Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Overview of Spice IndustryDocument13 pagesOverview of Spice IndustryvaibhavPas encore d'évaluation

- Company CatagoryDocument8 pagesCompany CatagoryHotel EkasPas encore d'évaluation

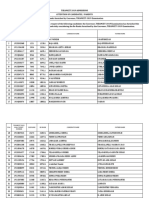

- NVS List ResultDocument131 pagesNVS List ResultShubham Kumar TiwariPas encore d'évaluation

- 644fdb116a586f00185b6b64 - ## - The First War of Independence 01: Summary Notes - (Victory 2024 - ICSE)Document37 pages644fdb116a586f00185b6b64 - ## - The First War of Independence 01: Summary Notes - (Victory 2024 - ICSE)Sushant KumarPas encore d'évaluation

- Datasets 100189 236788 AirQualityDocument57 pagesDatasets 100189 236788 AirQualityratnakarPas encore d'évaluation

- Official Invitation Letter To Law Schools For Participation - 6th PNBIMCCDocument3 pagesOfficial Invitation Letter To Law Schools For Participation - 6th PNBIMCCLive LawPas encore d'évaluation

- Landmark Judgements of Indian HistoryDocument25 pagesLandmark Judgements of Indian HistoryAmit SinghPas encore d'évaluation

- LPG drives globalization of Indian businessDocument5 pagesLPG drives globalization of Indian businessNikita Patwardhan100% (1)

- Evolution of India-Japan Ties: Prospects and Limitations: Manjeet S. PardesiDocument30 pagesEvolution of India-Japan Ties: Prospects and Limitations: Manjeet S. PardesiRupai SarkarPas encore d'évaluation

- Commercial History of DhakaDocument664 pagesCommercial History of DhakaNausheen Ahmed Noba100% (1)

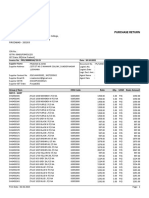

- Shivhare Garments purchase return detailsDocument34 pagesShivhare Garments purchase return detailsUjjwal GuptaPas encore d'évaluation

- Test - 5 - Indian Culture - Test-1Document16 pagesTest - 5 - Indian Culture - Test-1Srikanth Harinadh BPas encore d'évaluation

- UPSC Civil Services Examination: Revolt of 1857 - First War of Independence Against British Modern Indian History Notes for UPSCDocument4 pagesUPSC Civil Services Examination: Revolt of 1857 - First War of Independence Against British Modern Indian History Notes for UPSCSaurabh YadavPas encore d'évaluation

- KDocument7 pagesKMelissa JenkinsPas encore d'évaluation

- Tel-Directory - 2020-for-DMRC-WebsiteDocument11 pagesTel-Directory - 2020-for-DMRC-WebsitearadhanaPas encore d'évaluation

- Vdocuments - MX - I Have Dream by Rashmi BansalDocument14 pagesVdocuments - MX - I Have Dream by Rashmi BansalAshutosh JoshiPas encore d'évaluation

- Coal Vessel Updates As On 18 Mar 20Document15 pagesCoal Vessel Updates As On 18 Mar 20Frianata ZrPas encore d'évaluation

- 180 Days IAS Prelims Study Plan For 2017 PrelimsDocument9 pages180 Days IAS Prelims Study Plan For 2017 PrelimsmonumunduriPas encore d'évaluation

- Glossary: SPL Ch1: Understanding Diversity Notebook AssignmentDocument3 pagesGlossary: SPL Ch1: Understanding Diversity Notebook AssignmentsiddhantPas encore d'évaluation

- Africa in The Indian Imagination by Antoinette BurtonDocument43 pagesAfrica in The Indian Imagination by Antoinette BurtonDuke University PressPas encore d'évaluation

- Local Self GovernmentDocument10 pagesLocal Self GovernmentpriyaPas encore d'évaluation

- Tse Am Cet 2019 Admissions Re RanksDocument8 pagesTse Am Cet 2019 Admissions Re RanksBalamaniPas encore d'évaluation

- Tamil Calendar - WikipediaDocument14 pagesTamil Calendar - WikipediaVickyPas encore d'évaluation

- AP MBBS Final Merit List 2018Document248 pagesAP MBBS Final Merit List 2018నా పూకులో సనాతన ధర్మంPas encore d'évaluation

- Aurat Ki Masti Ka Raaz Urdu Sex Stories Desi Stories Urdu Sexy Kahani Desi Chudai Stories Hind PDFDocument3 pagesAurat Ki Masti Ka Raaz Urdu Sex Stories Desi Stories Urdu Sexy Kahani Desi Chudai Stories Hind PDFCara40% (5)

- Lovely MirajDocument3 pagesLovely MirajOnkar ChavanPas encore d'évaluation

- Kerala Districts, Taluks and Legislative Assembly ConstituenciesDocument3 pagesKerala Districts, Taluks and Legislative Assembly ConstituencieschintvanPas encore d'évaluation

- Bibliography of Ethnoarchaeological Studies Arunachal PradeshDocument22 pagesBibliography of Ethnoarchaeological Studies Arunachal PradeshJohn KAlespiPas encore d'évaluation

- Bank of Maharashtra PO Results 2016 Out!Document61 pagesBank of Maharashtra PO Results 2016 Out!nidhi tripathi100% (1)

- Aishe Table 2015-16Document428 pagesAishe Table 2015-16fpkhanzPas encore d'évaluation