Vous aimerez peut-être aussi

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)D'EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Évaluation : 5 sur 5 étoiles5/5 (1)

- Practice Multiple Choice Questions For First Test PDFDocument10 pagesPractice Multiple Choice Questions For First Test PDFBringinthehypePas encore d'évaluation

- Practice Multiple Choice Questions For First Test PDFDocument10 pagesPractice Multiple Choice Questions For First Test PDFBringinthehypePas encore d'évaluation

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsD'EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsPas encore d'évaluation

- Cfas ReviewerDocument10 pagesCfas ReviewershaylieeePas encore d'évaluation

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideD'EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuidePas encore d'évaluation

- Chapter 5 Test BankDocument12 pagesChapter 5 Test Bankmyngoc181233% (3)

- The Entrepreneur’S Dictionary of Business and Financial TermsD'EverandThe Entrepreneur’S Dictionary of Business and Financial TermsPas encore d'évaluation

- Activity 3 FinMaDocument6 pagesActivity 3 FinMaDiomela BionganPas encore d'évaluation

- Chapter 3. Mas-Ambray & BasulDocument7 pagesChapter 3. Mas-Ambray & BasulAmbray LynjoyPas encore d'évaluation

- Summary of Richard A. Lambert's Financial Literacy for ManagersD'EverandSummary of Richard A. Lambert's Financial Literacy for ManagersPas encore d'évaluation

- Answers Homework # 19 - Financial Reporting IDocument5 pagesAnswers Homework # 19 - Financial Reporting IRaman APas encore d'évaluation

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)D'EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (5)

- Principles of Financial Accounting PDFDocument5 pagesPrinciples of Financial Accounting PDFJia SPas encore d'évaluation

- Final PB ToaDocument6 pagesFinal PB ToaYaj CruzadaPas encore d'évaluation

- Applied Corporate Finance. What is a Company worth?D'EverandApplied Corporate Finance. What is a Company worth?Évaluation : 3 sur 5 étoiles3/5 (2)

- Financial AccountingDocument5 pagesFinancial Accountingimsana minatozakiPas encore d'évaluation

- Financial Accounting - Want to Become Financial Accountant in 30 Days?D'EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Évaluation : 5 sur 5 étoiles5/5 (1)

- Saint Vincent College of Cabuyao Financial Statement Analysis Quiz No. 1Document8 pagesSaint Vincent College of Cabuyao Financial Statement Analysis Quiz No. 1jovelyn labordoPas encore d'évaluation

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)D'EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Évaluation : 5 sur 5 étoiles5/5 (1)

- 6939 - Cash and Accruals BasisDocument5 pages6939 - Cash and Accruals BasisAljur SalamedaPas encore d'évaluation

- Acct 284 Clem Exam One - Doc Fall 2004Document3 pagesAcct 284 Clem Exam One - Doc Fall 2004noranycPas encore d'évaluation

- Act-6j03 Comp1 1stsem05-06Document14 pagesAct-6j03 Comp1 1stsem05-06RegenLudevesePas encore d'évaluation

- IA 3 ReviewerDocument23 pagesIA 3 ReviewerLarra NarcisoPas encore d'évaluation

- FAR Review Course Pre-Board - Answer KeyDocument17 pagesFAR Review Course Pre-Board - Answer KeyROMAR A. PIGAPas encore d'évaluation

- Pre Quali 2019Document9 pagesPre Quali 2019Haidie DiazPas encore d'évaluation

- ECO 444 Investments Test Bank-No AnswersDocument17 pagesECO 444 Investments Test Bank-No AnswersAllan Genesis Romblon100% (1)

- Finacc 3 Question Set BDocument9 pagesFinacc 3 Question Set BEza Joy ClaveriasPas encore d'évaluation

- Quiz 4Document7 pagesQuiz 4Vivienne Rozenn LaytoPas encore d'évaluation

- FAR Review Course Pre-Board - FinalDocument17 pagesFAR Review Course Pre-Board - FinalROMAR A. PIGA100% (1)

- English To Math and VocabDocument10 pagesEnglish To Math and VocabezaPas encore d'évaluation

- 01 (PRELIMS) FAR 2 (Intacc 1 - 2)Document19 pages01 (PRELIMS) FAR 2 (Intacc 1 - 2)Francis AsisPas encore d'évaluation

- College of Accountancy Final Examination Acctg.3A Instruction: Multiple ChoiceDocument7 pagesCollege of Accountancy Final Examination Acctg.3A Instruction: Multiple ChoiceDonalyn BannagaoPas encore d'évaluation

- OrcaDocument201 pagesOrcaFritzie Ann ZartigaPas encore d'évaluation

- P1 QuizzerDocument26 pagesP1 QuizzerLorena Joy AggabaoPas encore d'évaluation

- 5 13Document13 pages5 13rain06021992Pas encore d'évaluation

- Acctg 3b Midterm ExamDocument10 pagesAcctg 3b Midterm ExamDonalyn BannagaoPas encore d'évaluation

- Ias 7 Test Bank PDFDocument8 pagesIas 7 Test Bank PDFAB Cloyd100% (2)

