Vous aimerez peut-être aussi

- CH2M EAC EstimateAtCompletionPolicyDocument5 pagesCH2M EAC EstimateAtCompletionPolicynparlance100% (1)

- IT Project ManagmentDocument9 pagesIT Project ManagmentNehal Gupta100% (1)

- Advance KC ScorecardDocument36 pagesAdvance KC ScorecardSteve VockrodtPas encore d'évaluation

- Budgetary Planning and Control: 7.1 Nature and Purposes of BudgetsDocument18 pagesBudgetary Planning and Control: 7.1 Nature and Purposes of Budgetsserge folegwePas encore d'évaluation

- Sound Transit - Resolution R2021-05 - Adopted August 5, 2021Document8 pagesSound Transit - Resolution R2021-05 - Adopted August 5, 2021The UrbanistPas encore d'évaluation

- Leantakt Template 1.5Document218 pagesLeantakt Template 1.5lexloxPas encore d'évaluation

- Assignment 3Document2 pagesAssignment 3MarryRose Dela Torre Ferranco100% (1)

- Investigating The Value of An MBA Education Using NPV Decision ModelDocument72 pagesInvestigating The Value of An MBA Education Using NPV Decision ModelnabilquadriPas encore d'évaluation

- Chapter 13 PDFDocument77 pagesChapter 13 PDFMaureen ToledoPas encore d'évaluation

- Quantitative Techniques WbaDocument6 pagesQuantitative Techniques WbaDavid Mboya100% (1)

- BUS353 Project ManagementDocument25 pagesBUS353 Project ManagementevolynnPas encore d'évaluation

- B07 UTP & WT Non Routine and Estimation ProcessDocument8 pagesB07 UTP & WT Non Routine and Estimation ProcessJamey SimpsonPas encore d'évaluation

- Ifrs CH 1-2Document3 pagesIfrs CH 1-2Khaled SherifPas encore d'évaluation

- Section 013300 Submit Tal ProceduresDocument5 pagesSection 013300 Submit Tal ProceduresAnonymous NUn6MESxPas encore d'évaluation

- Post Fixture ActivitiesDocument2 pagesPost Fixture Activitiessaikumar selaPas encore d'évaluation

- Gilgit Baltistan System of Financial Control 2009Document55 pagesGilgit Baltistan System of Financial Control 2009Muhammad ShakirPas encore d'évaluation

- Cwip Theory AccountingDocument33 pagesCwip Theory AccountingRebeccaNandaPas encore d'évaluation

- CWIP PolicyDocument6 pagesCWIP Policyeswaran69Pas encore d'évaluation

- North Fork Peachtree Creek Comprehensive Concept PlanDocument5 pagesNorth Fork Peachtree Creek Comprehensive Concept PlanZachary HansenPas encore d'évaluation

- BITS ZG628T Dissertation (For Students of M. Tech. Software Systems)Document21 pagesBITS ZG628T Dissertation (For Students of M. Tech. Software Systems)Shiva Beduduri100% (1)

- Individual Case Analysis mgmt-4710-m55Document37 pagesIndividual Case Analysis mgmt-4710-m55api-658585122Pas encore d'évaluation

- Budget AccountabilityDocument2 pagesBudget AccountabilityAi Ai Serna LawangonPas encore d'évaluation

- (Ebook - PDF) Itil Project Management MethodologyDocument5 pages(Ebook - PDF) Itil Project Management MethodologyLeonhard CamargoPas encore d'évaluation

- CCA Mid-Term DetailsDocument5 pagesCCA Mid-Term DetailsRyanCallejaPas encore d'évaluation

- Post Implementation Review GuideDocument15 pagesPost Implementation Review GuideFred OdiawoPas encore d'évaluation

- Hacc423 Question Bank 2021Document13 pagesHacc423 Question Bank 2021Tawanda Tatenda HerbertPas encore d'évaluation

- CS615 - Finalterm - by Dr. Tariq HanifDocument14 pagesCS615 - Finalterm - by Dr. Tariq HanifAbidPas encore d'évaluation

- Strengths of Primavera P6Document3 pagesStrengths of Primavera P6hashim malikPas encore d'évaluation

- CA Ipcc Fast Track Notes For Information Technology PDFDocument133 pagesCA Ipcc Fast Track Notes For Information Technology PDFhampaiah0% (1)

- Taxguru - In-Checklist For Statutory Audit of Bank Branch Audit An OverviewDocument8 pagesTaxguru - In-Checklist For Statutory Audit of Bank Branch Audit An OverviewBhavani GirineniPas encore d'évaluation

