Vous aimerez peut-être aussi

- Mirion Level 10Document6 pagesMirion Level 10wicsPas encore d'évaluation

- 2012 NIDA - Part Time BrochureDocument6 pages2012 NIDA - Part Time BrochurewicsPas encore d'évaluation

- 2012 NIDA - Part Time BrochureDocument6 pages2012 NIDA - Part Time BrochurewicsPas encore d'évaluation

- Map - MPCC 2010Document1 pageMap - MPCC 2010wicsPas encore d'évaluation

- 9026 Sydnunsp Membership Brochure 2011Document2 pages9026 Sydnunsp Membership Brochure 2011wicsPas encore d'évaluation

- DCA 212 Chapter 6Document3 pagesDCA 212 Chapter 6wicsPas encore d'évaluation

- Dragon Magazine 382Document119 pagesDragon Magazine 382Arturo Partida100% (5)

- Sampling Guide - UK National Audit OfficeDocument20 pagesSampling Guide - UK National Audit OfficeChi Lam YeungPas encore d'évaluation

- Postprocessing in Machine Learning and Data Mining: Ivan Bruha A. (Fazel) FamiliDocument5 pagesPostprocessing in Machine Learning and Data Mining: Ivan Bruha A. (Fazel) FamiliwicsPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Costco Case StudyDocument3 pagesCostco Case StudyMaong LakiPas encore d'évaluation

- Fatwa Backbiting An Aalim Fatwa Razwiya PDFDocument3 pagesFatwa Backbiting An Aalim Fatwa Razwiya PDFzubairmbbsPas encore d'évaluation

- NDA Template Non Disclosure Non Circumvent No Company NameDocument9 pagesNDA Template Non Disclosure Non Circumvent No Company NamepvorsterPas encore d'évaluation

- Hac 1001 NotesDocument56 pagesHac 1001 NotesMarlin MerikanPas encore d'évaluation

- Rainin Catalog 2014 ENDocument92 pagesRainin Catalog 2014 ENliebersax8282Pas encore d'évaluation

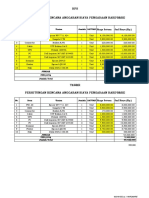

- HPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANDocument2 pagesHPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANYanto AstriPas encore d'évaluation

- Basic Principles of Social Stratification - Sociology 11 - A SY 2009-10Document9 pagesBasic Principles of Social Stratification - Sociology 11 - A SY 2009-10Ryan Shimojima67% (3)

- Week 1 ITM 410Document76 pagesWeek 1 ITM 410Awesom QuenzPas encore d'évaluation

- Scantype NNPC AdvertDocument3 pagesScantype NNPC AdvertAdeshola FunmilayoPas encore d'évaluation

- Research Course Outline For Resarch Methodology Fall 2011 (MBA)Document3 pagesResearch Course Outline For Resarch Methodology Fall 2011 (MBA)mudassarramzanPas encore d'évaluation

- Cinema Urn NBN Si Doc-Z01y9afrDocument24 pagesCinema Urn NBN Si Doc-Z01y9afrRyan BrandãoPas encore d'évaluation

- Hume's Standard TasteDocument15 pagesHume's Standard TasteAli Majid HameedPas encore d'évaluation

- Successfull Weight Loss: Beginner'S Guide ToDocument12 pagesSuccessfull Weight Loss: Beginner'S Guide ToDenise V. FongPas encore d'évaluation

- Writing Assessment and Evaluation Checklist - PeerDocument1 pageWriting Assessment and Evaluation Checklist - PeerMarlyn Joy YaconPas encore d'évaluation

- Saic P 3311Document7 pagesSaic P 3311Arshad ImamPas encore d'évaluation

- 3 QDocument2 pages3 QJerahmeel CuevasPas encore d'évaluation

- M8 UTS A. Sexual SelfDocument10 pagesM8 UTS A. Sexual SelfAnon UnoPas encore d'évaluation

- Rock Art and Metal TradeDocument22 pagesRock Art and Metal TradeKavu RI100% (1)

- Presidential Decree 1613 Amending The Law of ArsonDocument19 pagesPresidential Decree 1613 Amending The Law of ArsonBfp Atimonan QuezonPas encore d'évaluation

- Line GraphDocument13 pagesLine GraphMikelAgberoPas encore d'évaluation

- Effective Instruction OverviewDocument5 pagesEffective Instruction Overviewgene mapaPas encore d'évaluation

- BSD ReviewerDocument17 pagesBSD ReviewerMagelle AgbalogPas encore d'évaluation

- What Are Open-Ended Questions?Document3 pagesWhat Are Open-Ended Questions?Cheonsa CassiePas encore d'évaluation

- Asia Competitiveness ForumDocument2 pagesAsia Competitiveness ForumRahul MittalPas encore d'évaluation

- What is your greatest strengthDocument14 pagesWhat is your greatest strengthDolce NcubePas encore d'évaluation

- Lec 1 Modified 19 2 04102022 101842amDocument63 pagesLec 1 Modified 19 2 04102022 101842amnimra nazimPas encore d'évaluation

- Business Beyond Profit Motivation Role of Employees As Decision-Makers in The Business EnterpriseDocument6 pagesBusiness Beyond Profit Motivation Role of Employees As Decision-Makers in The Business EnterpriseCaladhiel100% (1)

- Food and ReligionDocument8 pagesFood and ReligionAniket ChatterjeePas encore d'évaluation

- Lab Report FormatDocument2 pagesLab Report Formatapi-276658659Pas encore d'évaluation

- Diagnosis of Dieback Disease of The Nutmeg Tree in Aceh Selatan, IndonesiaDocument10 pagesDiagnosis of Dieback Disease of The Nutmeg Tree in Aceh Selatan, IndonesiaciptaPas encore d'évaluation