Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- DownloadDocument4 pagesDownloadJames CarterPas encore d'évaluation

- Final Banking Law OutlineDocument95 pagesFinal Banking Law OutlineQuinton JohnsonPas encore d'évaluation

- Acccob2 Quiz 2 1203 Acccob2 k44 Financial AccountingDocument18 pagesAcccob2 Quiz 2 1203 Acccob2 k44 Financial AccountingChelcy Mari GugolPas encore d'évaluation

- A. 1a Problem 4Document1 pageA. 1a Problem 4shuzoPas encore d'évaluation

- IS and LMDocument18 pagesIS and LMM Samee ArifPas encore d'évaluation

- The Buyback OptionDocument7 pagesThe Buyback OptionsabijagdishPas encore d'évaluation

- 2022 - 02 - 03 Revision in Rates of NSSDocument10 pages2022 - 02 - 03 Revision in Rates of NSSKhawaja Burhan0% (2)

- Chapter 1. Overview of International Settlement1.Document4 pagesChapter 1. Overview of International Settlement1.BipPas encore d'évaluation

- Credit Risk Management Practice in Private Banks Case Study Bank of AbyssiniaDocument85 pagesCredit Risk Management Practice in Private Banks Case Study Bank of AbyssiniaamognePas encore d'évaluation

- Chapter 11 Capital N SurplusDocument12 pagesChapter 11 Capital N SurplusCiciPas encore d'évaluation

- OpTransactionHistory19 11 2019Document14 pagesOpTransactionHistory19 11 2019maheshPas encore d'évaluation

- Multinational Corporations: Some of Characteristics of Mncs AreDocument7 pagesMultinational Corporations: Some of Characteristics of Mncs AreMuskan KaurPas encore d'évaluation

- Day of Turmoil As Negative Rates Strike Fear Into Global MarketsDocument24 pagesDay of Turmoil As Negative Rates Strike Fear Into Global MarketsstefanoPas encore d'évaluation

- Natural English Collocations PDFDocument97 pagesNatural English Collocations PDFOana Adriana Stroe0% (1)

- OutputDocument37 pagesOutputTrisha RafalloPas encore d'évaluation

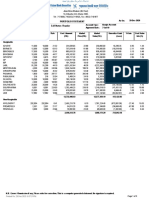

- Portfolio Statement Client Code: W0015 Name: Asish Dey Status: Active Call Status: RegularDocument3 pagesPortfolio Statement Client Code: W0015 Name: Asish Dey Status: Active Call Status: RegularSumitPas encore d'évaluation

- TVM Practice Questions Fall 2018Document4 pagesTVM Practice Questions Fall 2018ZarakKhanPas encore d'évaluation

- Acco 30103 Integrated Review in Afar 1st Evaluation Examination 2022Document42 pagesAcco 30103 Integrated Review in Afar 1st Evaluation Examination 2022Bunny SonyaPas encore d'évaluation

- The Negotiable Instruments Act, 1881Document55 pagesThe Negotiable Instruments Act, 1881meghna_mg8780% (5)

- Final Exam Engineering EconomyDocument2 pagesFinal Exam Engineering EconomyGelvie Lagos100% (2)

- Swift: Icbpo Irrevocable Conditional Bank Pay Order: TRANSACTION CODEDocument2 pagesSwift: Icbpo Irrevocable Conditional Bank Pay Order: TRANSACTION CODEdavid patrick100% (2)

- Hundaol ProposalDocument22 pagesHundaol ProposalletahundaolkasaPas encore d'évaluation

- Econ 304 HW 4Document14 pagesEcon 304 HW 4Tedjo Ardyandaru ImardjokoPas encore d'évaluation

- Types of Risk in MicrofinanceDocument9 pagesTypes of Risk in Microfinancevish100% (1)

- 02 PPT Statement of Financial Position PDFDocument61 pages02 PPT Statement of Financial Position PDFRaizah GaloPas encore d'évaluation

- Finance Quiz 6Document131 pagesFinance Quiz 6Peak ChindapolPas encore d'évaluation

- MODAUD1 UNIT 6 - Audit of InvestmentsDocument7 pagesMODAUD1 UNIT 6 - Audit of InvestmentsJake BundokPas encore d'évaluation

- The History of Paper Money in China (Pp. 136-142) John PickeringDocument8 pagesThe History of Paper Money in China (Pp. 136-142) John Pickeringzloty941Pas encore d'évaluation

- XXXXXXXXXX0009 20240128150640302188 UnlockedDocument6 pagesXXXXXXXXXX0009 20240128150640302188 Unlockedr6540073Pas encore d'évaluation

- Financial InclusionDocument57 pagesFinancial InclusionRaman Kumar100% (11)