Vous aimerez peut-être aussi

- Mental HealthDocument18 pagesMental HealthNCGA Project User 1Pas encore d'évaluation

- MilitaryDocument10 pagesMilitaryNCGA Project User 1Pas encore d'évaluation

- Environment and Natural ResourcesDocument16 pagesEnvironment and Natural ResourcesNCGA Project User 1Pas encore d'évaluation

- Education: Governor-Elect Perdue Transition Advisory Group SessionsDocument14 pagesEducation: Governor-Elect Perdue Transition Advisory Group SessionsNCGA Project User 1100% (1)

- Crime Control and Juvenile JusticeDocument12 pagesCrime Control and Juvenile JusticeNCGA Project User 1Pas encore d'évaluation

- Health and Human ServicesDocument16 pagesHealth and Human ServicesNCGA Project User 1Pas encore d'évaluation

- EnergyDocument12 pagesEnergyNCGA Project User 1Pas encore d'évaluation

- AgingDocument12 pagesAgingNCGA Project User 1Pas encore d'évaluation

- Cultural ResourcesDocument10 pagesCultural ResourcesNCGA Project User 1Pas encore d'évaluation

- CorrectionsDocument10 pagesCorrectionsNCGA Project User 1Pas encore d'évaluation

- CommerceDocument12 pagesCommerceNCGA Project User 1Pas encore d'évaluation

- Administration: Governor-Elect Perdue Transition Advisory Group SessionsDocument8 pagesAdministration: Governor-Elect Perdue Transition Advisory Group SessionsNCGA Project User 1Pas encore d'évaluation

- TransportationDocument16 pagesTransportationNCGA Project User 1Pas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Federal Treasury Rules SummaryDocument21 pagesFederal Treasury Rules SummaryKhurram Sheraz50% (2)

- Soal Latihan Chapter 7 TM 1-2Document6 pagesSoal Latihan Chapter 7 TM 1-2Antonius Sugi Suhartono100% (1)

- 1568997886067Iq6YiG0o2YEDSfOe PDFDocument6 pages1568997886067Iq6YiG0o2YEDSfOe PDFalpoPas encore d'évaluation

- Hesco Online BillDocument2 pagesHesco Online BillYasir RazaPas encore d'évaluation

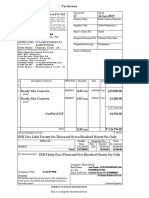

- Tax Invoice for Ready Mix ConcreteDocument1 pageTax Invoice for Ready Mix ConcreteFSPL HSEPas encore d'évaluation

- Price List OXYGEN PDFDocument2 pagesPrice List OXYGEN PDFParthPas encore d'évaluation

- Binder1 PDFDocument5 pagesBinder1 PDFSaad Raza KhanPas encore d'évaluation

- TCS India Process - Separation KitDocument25 pagesTCS India Process - Separation KitT HawkPas encore d'évaluation

- Demo Sheet VishwakarmaDocument15 pagesDemo Sheet Vishwakarmaasjkdaskj100% (1)

- Order to Cash Process in Oracle ERPDocument5 pagesOrder to Cash Process in Oracle ERPKishore KantamneniPas encore d'évaluation

- EBA Guidelines on Reporting Fraud Data Under PSD2Document33 pagesEBA Guidelines on Reporting Fraud Data Under PSD2ayalewtesfawPas encore d'évaluation

- School of Agriculture Fee Structure M. Sc. (Hons.) Horticulture (Vegetable Science) - M.SC Agriculture (Agronomy)Document1 pageSchool of Agriculture Fee Structure M. Sc. (Hons.) Horticulture (Vegetable Science) - M.SC Agriculture (Agronomy)Aarya ParasarPas encore d'évaluation

- Organic Shampoo Export Bill of Lading JamaicaDocument2 pagesOrganic Shampoo Export Bill of Lading JamaicaAavasqPas encore d'évaluation

- Salary Slip, Oct - 19 - EIPL - 109Document1 pageSalary Slip, Oct - 19 - EIPL - 109akhilesh singhPas encore d'évaluation

- Your Credit Card Statement: Miss Judith H Waters 30 Chantal Avenue Pen Y Fai Bridgend Mid Glamorgan CF31 4NNDocument4 pagesYour Credit Card Statement: Miss Judith H Waters 30 Chantal Avenue Pen Y Fai Bridgend Mid Glamorgan CF31 4NNhanhPas encore d'évaluation

- Werewolf Card SetDocument1 pageWerewolf Card SetKharPas encore d'évaluation

- Bernstein - India Financials Credit On UPI and The US$100 BN Consumer Transaction Credit Opportunity 2023-11-08Document18 pagesBernstein - India Financials Credit On UPI and The US$100 BN Consumer Transaction Credit Opportunity 2023-11-08narasimhaPas encore d'évaluation

- Customizing R/3 FI for VAT Processing in 3 StepsDocument8 pagesCustomizing R/3 FI for VAT Processing in 3 StepsJunling Xu100% (2)

- Exam SHODocument2 pagesExam SHOSakira ZakariaPas encore d'évaluation

- challanform9TH BIODocument1 pagechallanform9TH BIOferozabad schoolPas encore d'évaluation

- Manage tax regimes, jurisdictions, rates and formulasDocument2 301 pagesManage tax regimes, jurisdictions, rates and formulasrajaorugantiPas encore d'évaluation

- WalkingCyclingDesignGuideSG PDFDocument136 pagesWalkingCyclingDesignGuideSG PDFJoy Dawis-AsuncionPas encore d'évaluation

- Chapter 3 Employment Income A 202Document79 pagesChapter 3 Employment Income A 202ateen rizalmanPas encore d'évaluation

- Í ( 7/èteanco Hannaâloraineâ Mçâââ!), Fè1@Î: Plan SummaryDocument1 pageÍ ( 7/èteanco Hannaâloraineâ Mçâââ!), Fè1@Î: Plan SummaryHanna Mallorca TeancoPas encore d'évaluation

- Tourism Products and Services ExplainedDocument6 pagesTourism Products and Services ExplainedElyana100% (2)

- Chapter 6 Book-Keeping Balancing Off AccountsDocument12 pagesChapter 6 Book-Keeping Balancing Off AccountsfileacademyPas encore d'évaluation

- Oracle Cash ManagementDocument11 pagesOracle Cash ManagementSeenu DonPas encore d'évaluation

- How To Avoid Overdrafts and FeesDocument1 pageHow To Avoid Overdrafts and FeesPaul Tiberiu MandachePas encore d'évaluation

- Company ProfileDocument31 pagesCompany ProfileTimotius Aditya PrasetyaPas encore d'évaluation

- Muhammad Tahir S/O Muhammad Irshad Scheme No1 Abul Khair: Web Generated BillDocument1 pageMuhammad Tahir S/O Muhammad Irshad Scheme No1 Abul Khair: Web Generated BillUsama Elec15Pas encore d'évaluation