Vous aimerez peut-être aussi

- The Art of Maximizing Debt Collections: Digitization, Analytics, AI, Machine Learning and Performance ManagementD'EverandThe Art of Maximizing Debt Collections: Digitization, Analytics, AI, Machine Learning and Performance ManagementPas encore d'évaluation

- Chapter 2Document14 pagesChapter 2maryumarshad2Pas encore d'évaluation

- Ch. 1 RittenbergDocument32 pagesCh. 1 RittenbergAira CruzPas encore d'évaluation

- Chapter FourDocument24 pagesChapter FourMelat TPas encore d'évaluation

- Lecture 0224Document27 pagesLecture 0224jasonnumahnalkelPas encore d'évaluation

- ACC718 Topic 1Document22 pagesACC718 Topic 1Fujiyama IputuPas encore d'évaluation

- ACC718 Topic 3Document26 pagesACC718 Topic 3Fujiyama IputuPas encore d'évaluation

- Fundamentals of Auditing and Assurance ServicesDocument5 pagesFundamentals of Auditing and Assurance Servicesschooldocs itemsPas encore d'évaluation

- AA CH 2Document40 pagesAA CH 2mirogPas encore d'évaluation

- Ethical Behaviour and Implications For AccountantsDocument24 pagesEthical Behaviour and Implications For AccountantsKeoikantsePas encore d'évaluation

- Technical Update Refresher For Academics Presentation SlidesDocument58 pagesTechnical Update Refresher For Academics Presentation SlidesabushohagPas encore d'évaluation

- 2.0 Ethical Concerns For Accountants Mike MbayaDocument38 pages2.0 Ethical Concerns For Accountants Mike MbayaREJAY89Pas encore d'évaluation

- Department of Accounting Acc 316: Principles & Practice of AuditingDocument7 pagesDepartment of Accounting Acc 316: Principles & Practice of AuditingFreeman AbuPas encore d'évaluation

- Summary Last SessionDocument81 pagesSummary Last SessionmuhajedaPas encore d'évaluation

- Lecture 1 (I) - IntroductionDocument30 pagesLecture 1 (I) - IntroductionkhooPas encore d'évaluation

- Review Engagements:: Key DefinitionsDocument9 pagesReview Engagements:: Key DefinitionsQais Qazi ZadaPas encore d'évaluation

- Auditing, Assurance, Internal ControlDocument68 pagesAuditing, Assurance, Internal ControlDarji PareshPas encore d'évaluation

- IFA Chapter 1Document12 pagesIFA Chapter 1Suleyman TesfayePas encore d'évaluation

- New 27456Document60 pagesNew 27456Lovely Jane Raut CabiltoPas encore d'évaluation

- S02 EthicsDocument29 pagesS02 EthicsHashPas encore d'évaluation

- Consideration Before Commencing An AuditDocument13 pagesConsideration Before Commencing An AuditTushar GaurPas encore d'évaluation

- Solved Past Paper AuditingDocument7 pagesSolved Past Paper AuditingDaim AslamPas encore d'évaluation

- A 01 SOX ComplianceDocument34 pagesA 01 SOX ComplianceDevika TibrewalPas encore d'évaluation

- Week 3 PlanningDocument38 pagesWeek 3 Planningptnyagortey91Pas encore d'évaluation

- D11 Principles of AuditingDocument373 pagesD11 Principles of AuditingDixie Cheelo100% (1)

- Chapter 4 Ethics and AcceptanceDocument10 pagesChapter 4 Ethics and Acceptancerishi kareliaPas encore d'évaluation

- Ethical Issues in AccountingDocument16 pagesEthical Issues in AccountingsimplyhemsPas encore d'évaluation

- Auditor Independence, Ethics and Liability: Relates To Chapter 4 of TextDocument19 pagesAuditor Independence, Ethics and Liability: Relates To Chapter 4 of TextSteve SmithPas encore d'évaluation

- Chapter 13 Codes of Professional EthicsDocument26 pagesChapter 13 Codes of Professional EthicslnghiilwamoPas encore d'évaluation

- 2) Chapter 1 Assurance EngagementsDocument27 pages2) Chapter 1 Assurance Engagementsazone accounts & audit firmPas encore d'évaluation