- Midterm ExaminationDocument10 pagesMidterm ExaminationJo KePas encore d'évaluation

- Par Cor Accounting Cup - Average Round QuestionsDocument6 pagesPar Cor Accounting Cup - Average Round QuestionsShin YaePas encore d'évaluation

- Select The Best Answer From The Choices Given.: TheoryDocument14 pagesSelect The Best Answer From The Choices Given.: TheoryROMAR A. PIGAPas encore d'évaluation

- Far Theory Test BankDocument15 pagesFar Theory Test BankKimberly Etulle Celona100% (1)

- Adjusting ProcessDocument13 pagesAdjusting ProcessEly IseijinPas encore d'évaluation

- Corporate Finance Canadian 7th Edition Jaffe Test BankDocument27 pagesCorporate Finance Canadian 7th Edition Jaffe Test Bankdeborahmatayxojqtgzwr100% (13)

- FARAP 4702 ReceivablesDocument8 pagesFARAP 4702 Receivablesliberace cabreraPas encore d'évaluation

- ACYFAR1 CE On PAS1 (IAS1) Presentation of FSDocument4 pagesACYFAR1 CE On PAS1 (IAS1) Presentation of FSElle KongPas encore d'évaluation

- Theory of Accounts-SIR SALVADocument245 pagesTheory of Accounts-SIR SALVASofia SanchezPas encore d'évaluation

- Receivables QuizDocument3 pagesReceivables QuizGIRLPas encore d'évaluation

- Exercise 1Document3 pagesExercise 1CZARINA COMPLEPas encore d'évaluation

- Fundamentals of Accounting 1Document8 pagesFundamentals of Accounting 1julietpamintuanPas encore d'évaluation

- Examen Contabilidad IntermediaDocument8 pagesExamen Contabilidad IntermediaMariaPas encore d'évaluation

- Ia IDocument8 pagesIa IPamela BugarsoPas encore d'évaluation

- CASH FLOW STATEMENTS - Quiz 3Document2 pagesCASH FLOW STATEMENTS - Quiz 3JyPas encore d'évaluation

- Practical Accounting 1Document32 pagesPractical Accounting 1EdenA.Mata100% (9)

- Corporate Finance Canadian 7th Edition Ross Test BankDocument27 pagesCorporate Finance Canadian 7th Edition Ross Test BankChristinaCrawfordigdyp100% (16)

- Answers Homework # 20 - Financial Reporting IIDocument5 pagesAnswers Homework # 20 - Financial Reporting IIRaman APas encore d'évaluation

- Pamela Galang Bsa 2 IA3 Quiz - Cash Flows True or FalseDocument10 pagesPamela Galang Bsa 2 IA3 Quiz - Cash Flows True or FalseYukiPas encore d'évaluation

- Work Standards: 1) Five-Day Exception RuleDocument2 pagesWork Standards: 1) Five-Day Exception Rulemohit_namanPas encore d'évaluation

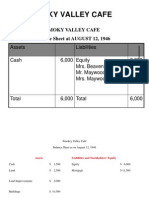

- Smoky Valley CafeDocument3 pagesSmoky Valley Cafemohit_namanPas encore d'évaluation

- Team NamesDocument14 pagesTeam Namesmohit_namanPas encore d'évaluation

- EstimationDocument6 pagesEstimationmohit_namanPas encore d'évaluation

- Proposal For: Co-Location FacilityDocument9 pagesProposal For: Co-Location Facilitymohit_namanPas encore d'évaluation

- 06 Feb 2024 - 451362AccStmtDownloadReport 1 4Document4 pages06 Feb 2024 - 451362AccStmtDownloadReport 1 4mohammedPas encore d'évaluation

- 5 Structured Products Forum 2007 Hong KongDocument11 pages5 Structured Products Forum 2007 Hong KongroversamPas encore d'évaluation

- 1 Cash and Cash EquivalentsDocument3 pages1 Cash and Cash EquivalentsSkie MaePas encore d'évaluation

- Bank Clerks' Exam: EnglishDocument8 pagesBank Clerks' Exam: Englishਰਾਹ ਗੀਰPas encore d'évaluation

- Principles of Macroeconomics 5E 5E Edition Ben Bernanke Et Al All ChapterDocument67 pagesPrinciples of Macroeconomics 5E 5E Edition Ben Bernanke Et Al All Chapterroscoe.carbonaro447100% (6)

- Contemporary Financial Management 13th Edition by Moyer McGuigan Rao ISBN Test BankDocument19 pagesContemporary Financial Management 13th Edition by Moyer McGuigan Rao ISBN Test Bankfrederick100% (25)

- Elements-Of Money FinancesDocument2 pagesElements-Of Money FinancesMayte DeliyorePas encore d'évaluation

- REPUBLIC ACT NO. 10883, July 17, 2016 An Act Providing For A New Anti-Carnapping Law of The PhilippinesDocument16 pagesREPUBLIC ACT NO. 10883, July 17, 2016 An Act Providing For A New Anti-Carnapping Law of The PhilippinesGabe BedanaPas encore d'évaluation

