Vous aimerez peut-être aussi

- FABM Accounting FundamentalsDocument17 pagesFABM Accounting FundamentalsKyle Kyle67% (3)

- Fabm1 Module 1Document2 pagesFabm1 Module 1Alyssa De Guzman75% (4)

- FABM 1 NotesDocument24 pagesFABM 1 Notessam100% (14)

- FABM-1 - Module 1 - Intro To AccountingDocument13 pagesFABM-1 - Module 1 - Intro To AccountingKJ Jones100% (26)

- Accounting Concepts and PrinciplesDocument4 pagesAccounting Concepts and PrinciplesNardsdel Rivera100% (12)

- FUNDAMENTALS OF ABM Reviewer 1st QDocument18 pagesFUNDAMENTALS OF ABM Reviewer 1st QJin's pink slippers100% (5)

- Branches of Accounting ExplainedDocument54 pagesBranches of Accounting ExplainedAbby Rosales - Perez100% (1)

- Learn the Accounting Equation and Rules of Debit and CreditDocument21 pagesLearn the Accounting Equation and Rules of Debit and CreditJesseca JosafatPas encore d'évaluation

- SRCBAI ABM1 Q3M10 Merchandising Concern Part1Document14 pagesSRCBAI ABM1 Q3M10 Merchandising Concern Part1Jaye RuantoPas encore d'évaluation

- Fundamentals of Accountancy, Business and Management 1Document25 pagesFundamentals of Accountancy, Business and Management 1Worship Songs / Choreo / LyricsPas encore d'évaluation

- Nature of AccountingDocument2 pagesNature of AccountingElla Simone100% (5)

- Nature of Accounting and Its Business EnvironmentDocument24 pagesNature of Accounting and Its Business EnvironmentApril Mae Villaceran100% (2)

- Accounting Reviewer Grade 11 ABMDocument1 pageAccounting Reviewer Grade 11 ABMHabibi Waishu77% (13)

- Far 1 - Activity 1 - Sept. 09, 2020 - Answer SheetDocument4 pagesFar 1 - Activity 1 - Sept. 09, 2020 - Answer SheetAnonn100% (1)

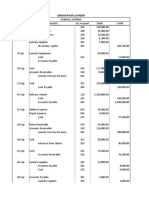

- Jordan River LaundryDocument4 pagesJordan River Laundryidk irdkPas encore d'évaluation

- FABM Dictionary 1Document32 pagesFABM Dictionary 1Candy TinapayPas encore d'évaluation

- History of AccountingDocument17 pagesHistory of AccountingJasmine Garcia57% (7)

- FABM 1 Lesson 8 Types of Major AccountsDocument7 pagesFABM 1 Lesson 8 Types of Major AccountsTiffany CenizaPas encore d'évaluation

- Summary FunaccDocument130 pagesSummary FunaccMicxz Sulit80% (5)

- Chapter 2Document24 pagesChapter 2Lleiram Bulotano Bolanio25% (4)

- Quiz For AccountingDocument1 pageQuiz For AccountingKelvin Jay Sebastian Sapla50% (2)

- Dr.-King AnswerDocument3 pagesDr.-King AnswerAdolph Christian Gonzales100% (1)

- Fabm NotesDocument8 pagesFabm NotesMark Jay Bongolan100% (1)

- Chapter 3 - Users of Accounting InformationDocument22 pagesChapter 3 - Users of Accounting InformationDM BonoanPas encore d'évaluation

- Department of Education: Learning Activity Sheet Third QuarterDocument18 pagesDepartment of Education: Learning Activity Sheet Third QuarterMark Joseph Bielza100% (1)

- WR SFP Using Report and Account FormDocument10 pagesWR SFP Using Report and Account FormJohn Fort Edwin AmoraPas encore d'évaluation

- A Brief History of AccountingDocument3 pagesA Brief History of AccountingRae Michael75% (4)

- Test Question For Exam Chapter 1 To 6Document4 pagesTest Question For Exam Chapter 1 To 6Cherryl ValmoresPas encore d'évaluation

- Lesson 9.4 Adjusting EntriesDocument36 pagesLesson 9.4 Adjusting EntriesDanica Medina50% (2)

- The Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingDocument12 pagesThe Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingKim Patrick Victoria100% (1)

- Fundamentals of ABM 1 Accounting CycleDocument47 pagesFundamentals of ABM 1 Accounting CycleHarrold HarryPas encore d'évaluation

- Fundamentals of ABM 1 & 2: Accounting ExercisesDocument22 pagesFundamentals of ABM 1 & 2: Accounting ExercisesRezel Funtilar100% (2)

- Drill ABMDocument1 pageDrill ABMGeorge Gonzales78% (23)

- Fabm 1 MidtermsDocument9 pagesFabm 1 MidtermsNicole Dantes100% (1)

