Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Value Chain Analysis of CokeDocument4 pagesValue Chain Analysis of CokeDeepak YadavPas encore d'évaluation

- Zeus Asset Management IncDocument7 pagesZeus Asset Management IncSmitha RajPas encore d'évaluation

- Chapter4 Feasibility of Idea ContinueDocument27 pagesChapter4 Feasibility of Idea ContinueCao ChanPas encore d'évaluation

- International StrategyDocument26 pagesInternational StrategyQuân Đoàn MinhPas encore d'évaluation

- Cost of Capital ExplainedDocument4 pagesCost of Capital ExplainedMaximusPas encore d'évaluation

- B2B Group 6 Section A PaytmDocument17 pagesB2B Group 6 Section A PaytmNeha RoyPas encore d'évaluation

- Mcs Imp QuestionsDocument4 pagesMcs Imp QuestionsNikhil KhobragadePas encore d'évaluation

- TBChap 008Document185 pagesTBChap 008JamiePas encore d'évaluation

- BASL Ratio Analysis Highlights Strong Financial PositionDocument18 pagesBASL Ratio Analysis Highlights Strong Financial PositionSreeram Anand IrugintiPas encore d'évaluation

- The Harvard and Chicago Schools and The Dominant FirmDocument28 pagesThe Harvard and Chicago Schools and The Dominant FirmGhada TariqPas encore d'évaluation

- Supply Chain Operations: Planning and SourcingDocument20 pagesSupply Chain Operations: Planning and Sourcingm. rubi setiawan100% (1)

- Porter's Five ForcesDocument3 pagesPorter's Five ForcesDEVINA GURRIAHPas encore d'évaluation

- SS Mid-Term Test Tax517 July 2022 Student VersionDocument6 pagesSS Mid-Term Test Tax517 July 2022 Student VersionFeahRafeah KikiPas encore d'évaluation

- COMP255 Question Bank Chapter 8Document8 pagesCOMP255 Question Bank Chapter 8Ferdous RahmanPas encore d'évaluation

- AttachmentDocument3 pagesAttachmentIkenna EdwinPas encore d'évaluation

- Determinants of Equity Share Prices in The Indian Corporate SectorDocument96 pagesDeterminants of Equity Share Prices in The Indian Corporate SectorRikesh Daliya100% (2)

- Advertising Management Unit-2Document85 pagesAdvertising Management Unit-2Anonymous RsBppDSPas encore d'évaluation

- Simplifyy - A Business Plan For A NewDocument41 pagesSimplifyy - A Business Plan For A NewSamyak Doshi100% (1)

- Idea To Launch (Stage Gate) Model: An Overview: by Scott J. EdgettDocument5 pagesIdea To Launch (Stage Gate) Model: An Overview: by Scott J. EdgettanassaleemPas encore d'évaluation

- Chapter 6-Media DecisionsDocument22 pagesChapter 6-Media DecisionsVarun VKPas encore d'évaluation

- Effect of Marketing Mix Strategies On Performance of Selected Dairy Co-Operative SocietiesDocument72 pagesEffect of Marketing Mix Strategies On Performance of Selected Dairy Co-Operative SocietiesAlexCorch75% (8)

- Reserve Management Parts I and II WBP Public 71907Document86 pagesReserve Management Parts I and II WBP Public 71907Primo KUSHFUTURES™ M©QUEENPas encore d'évaluation

- Ketan Parekh Scam MergedDocument48 pagesKetan Parekh Scam MergedKaushal RautPas encore d'évaluation

- Bisnis Internasional - Week 9 - The Global Capital MarketDocument21 pagesBisnis Internasional - Week 9 - The Global Capital MarketannabethPas encore d'évaluation

- TR 1Document45 pagesTR 1Nandini BhandariPas encore d'évaluation

- Tesco CRM ReportDocument2 pagesTesco CRM ReportSoham PradhanPas encore d'évaluation

- Export Selling vs. Export MarketingDocument22 pagesExport Selling vs. Export MarketingaudityaerosPas encore d'évaluation

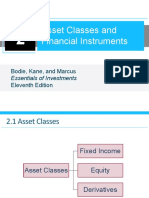

- Asset Classes and Financial Instruments: Bodie, Kane, and Marcus Eleventh EditionDocument48 pagesAsset Classes and Financial Instruments: Bodie, Kane, and Marcus Eleventh EditionFederico PortalePas encore d'évaluation

- The New Marketing Era ArticleDocument2 pagesThe New Marketing Era ArticleFerdows Abid ChowdhuryPas encore d'évaluation

- Final Report For Jeevan Dhaara - FinalDocument36 pagesFinal Report For Jeevan Dhaara - FinalAbhimanyu YadavPas encore d'évaluation