Vous aimerez peut-être aussi

- Sample Trust DeedDocument11 pagesSample Trust DeedCA Mukesh Kumar Mishra100% (1)

- Toolkit On ESG For Fund ManagersDocument25 pagesToolkit On ESG For Fund ManagersMariah Sharp100% (1)

- The Road To WealthDocument275 pagesThe Road To Wealthgabbo24100% (1)

- Part 3 Case Digest Eladla de Lima vs. Laguna Tayabas CoDocument13 pagesPart 3 Case Digest Eladla de Lima vs. Laguna Tayabas CoJay-r Mercado ValenciaPas encore d'évaluation

- Elements of Accounting LectureDocument43 pagesElements of Accounting LectureRaissa Mae100% (1)

- Internship Report On Bank AlfalahDocument38 pagesInternship Report On Bank Alfalahaamir mumtazPas encore d'évaluation

- CT Energy Subscription Agreement 08142019Document9 pagesCT Energy Subscription Agreement 08142019Fred Lamert0% (1)

- Finance Ministry - Monthly Economic Report - August 2011Document11 pagesFinance Ministry - Monthly Economic Report - August 2011yasheshthakkarPas encore d'évaluation

- Inddec 10Document12 pagesInddec 10Surbhi SarnaPas encore d'évaluation

- Indian EconomyDocument13 pagesIndian Economygadekar1986Pas encore d'évaluation

- Press Note ON Estimates of Gross Domestic Product For The First QuarterDocument5 pagesPress Note ON Estimates of Gross Domestic Product For The First QuarterRajesh PatelPas encore d'évaluation

- Current State of Indian Economy August 2010 Current State of Indian EconomyDocument16 pagesCurrent State of Indian Economy August 2010 Current State of Indian EconomyNishant VyasPas encore d'évaluation

- Ministry of Finance Department of Economic Affairs Economic Division 4 (5) /ec. Dn. /2010Document13 pagesMinistry of Finance Department of Economic Affairs Economic Division 4 (5) /ec. Dn. /2010AshishPas encore d'évaluation

- Economic Survey of India 2012 Echap-09Document24 pagesEconomic Survey of India 2012 Echap-09sachi26Pas encore d'évaluation

- AnnualReport2010 11Document265 pagesAnnualReport2010 11Sriram CbPas encore d'évaluation

- Monthly Economic Report July 270812Document13 pagesMonthly Economic Report July 270812Chandrakant AgarwalPas encore d'évaluation

- Rav 3Q 2011Document44 pagesRav 3Q 2011Emerson RichardPas encore d'évaluation

- GDP GrowthDocument3 pagesGDP GrowthmoulshreesharmaPas encore d'évaluation

- Indian EconomyDocument15 pagesIndian EconomyleoboyrulesPas encore d'évaluation

- 01 Growth and InvestmentDocument31 pages01 Growth and Investmentmalikrahul_53Pas encore d'évaluation

- Current State of Indian Economy November 2010: Federation of Indian Chambers of Commerce and Industry New DelhiDocument16 pagesCurrent State of Indian Economy November 2010: Federation of Indian Chambers of Commerce and Industry New DelhiRohit KallaPas encore d'évaluation

- Annual Report 2011 - 12 PDFDocument108 pagesAnnual Report 2011 - 12 PDFHenizionPas encore d'évaluation

- Aug2010 IndiaecoDocument12 pagesAug2010 IndiaecovatsadbgPas encore d'évaluation

- 1pstate of EconomyDocument15 pages1pstate of EconomysuvradipPas encore d'évaluation

- IIP June2011 ICRA 120811Document8 pagesIIP June2011 ICRA 120811Krishna Chaitanya.APas encore d'évaluation

- The Real Economy: Economic GrowthDocument5 pagesThe Real Economy: Economic GrowthMamun KabirPas encore d'évaluation

- IIP NovDocument9 pagesIIP Novharen1234Pas encore d'évaluation

- India GDP Growth RateDocument2 pagesIndia GDP Growth RateBhanu MehraPas encore d'évaluation

- Current State of Indian Economy September 2010Document16 pagesCurrent State of Indian Economy September 2010mahajanrahulPas encore d'évaluation

- Per Capita GDP at Factor Cost (RS.) : QE: Quick Estimate RE: Revised EstimateDocument5 pagesPer Capita GDP at Factor Cost (RS.) : QE: Quick Estimate RE: Revised EstimateSankar NarayananPas encore d'évaluation

- Current State of Indian Economy July 2010 Current State of Indian EconomyDocument17 pagesCurrent State of Indian Economy July 2010 Current State of Indian EconomyPritamkshettyPas encore d'évaluation