- Old Engagement and New EngagementDocument3 pagesOld Engagement and New EngagementMohammad MonirujjamanPas encore d'évaluation

- In The Name of God, The Most Beneficent, The Eternally MercifulDocument22 pagesIn The Name of God, The Most Beneficent, The Eternally MercifulJhon AntoniPas encore d'évaluation

- Chapter 6 PlanningDocument19 pagesChapter 6 PlanningAbdulahi farah AbdiPas encore d'évaluation

- Chapter 1 Assurance EngagementsDocument31 pagesChapter 1 Assurance EngagementsOmer UddinPas encore d'évaluation

- Governance and Responsibility - Lecture 1Document16 pagesGovernance and Responsibility - Lecture 1Anep ZainuldinPas encore d'évaluation

- Group 4 The Audit ProcessDocument31 pagesGroup 4 The Audit ProcessYonica Salonga De BelenPas encore d'évaluation

- 01 Rittenberg PPT Ch1Document48 pages01 Rittenberg PPT Ch1Isabel HigginsPas encore d'évaluation

- Chapter ThreeDocument36 pagesChapter ThreeVida SalehiPas encore d'évaluation

- Chapter 4 - AuditDocument59 pagesChapter 4 - AuditMisshtaCPas encore d'évaluation

- Ethics: Understanding and Meeting Ethical ExpectationsDocument30 pagesEthics: Understanding and Meeting Ethical ExpectationsbaburamPas encore d'évaluation

- General Principles of A Financial Statement AuditDocument14 pagesGeneral Principles of A Financial Statement AuditMary Grace P CastroPas encore d'évaluation

- Code of Ethics: FOR Professional AccountantsDocument42 pagesCode of Ethics: FOR Professional AccountantsTracy Marsh RapanutPas encore d'évaluation

- Financial Statement AuditDocument43 pagesFinancial Statement AuditMahmudul HasanPas encore d'évaluation

- Audit Planning Lecture 6 NewDocument24 pagesAudit Planning Lecture 6 Newpadjetey00Pas encore d'évaluation

- Audit 1Document26 pagesAudit 1ngothimyduyen27042003Pas encore d'évaluation

- Sarbanes Oxley Audit Committee RequirementsDocument32 pagesSarbanes Oxley Audit Committee RequirementsMarian's PrelovePas encore d'évaluation

- 03.2 Handbook of The International Code of Ethics For Professional AccountantsDocument92 pages03.2 Handbook of The International Code of Ethics For Professional AccountantsnuggsPas encore d'évaluation

- Expanded Services of Accountants-FABM Chapter 2Document8 pagesExpanded Services of Accountants-FABM Chapter 2Jeannie Lyn Dela CruzPas encore d'évaluation

- Cycle 6 TM Session 3Document77 pagesCycle 6 TM Session 3abdulkadir mohamedPas encore d'évaluation

- ACCA Paper F8 - : Audit and Assurance (INT)Document232 pagesACCA Paper F8 - : Audit and Assurance (INT)sohail merchantPas encore d'évaluation

- F8 PresentationDocument232 pagesF8 PresentationDorian CaruanaPas encore d'évaluation

- Ethics in Accounting and Finance: Presented byDocument13 pagesEthics in Accounting and Finance: Presented byNikita WalterPas encore d'évaluation

- Performing Preliminary Engagement Activities: 1. Engagement Acceptance Procedures 2. Basis of EngagementDocument14 pagesPerforming Preliminary Engagement Activities: 1. Engagement Acceptance Procedures 2. Basis of EngagementCarlo manejaPas encore d'évaluation

- Grace Gural-Balaguer: Acctg 22 InstructorDocument59 pagesGrace Gural-Balaguer: Acctg 22 InstructorMary CuisonPas encore d'évaluation

- Federal Incentives That Can Show You The Money & Increase Cash FlowDocument23 pagesFederal Incentives That Can Show You The Money & Increase Cash FlowCBIZ Inc.Pas encore d'évaluation

- Lecture 5-Professional Ethics and Code of ConductDocument29 pagesLecture 5-Professional Ethics and Code of ConductNatalia NaveedPas encore d'évaluation

