'évaluation

- CONSOLIDATED Journal of Proceedings 2nd Regular Session 1 11 24Document20 pagesCONSOLIDATED Journal of Proceedings 2nd Regular Session 1 11 24Mark HenryPas encore d'évaluation

- Board of Ed Agendas 2009 - 2010Document9 pagesBoard of Ed Agendas 2009 - 2010Hob151219!Pas encore d'évaluation

- Nestle Political Contribution BreakdownDocument6 pagesNestle Political Contribution BreakdownJulio Ricardo VarelaPas encore d'évaluation

- NTACSIR AdmitCardDocument1 pageNTACSIR AdmitCardVikram kumar0% (1)

- SEIP Trainee Admission FormDocument2 pagesSEIP Trainee Admission FormRj IsratPas encore d'évaluation

- Mircea DinescuDocument3 pagesMircea DinescuMironel VasilePas encore d'évaluation

- The Right To Information ActDocument10 pagesThe Right To Information ActsimranPas encore d'évaluation

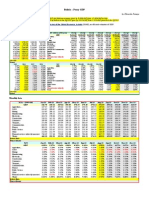

- Bolivia - Proxy GDPDocument1 pageBolivia - Proxy GDPEduardo PetazzePas encore d'évaluation

- Rizal - Chapter 2ADocument28 pagesRizal - Chapter 2ARomePas encore d'évaluation

- Final Report Mapping Update 2015-En PDFDocument63 pagesFinal Report Mapping Update 2015-En PDFImran JahanPas encore d'évaluation

- The King Alfred Plan (BKA) Rex 84Document5 pagesThe King Alfred Plan (BKA) Rex 84Mosi Ngozi (fka) james harris100% (5)

- Northern Luzon Command: AFP Vision 2028: A World-Class Armed Forces, Source of National PrideDocument2 pagesNorthern Luzon Command: AFP Vision 2028: A World-Class Armed Forces, Source of National PrideYelle LacernaPas encore d'évaluation

- Case Digest Tano v. Socrates G.R. No. 110249. August 21 1997Document2 pagesCase Digest Tano v. Socrates G.R. No. 110249. August 21 1997Winnie Ann Daquil Lomosad100% (5)

- National Officers Academy: Mock Exams Special CSS & CSS-2024 August 2023 (Mock-5) International Relations, Paper-IiDocument1 pageNational Officers Academy: Mock Exams Special CSS & CSS-2024 August 2023 (Mock-5) International Relations, Paper-IiKiranPas encore d'évaluation

- Department of Human Settlements and Urban Development: Kagawaran NG Pananahanang Pantao at Pagpapaunlad NG KalunsuranDocument11 pagesDepartment of Human Settlements and Urban Development: Kagawaran NG Pananahanang Pantao at Pagpapaunlad NG KalunsuranjabahPas encore d'évaluation

- Lakemont Shores POA Bylaws As of 2005Document11 pagesLakemont Shores POA Bylaws As of 2005PAAWS2Pas encore d'évaluation

- Name: Floranne Mar Luklukan Subject: Lie Detection Techniques Section: BSCRIM D2018 Date July 30 2021Document4 pagesName: Floranne Mar Luklukan Subject: Lie Detection Techniques Section: BSCRIM D2018 Date July 30 2021Joshua PatiuPas encore d'évaluation

- Dizon Vs EduardoDocument25 pagesDizon Vs EduardoBerPas encore d'évaluation

- John F. Kennedy's Speeches 1947-1963Document934 pagesJohn F. Kennedy's Speeches 1947-1963Brian Keith Haskins100% (1)

- Facts:: 9. Tomali V Civil Service CommissionDocument3 pagesFacts:: 9. Tomali V Civil Service CommissionEmmanuelMedinaJr.Pas encore d'évaluation

- List of Shortlisted Candidates For DSSC 27 Selection BoardDocument12 pagesList of Shortlisted Candidates For DSSC 27 Selection BoardBinde PonlePas encore d'évaluation

- Application For Intimation and Transfer of Ownership of A Motor VehicleDocument3 pagesApplication For Intimation and Transfer of Ownership of A Motor VehicleAnanth KrishnaPas encore d'évaluation

- Section 54. Approval of Ordinances. - : Sangguniang PanlalawiganDocument3 pagesSection 54. Approval of Ordinances. - : Sangguniang PanlalawiganDroidlyfPas encore d'évaluation

- PhilosophyDocument51 pagesPhilosophykenPas encore d'évaluation

- Austin Residents Sue City Over Code Next PetitionDocument8 pagesAustin Residents Sue City Over Code Next PetitionAnonymous Pb39klJPas encore d'évaluation

- HT Chandigarh - (2019-08-17)Document68 pagesHT Chandigarh - (2019-08-17)Mohd AbbasPas encore d'évaluation

- KCS - Revised Pay - Rules, 2012 PDFDocument28 pagesKCS - Revised Pay - Rules, 2012 PDFNelvin RoyPas encore d'évaluation