Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Santander BankDocument8 pagesSantander BankJesus MartinezPas encore d'évaluation

- BB Bill Template - ScribdDocument3 pagesBB Bill Template - ScribdSomansh Kumar100% (1)

- ABriefOverviewComparisonUCP600 ISP8 URDG 758 PDFDocument47 pagesABriefOverviewComparisonUCP600 ISP8 URDG 758 PDFmackjblPas encore d'évaluation

- Kashware DeckDocument14 pagesKashware DeckTushar VyasPas encore d'évaluation

- Nift ProposalDocument2 pagesNift Proposalmahrukh123Pas encore d'évaluation

- Statement of Account No:917010065595820 For The Period (From: 01-11-2018 To: 20-06-2019)Document3 pagesStatement of Account No:917010065595820 For The Period (From: 01-11-2018 To: 20-06-2019)Rakesh BabuPas encore d'évaluation

- Proforma I2 Cns CNR 25521526Document5 pagesProforma I2 Cns CNR 25521526piyushkatariya8Pas encore d'évaluation

- Accounting For Managers GTU Question PaperDocument3 pagesAccounting For Managers GTU Question PaperbhfunPas encore d'évaluation

- Project Finance-Dissertation ReportDocument2 pagesProject Finance-Dissertation ReportAhamed IbrahimPas encore d'évaluation

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancesamarth agrawalPas encore d'évaluation

- National Bank of Anguilla DeclDocument10 pagesNational Bank of Anguilla DeclChapter 11 DocketsPas encore d'évaluation

- Week 1 - Asset Classes and Financial MarketsDocument37 pagesWeek 1 - Asset Classes and Financial MarketsshanikaPas encore d'évaluation

- Intermediate Accounting Practice QuestionsDocument4 pagesIntermediate Accounting Practice QuestionsYsa Acupan100% (1)

- Gurleen Internship Report-6Document74 pagesGurleen Internship Report-6Joshua LoyalPas encore d'évaluation

- Financial Institutional Support To Exporters: Sidbi EXIM Bank EcgcDocument10 pagesFinancial Institutional Support To Exporters: Sidbi EXIM Bank EcgcAshvin RavriyaPas encore d'évaluation

- Measurement of Interest - SlidesDocument47 pagesMeasurement of Interest - SlidesSamir Arun BhucharPas encore d'évaluation

- 01 ProtectServer - Part I - Product OverviewDocument20 pages01 ProtectServer - Part I - Product OverviewmasanjayaPas encore d'évaluation

- Mohana Sangeetha RSecDocument3 pagesMohana Sangeetha RSecPrabuPas encore d'évaluation

- Business Finance Second QuarterDocument28 pagesBusiness Finance Second QuarterJessa GallardoPas encore d'évaluation

- Literature Review On Financial Performance of BanksDocument4 pagesLiterature Review On Financial Performance of BanksafdtzvbexPas encore d'évaluation

- PHILIPPINE EDUCATION CO., INC., Plaintiff-Appellant, vs. MAURICIO A. SORIANO, ET AL., Defendants-AppelleesDocument6 pagesPHILIPPINE EDUCATION CO., INC., Plaintiff-Appellant, vs. MAURICIO A. SORIANO, ET AL., Defendants-AppelleesKing BadongPas encore d'évaluation

- Financial Awareness Capsule For RRB Scale 2 2022 PDF by Ambitious BabaDocument119 pagesFinancial Awareness Capsule For RRB Scale 2 2022 PDF by Ambitious Bababhaskar kPas encore d'évaluation

- E Receipt For State Bank Collect PaymentDocument1 pageE Receipt For State Bank Collect PaymentPooja TripathiPas encore d'évaluation

- Simple InterestDocument27 pagesSimple Interestleslie0% (1)

- BFSM Unit IDocument30 pagesBFSM Unit IAbhinayaa SPas encore d'évaluation

- ACC106 - Project: Book of Prime EntryDocument20 pagesACC106 - Project: Book of Prime EntryAhmad Adam94% (16)

- BRM Term PaperDocument14 pagesBRM Term PaperAarti GulatiPas encore d'évaluation

- Bidensar 3Document2 pagesBidensar 3Adamou MFAMBOUPas encore d'évaluation

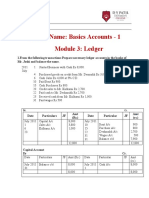

- Assignment Module 3 LedgerDocument3 pagesAssignment Module 3 LedgerPRINCE100% (1)