- Vietnam - Economic Highlights - Stronger Economic Activities in May - 1/6/2010Document4 pagesVietnam - Economic Highlights - Stronger Economic Activities in May - 1/6/2010Rhb InvestPas encore d'évaluation

- E02dcindustry News Digest (Issue No. 4)Document63 pagesE02dcindustry News Digest (Issue No. 4)Prafulla TekriwalPas encore d'évaluation

- Year Book 10-11 EngDocument138 pagesYear Book 10-11 EngRajiv MahajanPas encore d'évaluation

- Economic Survey of India 2012 Echap-11Document26 pagesEconomic Survey of India 2012 Echap-11sachi26Pas encore d'évaluation

- 1st Quarterly Economic Performance Release 2011Document14 pages1st Quarterly Economic Performance Release 2011amektomPas encore d'évaluation

- Rbi 4Document7 pagesRbi 4Khizer Ahmed KhanPas encore d'évaluation

- Public Debt Management: Quarterly Report Apr-Jun 2010Document27 pagesPublic Debt Management: Quarterly Report Apr-Jun 2010rachitganatraPas encore d'évaluation

- National Quickstat: As of February 2012Document4 pagesNational Quickstat: As of February 2012Michael Ian TianoPas encore d'évaluation

- Indian EconomyDocument12 pagesIndian Economyprakash_adimulam9840Pas encore d'évaluation

- India Econimic Survey 2010-11Document296 pagesIndia Econimic Survey 2010-11vishwanathPas encore d'évaluation

- State of The Economy and Prospects: Website: Http://indiabudget - Nic.inDocument22 pagesState of The Economy and Prospects: Website: Http://indiabudget - Nic.inNDTVPas encore d'évaluation

- Gross Domestic Product For The First Quarter of 2011Document5 pagesGross Domestic Product For The First Quarter of 2011lineaextraPas encore d'évaluation

- 01 Growth and InvestmentDocument24 pages01 Growth and Investmentbugti1986Pas encore d'évaluation

- GDP Growth, Q1FY11: Pace of Growth Accelerates To 8.8%: ContactsDocument6 pagesGDP Growth, Q1FY11: Pace of Growth Accelerates To 8.8%: Contactssamm123456Pas encore d'évaluation

- Gurwinder 1Document20 pagesGurwinder 1shyamalmishra1988Pas encore d'évaluation

- Construction Spending December 2011Document1 pageConstruction Spending December 2011Jessica Kister-LombardoPas encore d'évaluation

- Highlight of Economy 2009-10-2Document18 pagesHighlight of Economy 2009-10-2Mateen SajidPas encore d'évaluation

- Current Macroeconomic Situation: Real SectorDocument14 pagesCurrent Macroeconomic Situation: Real SectorMonkey.D. LuffyPas encore d'évaluation

- Asia Construct: Indian Construction IndustryDocument52 pagesAsia Construct: Indian Construction IndustryAshish DesaiPas encore d'évaluation

- Apic Country Report India 2012Document103 pagesApic Country Report India 2012Amrendra KumarPas encore d'évaluation

- FICCI Eco Survey 2011 12Document9 pagesFICCI Eco Survey 2011 12Krunal KeniaPas encore d'évaluation

- Indonesias Economic Outlook 2011Document93 pagesIndonesias Economic Outlook 2011lutfhizPas encore d'évaluation

- Country Strategy 2011-2014 RussiaDocument18 pagesCountry Strategy 2011-2014 RussiaBeeHoofPas encore d'évaluation

- FRBM 1Document6 pagesFRBM 1girishyadav89Pas encore d'évaluation

- Economic Highlights - Economic Activities Improved in April - 30/04/2010Document4 pagesEconomic Highlights - Economic Activities Improved in April - 30/04/2010Rhb InvestPas encore d'évaluation

- Indian EconomyDocument17 pagesIndian EconomymanboombaamPas encore d'évaluation

- Docum 444Document84 pagesDocum 444Dheeman BaruaPas encore d'évaluation

- On The Development of The Russian Economy in 2011 and Forecast For 2012-2014Document31 pagesOn The Development of The Russian Economy in 2011 and Forecast For 2012-2014ftorbergPas encore d'évaluation

- National Quickstat: As of June 2011Document4 pagesNational Quickstat: As of June 2011Allan Roelen BacaronPas encore d'évaluation

- CPI, Dec 2011: MalaysiaDocument7 pagesCPI, Dec 2011: Malaysiamhaidar_6Pas encore d'évaluation

- National Quickstat: As of November 2011Document4 pagesNational Quickstat: As of November 2011Allan Roelen BacaronPas encore d'évaluation