- What Is Spread Betting (Good) PDFDocument4 pagesWhat Is Spread Betting (Good) PDFMyriam GrissaPas encore d'évaluation

- Plagiarism Declaration Form (T-DF)Document8 pagesPlagiarism Declaration Form (T-DF)Nur HidayahPas encore d'évaluation

- Balance Statement ReportingDocument12 pagesBalance Statement ReportingahnaflionheartPas encore d'évaluation

- Accountancy em Iii RevisionDocument7 pagesAccountancy em Iii RevisionMalathi RajaPas encore d'évaluation

- DHFLDocument7 pagesDHFLSubhadip Sinha100% (1)

- CIR vs. Sekisui Jushi Philippines, IncDocument2 pagesCIR vs. Sekisui Jushi Philippines, IncCombat GunneyPas encore d'évaluation

- Fundamentals of Partnership: Dhiman ClaimsDocument7 pagesFundamentals of Partnership: Dhiman ClaimsAyareena GiriPas encore d'évaluation

- Boi and HDFCDocument24 pagesBoi and HDFCDharmikPas encore d'évaluation

- Shares Class PPT Sunil PandaDocument60 pagesShares Class PPT Sunil Pandadollpees01Pas encore d'évaluation

- SBR - Mock A - AnswersDocument14 pagesSBR - Mock A - AnswersDylan MutambanengwePas encore d'évaluation

- Receivables Management: "Any Fool Can Lend Money, But It TakesDocument37 pagesReceivables Management: "Any Fool Can Lend Money, But It Takesjai262418Pas encore d'évaluation

- Characteristics and Functions of MoneyDocument2 pagesCharacteristics and Functions of Moneyanastasiasteele_greyPas encore d'évaluation

- Modern Banking Services - A Key Tool For Banking Sector: Mobile No: 90038 12289Document6 pagesModern Banking Services - A Key Tool For Banking Sector: Mobile No: 90038 12289MD Hafizul Islam HafizPas encore d'évaluation

- Investments AssignmentDocument5 pagesInvestments Assignmentapi-276011592Pas encore d'évaluation

- Blueprint For Service Design of A Credit Card DivisionDocument3 pagesBlueprint For Service Design of A Credit Card Divisionanaghmahajan100% (1)

- Cakpo T. Paul Luc U: Who I'Am Personal InformationDocument4 pagesCakpo T. Paul Luc U: Who I'Am Personal Informationchancia angePas encore d'évaluation

- Dillon Read & The Aristocracy of Stock Profits - Catherine Austin FittsDocument231 pagesDillon Read & The Aristocracy of Stock Profits - Catherine Austin Fittsfourcade100% (2)

- Shriram Payslip MayDocument2 pagesShriram Payslip MayGanesh SahuPas encore d'évaluation

- Account Summary: Past Due Current Charges Total Amount DueDocument2 pagesAccount Summary: Past Due Current Charges Total Amount DueGuillermina HerreraPas encore d'évaluation

- Letter of Credit ProcedureDocument4 pagesLetter of Credit ProcedureKarthickDevanPas encore d'évaluation

- Final Accounts of CompaniesDocument30 pagesFinal Accounts of CompaniesAkanksha GanveerPas encore d'évaluation

- Chapter 15 HW SolutionDocument5 pagesChapter 15 HW SolutionZarifah FasihahPas encore d'évaluation

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)D'EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (15)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesD'EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesPas encore d'évaluation

- Getting to Yes: How to Negotiate Agreement Without Giving InD'EverandGetting to Yes: How to Negotiate Agreement Without Giving InÉvaluation : 4 sur 5 étoiles4/5 (652)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!D'EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Évaluation : 4.5 sur 5 étoiles4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindD'EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindÉvaluation : 5 sur 5 étoiles5/5 (231)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookD'EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookÉvaluation : 5 sur 5 étoiles5/5 (4)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeD'EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeÉvaluation : 4 sur 5 étoiles4/5 (21)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsD'EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsPas encore d'évaluation

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyD'EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyPas encore d'évaluation

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)D'EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Évaluation : 4 sur 5 étoiles4/5 (33)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineD'EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlinePas encore d'évaluation

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)D'EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Évaluation : 4.5 sur 5 étoiles4.5/5 (5)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessD'EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessÉvaluation : 4.5 sur 5 étoiles4.5/5 (28)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!D'EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Évaluation : 4.5 sur 5 étoiles4.5/5 (8)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetD'EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceD'EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceÉvaluation : 4 sur 5 étoiles4/5 (1)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCD'EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCÉvaluation : 5 sur 5 étoiles5/5 (1)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsD'EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingD'EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingÉvaluation : 4.5 sur 5 étoiles4.5/5 (760)

- Contract Negotiation Handbook: Getting the Most Out of Commercial DealsD'EverandContract Negotiation Handbook: Getting the Most Out of Commercial DealsÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookD'EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookPas encore d'évaluation

- Financial Accounting For Dummies: 2nd EditionD'EverandFinancial Accounting For Dummies: 2nd EditionÉvaluation : 5 sur 5 étoiles5/5 (10)

- Small Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessD'EverandSmall Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessPas encore d'évaluation