- Activity 1: Yellow Paper 1/4Document21 pagesActivity 1: Yellow Paper 1/4saralimanuyag8_25539Pas encore d'évaluation

- Advanced Auditing Chapter ThreeDocument49 pagesAdvanced Auditing Chapter ThreemirogPas encore d'évaluation

- Auditing Information Systems and Controls: The Only Thing Worse Than No Control Is the Illusion of ControlD'EverandAuditing Information Systems and Controls: The Only Thing Worse Than No Control Is the Illusion of ControlPas encore d'évaluation

- Accounting Policies and Procedures For Savings & Credit CoopDocument1 pageAccounting Policies and Procedures For Savings & Credit CoopJing SagittariusPas encore d'évaluation

- Joint Rules Implementing R.A. 9520 or The Cooperative Code of The PhilippinesDocument14 pagesJoint Rules Implementing R.A. 9520 or The Cooperative Code of The PhilippinesEdd N Ros AdlawanPas encore d'évaluation

- With Both Members and Non-MembersDocument2 pagesWith Both Members and Non-MembersJing SagittariusPas encore d'évaluation

- With Both Members and Non-MembersDocument2 pagesWith Both Members and Non-MembersJing SagittariusPas encore d'évaluation

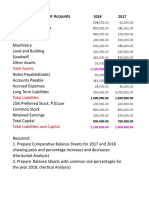

- Balance Sheet Accounts: Total AssetsDocument4 pagesBalance Sheet Accounts: Total AssetsJing SagittariusPas encore d'évaluation

- R.A 7160 Local Government CodeDocument1 pageR.A 7160 Local Government CodeJing SagittariusPas encore d'évaluation

- Finman Session 4 ForecastingDocument3 pagesFinman Session 4 ForecastingJing SagittariusPas encore d'évaluation

- Philippine Financial Reporting FrameworkDocument18 pagesPhilippine Financial Reporting FrameworkJing SagittariusPas encore d'évaluation

- 2 Risk and Credit Management - Hermes VergaraDocument119 pages2 Risk and Credit Management - Hermes VergaraJing SagittariusPas encore d'évaluation

- Standard Charts of Account For CooperativesDocument54 pagesStandard Charts of Account For CooperativesJing SagittariusPas encore d'évaluation

- Coop Pesos PaperDocument46 pagesCoop Pesos Paperkhasper_d100% (5)

- Cda Memorandum Circular 2015-09Document32 pagesCda Memorandum Circular 2015-09Jing Sagittarius100% (2)

- Coop Pesos FormulaDocument60 pagesCoop Pesos FormulaJing Sagittarius80% (5)

- VILLANUEVA-CASTRO COMMERCIAL LAW - New PDFDocument40 pagesVILLANUEVA-CASTRO COMMERCIAL LAW - New PDFJing Sagittarius100% (4)

- UP Civil Law Quizzer PDFDocument116 pagesUP Civil Law Quizzer PDFJing SagittariusPas encore d'évaluation

- Org BehaviorDocument29 pagesOrg BehaviorJing SagittariusPas encore d'évaluation

- Civ Pro (Riano) PDFDocument110 pagesCiv Pro (Riano) PDFJude-lo Aranaydo100% (3)

- Introduction To Statistical Thinking For Decision MakingDocument13 pagesIntroduction To Statistical Thinking For Decision MakingJing Sagittarius100% (1)

- SERVA 4-Axle Coiled Tubing Unit - Electric Over HydraulicDocument25 pagesSERVA 4-Axle Coiled Tubing Unit - Electric Over HydraulicWilliamPas encore d'évaluation

- Application For Type Aircraft Training: Farsco Training Center IR.147.12Document1 pageApplication For Type Aircraft Training: Farsco Training Center IR.147.12benyamin karimiPas encore d'évaluation

- AIDTauditDocument74 pagesAIDTauditCaleb TaylorPas encore d'évaluation

- 3-Module 3-23-Feb-2021Material I 23-Feb-2021 Error Detection and CorrectionDocument39 pages3-Module 3-23-Feb-2021Material I 23-Feb-2021 Error Detection and CorrectionPIYUSH RAJ GUPTA 19BCE2087Pas encore d'évaluation

