Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5782)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- In This Mini-Case You Will Complete The Preliminary Analytical Procedures For The 2016 Audit of Earthwear Clothiers, IncDocument6 pagesIn This Mini-Case You Will Complete The Preliminary Analytical Procedures For The 2016 Audit of Earthwear Clothiers, IncakjrflPas encore d'évaluation

- Logistic Performance MeasurementDocument17 pagesLogistic Performance Measurementpa JamalPas encore d'évaluation

- Audit Working PapersDocument5 pagesAudit Working PapersDlamini SiceloPas encore d'évaluation

- Baria Planning SolutionsDocument23 pagesBaria Planning SolutionsMonika Baheti50% (2)

- Just in TimeDocument7 pagesJust in Timewaqas08Pas encore d'évaluation

- Engg Project Management Lec1-2 (CASE Islamabad)Document108 pagesEngg Project Management Lec1-2 (CASE Islamabad)Rameez AnwarPas encore d'évaluation

- Globe Telecom Working CapitalDocument6 pagesGlobe Telecom Working CapitalPaulineBiroselPas encore d'évaluation

- Practice Exam 02 S04 312S05Document13 pagesPractice Exam 02 S04 312S05azirPas encore d'évaluation

- Managing Talent and Employee Performance AssessmentDocument12 pagesManaging Talent and Employee Performance AssessmentFerdiPas encore d'évaluation

- Example Rubric Case StudyDocument1 pageExample Rubric Case StudyGurinder ParmarPas encore d'évaluation

- Contract Review AgendaDocument34 pagesContract Review AgendaTheoPas encore d'évaluation

- Acct Statement XX2169 01102022Document22 pagesAcct Statement XX2169 01102022saurabh92prasadPas encore d'évaluation

- B.COM. (HONS.) PROGRAM AT MGKVDocument48 pagesB.COM. (HONS.) PROGRAM AT MGKVPahetuPas encore d'évaluation

- Chapter 1 AnswerDocument15 pagesChapter 1 AnswerKristina Kitty100% (1)

- Determining Exchange Ratio in MergersDocument2 pagesDetermining Exchange Ratio in MergersJyoti YadavPas encore d'évaluation

- Project On Bank of IndiaDocument56 pagesProject On Bank of IndiaJoanna HernandezPas encore d'évaluation

- Acca Paper P5 Advanced Performance Management Final Mock ExaminationDocument20 pagesAcca Paper P5 Advanced Performance Management Final Mock ExaminationMSA-ACCAPas encore d'évaluation

- Project Management For ManagersDocument22 pagesProject Management For ManagersBiswanathMudiPas encore d'évaluation

- Waterfall Model DocumentsDocument14 pagesWaterfall Model DocumentsNAMITA JHA100% (1)

- Management TheoryDocument65 pagesManagement TheoryPraveen ShuklaPas encore d'évaluation

- Exam History Transcript 5354100720293787408Document2 pagesExam History Transcript 5354100720293787408Ali HussainPas encore d'évaluation

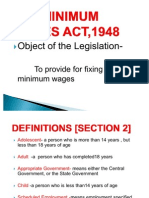

- Minimum Wages Act, 1948Document20 pagesMinimum Wages Act, 1948Manish KumarPas encore d'évaluation

- Ankit Sharma: Thanks For Choosing Swiggy, Ankit Sharma! Here Are Your Order Details: Delivery ToDocument2 pagesAnkit Sharma: Thanks For Choosing Swiggy, Ankit Sharma! Here Are Your Order Details: Delivery TobhetariaPas encore d'évaluation

- Antitrust Law ChecklistDocument4 pagesAntitrust Law ChecklistZhaojiang XuePas encore d'évaluation

- Jurnal 2, Celebrity Endorsement, Brand Credibility and Brand Equity PDFDocument36 pagesJurnal 2, Celebrity Endorsement, Brand Credibility and Brand Equity PDFSari LimPas encore d'évaluation

- Ch. 1 - GST (Goods and Services Tax)Document15 pagesCh. 1 - GST (Goods and Services Tax)Natasha SinghPas encore d'évaluation

- Technical SpecificationsDocument16 pagesTechnical Specificationsgg zoiPas encore d'évaluation

- Service Charges and Fees For Current Account Advantage Effective July 01 2022Document2 pagesService Charges and Fees For Current Account Advantage Effective July 01 2022rupak.album.03Pas encore d'évaluation

- Privacy Information Management Systems: Protect Comply ThriveDocument10 pagesPrivacy Information Management Systems: Protect Comply ThriveVincent John RigorPas encore d'évaluation

- Multiple Choice Questions For Non Executives To Executive Examination in CILDocument40 pagesMultiple Choice Questions For Non Executives To Executive Examination in CILsbaheti48100% (1)