- 2020 Body Worn Camera Evaluation Report: ISC: Protected ADocument45 pages2020 Body Worn Camera Evaluation Report: ISC: Protected ACTV CalgaryPas encore d'évaluation

- 4 5868236919153887449-1Document49 pages4 5868236919153887449-1Fasiko Asmaro100% (1)

- Unit-3 Activity Planning and Risk Management The Objectives of Activity Planning Feasibility AssessmentDocument21 pagesUnit-3 Activity Planning and Risk Management The Objectives of Activity Planning Feasibility AssessmentzoePas encore d'évaluation

- Principles of Accounting Chapter 18Document36 pagesPrinciples of Accounting Chapter 18myrentistoodamnhighPas encore d'évaluation

- Accounting ReviewDocument24 pagesAccounting ReviewChris Tian FlorendoPas encore d'évaluation

- CA Ipcc Fast Track Notes For Imformation TechnologyDocument133 pagesCA Ipcc Fast Track Notes For Imformation TechnologySipoy Satish67% (3)

- Cen Hud PSC Agree MonitorDocument14 pagesCen Hud PSC Agree MonitorrkarlinPas encore d'évaluation

- BSBHR513 - FORMATIVE ASSESSMENT Activity 12 Q3 PDFDocument1 pageBSBHR513 - FORMATIVE ASSESSMENT Activity 12 Q3 PDFdgerke001Pas encore d'évaluation

- Mid Term Exam ITPM PMAS-AAUR BSIT 5 SolutionDocument7 pagesMid Term Exam ITPM PMAS-AAUR BSIT 5 SolutionUnknownPas encore d'évaluation

- CR Open Book Notes 2019Document61 pagesCR Open Book Notes 2019Wajih YunusPas encore d'évaluation

- ACCT504 Case Study 1 The Complete Accounting Cycle-13Document16 pagesACCT504 Case Study 1 The Complete Accounting Cycle-13chaitrasuhas0% (1)

- Framework - Post Implementation Review TemplateDocument11 pagesFramework - Post Implementation Review Templatemaisa207Pas encore d'évaluation

- Introduction To Logistics and Supply ChainDocument25 pagesIntroduction To Logistics and Supply ChainAmanda CheongPas encore d'évaluation

- IENG300 - Fall 2012 MidtermDocument11 pagesIENG300 - Fall 2012 MidtermAhmad Yassen GhayadPas encore d'évaluation

- Chapter 5 - Solution CasesDocument85 pagesChapter 5 - Solution CasesAgus Triana PutraPas encore d'évaluation

- Chapter 3Document2 pagesChapter 3Zvioule Ma Fuentes0% (1)

- MGMT 3000 Assignment 2017 v7 (Final) 2017Document14 pagesMGMT 3000 Assignment 2017 v7 (Final) 2017SahanPas encore d'évaluation

- Introduction To MAC OSDocument109 pagesIntroduction To MAC OSariess22009Pas encore d'évaluation

- FIN 201 Chapter 11 Homework QuestionsDocument4 pagesFIN 201 Chapter 11 Homework QuestionsKyzer GardiolaPas encore d'évaluation

- Chapter - 5Document11 pagesChapter - 5dejen mengstiePas encore d'évaluation

- Project Delivery and Control: SynopsisDocument22 pagesProject Delivery and Control: SynopsisChaitanya ShaligramPas encore d'évaluation

- The S Curves Made Easy With Oracle Primavera P6Document7 pagesThe S Curves Made Easy With Oracle Primavera P6sadiqaftab786Pas encore d'évaluation

- ICDV Evaluation Final ReportDocument17 pagesICDV Evaluation Final ReportCTV CalgaryPas encore d'évaluation

- Reproduced Below From Farthington Supply S Accounting Records Is The AccountsDocument1 pageReproduced Below From Farthington Supply S Accounting Records Is The AccountsLet's Talk With HassanPas encore d'évaluation

- Hong Kong University of Science and Technology FINA2303 Financial Management Final Mock Examination Spring 2015Document17 pagesHong Kong University of Science and Technology FINA2303 Financial Management Final Mock Examination Spring 2015Sin TungPas encore d'évaluation

- 1y0 403Document65 pages1y0 403velianlamaPas encore d'évaluation

- Accounting Exam GuideDocument3 pagesAccounting Exam GuideJUNE CARLO CATULONGPas encore d'évaluation

- LSCM - NotesDocument20 pagesLSCM - NotesJoju JohnyPas encore d'évaluation

- Project Management NotesDocument4 pagesProject Management NotesPovenesan KrishnanPas encore d'évaluation