- OOAD Documentation (Superstore)Document15 pagesOOAD Documentation (Superstore)Umâir KhanPas encore d'évaluation

- BUSINESS PROPOSAL-dönüştürüldü-2Document15 pagesBUSINESS PROPOSAL-dönüştürüldü-2Fatah Imdul UmasugiPas encore d'évaluation

- Law EssayDocument7 pagesLaw EssayNahula AliPas encore d'évaluation

- International Journal On Cryptography and Information Security (IJCIS)Document2 pagesInternational Journal On Cryptography and Information Security (IJCIS)ijcisjournalPas encore d'évaluation

- ACI 533.5R-20 Guide For Precast Concrete Tunnel SegmentsDocument84 pagesACI 533.5R-20 Guide For Precast Concrete Tunnel SegmentsJULIE100% (3)

- C10G - Hardware Installation GD - 3 - 12 - 2014Document126 pagesC10G - Hardware Installation GD - 3 - 12 - 2014Htt Ếch CốmPas encore d'évaluation

- 02 IG4K TechnologiesDocument47 pages02 IG4K TechnologiesM Tanvir AnwarPas encore d'évaluation

- Bugreport Fog - in SKQ1.211103.001 2023 04 10 19 23 21 Dumpstate - Log 9097Document32 pagesBugreport Fog - in SKQ1.211103.001 2023 04 10 19 23 21 Dumpstate - Log 9097chandrakanth reddyPas encore d'évaluation

- QuickTransit SSLI Release Notes 1.1Document12 pagesQuickTransit SSLI Release Notes 1.1subhrajitm47Pas encore d'évaluation

- SAM3-P256 Development Board Users Manual: This Datasheet Has Been Downloaded From at ThisDocument21 pagesSAM3-P256 Development Board Users Manual: This Datasheet Has Been Downloaded From at ThissunnguyenPas encore d'évaluation

- 010 Informed Search 2 - A StarDocument20 pages010 Informed Search 2 - A StarRashdeep SinghPas encore d'évaluation

- Final - Far Capital - Infopack Diana V3 PDFDocument79 pagesFinal - Far Capital - Infopack Diana V3 PDFjoekaledaPas encore d'évaluation

- Debt RestructuringDocument4 pagesDebt Restructuringjano_art21Pas encore d'évaluation

- A218437 HUET PDFDocument271 pagesA218437 HUET PDFKayser_MPas encore d'évaluation

- Bearing SettlementDocument4 pagesBearing SettlementBahaismail100% (1)

- LC1D40008B7: Product Data SheetDocument4 pagesLC1D40008B7: Product Data SheetLê Duy MinhPas encore d'évaluation

- MSW - 1 - 2016 Munisicpal Solid Waste Rules-2016 - Vol IDocument96 pagesMSW - 1 - 2016 Munisicpal Solid Waste Rules-2016 - Vol Inimm1962Pas encore d'évaluation

- Islm ModelDocument7 pagesIslm ModelPrastuti SachanPas encore d'évaluation

- Performance Online - Classic Car Parts CatalogDocument168 pagesPerformance Online - Classic Car Parts CatalogPerformance OnlinePas encore d'évaluation

- Gas Turbine Performance CalculationDocument7 pagesGas Turbine Performance CalculationAtiqur RahmanPas encore d'évaluation

- Lab Manual: Department of Computer EngineeringDocument65 pagesLab Manual: Department of Computer EngineeringRohitPas encore d'évaluation

- Qualifications and Disqualifications of CandidatesDocument3 pagesQualifications and Disqualifications of CandidatesCARLO JOSE BACTOLPas encore d'évaluation

- Introduction To Risk Management and Insurance 10th Edition Dorfman Test BankDocument26 pagesIntroduction To Risk Management and Insurance 10th Edition Dorfman Test BankMichelleBellsgkb100% (50)

- Sample Resume FinalDocument2 pagesSample Resume FinalSyed Asad HussainPas encore d'évaluation

- Testing Template - Plan and Cases CombinedDocument3 pagesTesting Template - Plan and Cases Combinedapi-19980631Pas encore d'évaluation

- Google Translate - Google SearchDocument1 pageGoogle Translate - Google SearchNicole Alex Bustamante CamposPas encore d'évaluation