- Economic Highlights - Industrial Production Slowed Down Markedly in July, Pointing To Further Deceleration in Economic Growth in The 3Q - 09/09/2010Document3 pagesEconomic Highlights - Industrial Production Slowed Down Markedly in July, Pointing To Further Deceleration in Economic Growth in The 3Q - 09/09/2010Rhb InvestPas encore d'évaluation

- Economic Highlights - Vietnam: Real GDP Grew at A Stronger Pace in The 1H-01/07/2010Document3 pagesEconomic Highlights - Vietnam: Real GDP Grew at A Stronger Pace in The 1H-01/07/2010Rhb InvestPas encore d'évaluation

- Property Boom and Banking Bust: The Role of Commercial Lending in the Bankruptcy of BanksD'EverandProperty Boom and Banking Bust: The Role of Commercial Lending in the Bankruptcy of BanksPas encore d'évaluation

- Unloved Bull Markets: Getting Rich the Easy Way by Riding Bull MarketsD'EverandUnloved Bull Markets: Getting Rich the Easy Way by Riding Bull MarketsPas encore d'évaluation

- 16 Role of SME in Indian Economoy - Ruchika - FINC004Document22 pages16 Role of SME in Indian Economoy - Ruchika - FINC004Ajeet SinghPas encore d'évaluation

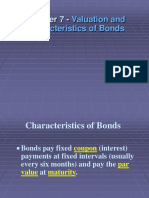

- Chapter 7 - : Valuation and Characteristics of BondsDocument54 pagesChapter 7 - : Valuation and Characteristics of BondsAndre SantosoPas encore d'évaluation

- Blue Star Corp. v. CKF Properties, CUMcv-07-448 (Cumberland Super. CT., 2008)Document26 pagesBlue Star Corp. v. CKF Properties, CUMcv-07-448 (Cumberland Super. CT., 2008)Chris BuckPas encore d'évaluation

- GrandFoundy 2011Document57 pagesGrandFoundy 2011eepPas encore d'évaluation

- DB Corp: Performance HighlightsDocument11 pagesDB Corp: Performance HighlightsAngel BrokingPas encore d'évaluation

- Edu-Care Professional Academy:, 243, Sundaram Coplex, Bhanwerkuan Main Road, IndoreDocument10 pagesEdu-Care Professional Academy:, 243, Sundaram Coplex, Bhanwerkuan Main Road, IndoreCA Gourav Jashnani100% (1)

- Keec 106Document17 pagesKeec 106KarthikPrakashPas encore d'évaluation

- Bicol University Legazpi City Consolidated Notes To Fy 2013 Financial StatementsDocument14 pagesBicol University Legazpi City Consolidated Notes To Fy 2013 Financial Statementsjaymark camachoPas encore d'évaluation

- 01 NIC Annual Report 64-65Document84 pages01 NIC Annual Report 64-65Ronit KcPas encore d'évaluation

- AT&T NegotiationDocument29 pagesAT&T NegotiationEbube Anizor100% (5)

- Credit Management Mid Term Assignment - Arafat Hussain - Id - 1303010034Document12 pagesCredit Management Mid Term Assignment - Arafat Hussain - Id - 1303010034ArafatAdilPas encore d'évaluation

- May Salary PayrollDocument610 pagesMay Salary PayrollSaurabh SinghPas encore d'évaluation

- Discretionary Financing Fees (DF Fees)Document1 pageDiscretionary Financing Fees (DF Fees)Daniel WigginsPas encore d'évaluation

- (LC) International TradeDocument17 pages(LC) International TradeSumayra RahmanPas encore d'évaluation

- Hospital ManagementDocument23 pagesHospital ManagementFahim AhmedPas encore d'évaluation

- HBA, MCA, Computer Advance Forms For Government EmployeesDocument7 pagesHBA, MCA, Computer Advance Forms For Government EmployeesprinceejPas encore d'évaluation

- Villaroel v. EstradaDocument1 pageVillaroel v. EstradaAudreySyUyanPas encore d'évaluation

- Annu Singh FinalDocument64 pagesAnnu Singh Finalsauravv7100% (1)

- Lifting The Corporate VeilDocument3 pagesLifting The Corporate VeilLennox Allen KipPas encore d'évaluation

- Essar OilDocument20 pagesEssar OilVinay PrabhakarPas encore d'évaluation

- Development Financial Institution of IndiaDocument11 pagesDevelopment Financial Institution of IndiaarunimaPas encore d'évaluation

- Care'S Default and Transition Study 2018Document10 pagesCare'S Default and Transition Study 2018praveenmohantyPas encore d'évaluation

- BMR Case StudyDocument92 pagesBMR Case StudychamatkaribabaPas encore d'évaluation