- BSBPMG514 - Assessment Task 2: Task 1: Determine Project CostsDocument8 pagesBSBPMG514 - Assessment Task 2: Task 1: Determine Project CostsShaista MalikPas encore d'évaluation

- Borromeo v. DescallarDocument2 pagesBorromeo v. Descallarbenjo2001Pas encore d'évaluation

- GM 4Q W4Document24 pagesGM 4Q W4Charmaine GatchalianPas encore d'évaluation

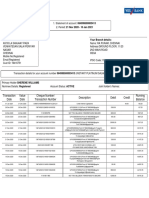

- Transaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running BalanceDocument2 pagesTransaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running Balancesylvereye07Pas encore d'évaluation

- Memo Re Intensification of Anti-Kidnapping Stratergy and Effort Against Motorcycle Riding Suspects (MRS)Document2 pagesMemo Re Intensification of Anti-Kidnapping Stratergy and Effort Against Motorcycle Riding Suspects (MRS)Wilben DanezPas encore d'évaluation

- PFRS 3 Business CombinationDocument3 pagesPFRS 3 Business CombinationRay Allen UyPas encore d'évaluation

- The Analysis of Foreign PolicyDocument24 pagesThe Analysis of Foreign PolicyMikael Dominik AbadPas encore d'évaluation

- Irish Independent Rate CardDocument2 pagesIrish Independent Rate CardPB VeroPas encore d'évaluation

- Pedani Maria PiaDocument17 pagesPedani Maria PiaZafer AksoyPas encore d'évaluation

- Candidate Profile - Apprenticeship Training PortalDocument3 pagesCandidate Profile - Apprenticeship Training PortalTasmay EnterprisesPas encore d'évaluation

- Indian Council Act, 1892Document18 pagesIndian Council Act, 1892Khan PurPas encore d'évaluation

- Hydrolics-Ch 4Document21 pagesHydrolics-Ch 4solxPas encore d'évaluation

- Consti - People Vs de LarDocument1 pageConsti - People Vs de LarLu CasPas encore d'évaluation

- Call CenterDocument25 pagesCall Centerbonika08Pas encore d'évaluation

- About HDFC Bank: ProfileDocument8 pagesAbout HDFC Bank: ProfileGoyalRichuPas encore d'évaluation

- Module 4 Criminal Law 1Document7 pagesModule 4 Criminal Law 1Frans Raff LopezPas encore d'évaluation

- Motion For Bill of ParticularsDocument3 pagesMotion For Bill of ParticularsPaulo Villarin67% (3)

- Full Download Technical Communication 12th Edition Markel Test BankDocument35 pagesFull Download Technical Communication 12th Edition Markel Test Bankchac49cjones100% (22)

- CHAP - 02 - Financial Statements of BankDocument72 pagesCHAP - 02 - Financial Statements of BankTran Thanh NganPas encore d'évaluation

- Poe-Llamanzares v. COMELECDocument1 pagePoe-Llamanzares v. COMELECRammel SantosPas encore d'évaluation

- False Imprisonment and IIED Ch. 1Document2 pagesFalse Imprisonment and IIED Ch. 1Litvin EstheticsPas encore d'évaluation

- SSGC Bill JunDocument1 pageSSGC Bill Junshahzaib azamPas encore d'évaluation

- 14 Vapour Absorption Refrigeration SystemsDocument20 pages14 Vapour Absorption Refrigeration SystemsPRASAD326100% (8)

- Memorandum Shall Be A Ground For Dismissal of The AppealDocument4 pagesMemorandum Shall Be A Ground For Dismissal of The AppealLitto B. BacasPas encore d'évaluation

- Presenters GuidelinesDocument9 pagesPresenters GuidelinesAl Dustur JurnalPas encore d'évaluation

- IA I Financial Accounting 3B MemoDocument5 pagesIA I Financial Accounting 3B MemoM CPas encore d'évaluation

- Cooperative BankDocument70 pagesCooperative BankMonil MittalPas encore d'évaluation

- LetterDocument2 pagesLetterAppleJoyAbao-PeleñoPas encore d'évaluation

- Reodica Vs Court of AppealsDocument2 pagesReodica Vs Court of AppealsChaoSisonPas encore d'évaluation

- Certificate of Conformity: No. CLSAN 080567 0058 Rev. 00Document2 pagesCertificate of Conformity: No. CLSAN 080567 0058 Rev. 00annamalaiPas encore d'évaluation

- Fund Flow StatementDocument21 pagesFund Flow StatementSarvagya GuptaPas encore d'évaluation