- Branches of AccountingDocument14 pagesBranches of AccountingSharif ShaikPas encore d'évaluation

- Accounting Branches: Financial, Managerial, Cost, Auditing & MoreDocument2 pagesAccounting Branches: Financial, Managerial, Cost, Auditing & MoreMJ San PedroPas encore d'évaluation

- Users of Accounting InformationDocument17 pagesUsers of Accounting InformationZybel Rosales67% (3)

- History of AccountingDocument1 pageHistory of AccountingElvira Baliag0% (1)

- 7 Business FormsDocument14 pages7 Business FormsJc Coronacion100% (3)

- Delos Reyes Quiz 1Document2 pagesDelos Reyes Quiz 1zavriaPas encore d'évaluation

- Reviewer Fabm2Document7 pagesReviewer Fabm2Anne BustilloPas encore d'évaluation

- Fabm 1Document7 pagesFabm 1Phia Vhianna RamirezPas encore d'évaluation

- Chapter 2 and 3 Lopez BookDocument4 pagesChapter 2 and 3 Lopez BookSam CorsigaPas encore d'évaluation

- Chapter 1 Introduction To AccountingDocument51 pagesChapter 1 Introduction To AccountingHeisei De LunaPas encore d'évaluation

- Mr. Labandero Journalizing Posting and Unadjusted Trial Balance ASSIGNMENT KEYDocument8 pagesMr. Labandero Journalizing Posting and Unadjusted Trial Balance ASSIGNMENT KEYMiguel Nieves67% (6)

- FABM 1 Lesson 1-Introdcution To AccountingDocument7 pagesFABM 1 Lesson 1-Introdcution To AccountingJon Carlo Garcia MachetePas encore d'évaluation

- ABM 1 Module 4 Accounting Concepts and PrinciplesDocument9 pagesABM 1 Module 4 Accounting Concepts and PrinciplesJey Di100% (2)

- Review of FS Preparation, Analysis and InterpretationDocument50 pagesReview of FS Preparation, Analysis and InterpretationAries Gonzales Caragan0% (2)

- Fundamental of Accountancy, Business and Management ReviewerDocument5 pagesFundamental of Accountancy, Business and Management ReviewerMarkDeoAboboto100% (2)

- AccountingDocument88 pagesAccountingFranky100% (3)

- Fundamentals of Accountancy, Business and Management 1: Quarter 3 - Module 3: The Accounting EquationDocument22 pagesFundamentals of Accountancy, Business and Management 1: Quarter 3 - Module 3: The Accounting EquationMarissa Dulay - Sitanos92% (13)

- Actg1 - Chapter 3Document37 pagesActg1 - Chapter 3Reynaleen Agta100% (1)

- Lesson 5 Accounting Concepts and PrinciplesDocument26 pagesLesson 5 Accounting Concepts and PrinciplesTJ gatmaitan67% (9)

- Week 7-8Document8 pagesWeek 7-8Kim Albero Cubel0% (1)

- Notes For Class 11 AccountsDocument21 pagesNotes For Class 11 AccountsKhuanna KapoorPas encore d'évaluation

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"D'Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Pas encore d'évaluation

- Accounting System Short Notes Du Bcom Hons Chapter 1Document7 pagesAccounting System Short Notes Du Bcom Hons Chapter 1ishubhy111Pas encore d'évaluation

- Introduction To AccountingDocument40 pagesIntroduction To AccountingMuskan BohraPas encore d'évaluation

- Conceptual Framework of Financial Accounting and ReportingDocument9 pagesConceptual Framework of Financial Accounting and ReportingOyeleye TofunmiPas encore d'évaluation

- IndexDocument1 pageIndexRajs MalikPas encore d'évaluation

- KPDocument3 pagesKPRajs MalikPas encore d'évaluation

- MDU BEd 2014 InstituteDocument33 pagesMDU BEd 2014 InstituteRajs MalikPas encore d'évaluation

- District Wise List of Clerk: RohtakDocument4 pagesDistrict Wise List of Clerk: RohtakRajs MalikPas encore d'évaluation

- Haryana Public Service CommissionDocument5 pagesHaryana Public Service CommissionIndiaresultPas encore d'évaluation

- Norton Ghost 2003 Users GuideDocument221 pagesNorton Ghost 2003 Users GuideFredsr BoydPas encore d'évaluation

- Enlistment Criteria2010Document21 pagesEnlistment Criteria2010Rajs MalikPas encore d'évaluation

- List of RateDocument1 pageList of RateRavi JainPas encore d'évaluation

- Boiler PresentationDocument54 pagesBoiler PresentationRajs MalikPas encore d'évaluation

- COMPUTERDocument6 pagesCOMPUTERRajs MalikPas encore d'évaluation

- Disinvestment in Public SectorDocument7 pagesDisinvestment in Public SectorRajs MalikPas encore d'évaluation

- Bcom BMT 1st Business MathDocument231 pagesBcom BMT 1st Business MathRajs MalikPas encore d'évaluation

- Budgetary Control NumericalDocument8 pagesBudgetary Control NumericalPuja AgarwalPas encore d'évaluation

- Grade 4 Science Quiz Bee QuestionsDocument3 pagesGrade 4 Science Quiz Bee QuestionsCecille Guillermo78% (9)

- INDIA'S DEFENCE FORCESDocument3 pagesINDIA'S DEFENCE FORCESJanardhan ChakliPas encore d'évaluation

- Molly C. Dwyer Clerk of CourtDocument3 pagesMolly C. Dwyer Clerk of CourtL. A. PatersonPas encore d'évaluation

- Script For The FiestaDocument3 pagesScript For The FiestaPaul Romano Benavides Royo95% (21)

- Financial Management-Capital BudgetingDocument39 pagesFinancial Management-Capital BudgetingParamjit Sharma100% (53)

- Pharmacology of GingerDocument24 pagesPharmacology of GingerArkene LevyPas encore d'évaluation

- A Random-Walk-Down-Wall-Street-Malkiel-En-2834 PDFDocument5 pagesA Random-Walk-Down-Wall-Street-Malkiel-En-2834 PDFTim100% (1)

- Mini Lecture and Activity Sheets in English For Academic and Professional Purposes Quarter 4, Week 5Document11 pagesMini Lecture and Activity Sheets in English For Academic and Professional Purposes Quarter 4, Week 5EllaPas encore d'évaluation

- Assessment of Hygiene Status and Environmental Conditions Among Street Food Vendors in South-Delhi, IndiaDocument6 pagesAssessment of Hygiene Status and Environmental Conditions Among Street Food Vendors in South-Delhi, IndiaAdvanced Research Publications100% (1)

- IT WorkShop Lab ManualDocument74 pagesIT WorkShop Lab ManualcomputerstudentPas encore d'évaluation

- SuccessDocument146 pagesSuccessscribdPas encore d'évaluation

- How To Write A Cover Letter For A Training ProgramDocument4 pagesHow To Write A Cover Letter For A Training Programgyv0vipinem3100% (2)

- WritingSubmission OET20 SUMMARIZE SUBTEST WRITING ASSESSMENT 726787 40065 PDFDocument6 pagesWritingSubmission OET20 SUMMARIZE SUBTEST WRITING ASSESSMENT 726787 40065 PDFLeannaPas encore d'évaluation

- 1995 - Legacy SystemsDocument5 pages1995 - Legacy SystemsJosé MªPas encore d'évaluation

- 1 Minute Witness PDFDocument8 pages1 Minute Witness PDFMark Aldwin LopezPas encore d'évaluation

- Apple Mango Buche'es Business PlanDocument51 pagesApple Mango Buche'es Business PlanTyron MenesesPas encore d'évaluation

- KAMAGONGDocument2 pagesKAMAGONGjeric plumosPas encore d'évaluation

- VT JCXDocument35 pagesVT JCXAkshay WingriderPas encore d'évaluation

- Chapter 6 Sequence PakistanDocument16 pagesChapter 6 Sequence PakistanAsif Ullah0% (1)

- Postmodern Dystopian Fiction: An Analysis of Bradbury's Fahrenheit 451' Maria AnwarDocument4 pagesPostmodern Dystopian Fiction: An Analysis of Bradbury's Fahrenheit 451' Maria AnwarAbdennour MaafaPas encore d'évaluation

- TAFJ-H2 InstallDocument11 pagesTAFJ-H2 InstallMrCHANTHAPas encore d'évaluation

- Referensi Blok 15 16Document2 pagesReferensi Blok 15 16Dela PutriPas encore d'évaluation

- Foundations of Public Policy AnalysisDocument20 pagesFoundations of Public Policy AnalysisSimran100% (1)

- FIN 1050 - Final ExamDocument6 pagesFIN 1050 - Final ExamKathi100% (1)

- AIRs LM Business-Finance Q1 Module-5Document25 pagesAIRs LM Business-Finance Q1 Module-5Oliver N AnchetaPas encore d'évaluation

- Sarina Dimaggio Teaching Resume 5Document1 pageSarina Dimaggio Teaching Resume 5api-660205517Pas encore d'évaluation

- WSP - Aci 318-02 Shear Wall DesignDocument5 pagesWSP - Aci 318-02 Shear Wall DesignSalomi Ann GeorgePas encore d'évaluation

- Credit Suisse AI ResearchDocument38 pagesCredit Suisse AI ResearchGianca DevinaPas encore d'évaluation

- Mechanics of Solids Unit - I: Chadalawada Ramanamma Engineering CollegeDocument1 pageMechanics of Solids Unit - I: Chadalawada Ramanamma Engineering CollegeMITTA NARESH BABUPas encore d'évaluation