Vous aimerez peut-être aussi

- The Impending Monetary Revolution, the Dollar and GoldD'EverandThe Impending Monetary Revolution, the Dollar and GoldPas encore d'évaluation

- The Eurozone in Crisis:: Professor Assaf RazinDocument59 pagesThe Eurozone in Crisis:: Professor Assaf RazinUmesh YadavPas encore d'évaluation

- Contagious Effects of Greece Crisis On Euro-Zone StatesDocument10 pagesContagious Effects of Greece Crisis On Euro-Zone StatesSidra MukhtarPas encore d'évaluation

- Eurozone Crisis ThesisDocument8 pagesEurozone Crisis Thesisfjf8xxz4100% (2)

- Guide To The Eurozone CrisisDocument9 pagesGuide To The Eurozone CrisisLakshmikanth RaoPas encore d'évaluation

- 1 DissertationsDocument11 pages1 DissertationsKumar DeepanshuPas encore d'évaluation

- Sovereign Debt: A Modern Greek Tragedy Greek Tragedy: Dr. Christopher WallerDocument44 pagesSovereign Debt: A Modern Greek Tragedy Greek Tragedy: Dr. Christopher WallerJay H. ManiPas encore d'évaluation

- What Is The European DebtDocument32 pagesWhat Is The European DebtVaibhav JainPas encore d'évaluation

- John Mauldin Weekly 10 SeptemberDocument11 pagesJohn Mauldin Weekly 10 Septemberrichardck61Pas encore d'évaluation

- Greece's 'Odious' Debt: The Looting of the Hellenic Republic by the Euro, the Political Elite and the Investment CommunityD'EverandGreece's 'Odious' Debt: The Looting of the Hellenic Republic by the Euro, the Political Elite and the Investment CommunityÉvaluation : 4 sur 5 étoiles4/5 (4)

- The Incomplete Currency: The Future of the Euro and Solutions for the EurozoneD'EverandThe Incomplete Currency: The Future of the Euro and Solutions for the EurozonePas encore d'évaluation

- Greece Crisis 2010Document26 pagesGreece Crisis 2010Kamalpreet KaurPas encore d'évaluation

- Euro Debt Crises: Written by Shoaib YaqoobDocument4 pagesEuro Debt Crises: Written by Shoaib Yaqoobhamid2k30Pas encore d'évaluation

- Vinod Gupta School of Management, IIT KHARAGPUR: About Fin-o-MenalDocument4 pagesVinod Gupta School of Management, IIT KHARAGPUR: About Fin-o-MenalFinterestPas encore d'évaluation

- Euro Debt-1Document7 pagesEuro Debt-1DHAVAL PATELPas encore d'évaluation

- W. Bello: Turning Villains Into Victims Finance Capital and GreeceDocument35 pagesW. Bello: Turning Villains Into Victims Finance Capital and GreeceGeorge PaynePas encore d'évaluation

- Compare and Contrast The Eurozone Debt Crisis of The 2000 and The LDC Crisis of 1980s. What Lessons Can Be Learnt From Both CrisisDocument12 pagesCompare and Contrast The Eurozone Debt Crisis of The 2000 and The LDC Crisis of 1980s. What Lessons Can Be Learnt From Both CrisisphlupoPas encore d'évaluation

- European UpdateDocument5 pagesEuropean UpdatebienvillecapPas encore d'évaluation

- Fixed Income Securities: Essay AssignmentDocument3 pagesFixed Income Securities: Essay AssignmentSheeraz AhmedPas encore d'évaluation

- Eurozone Crisis: Impacts: Prepared ForDocument24 pagesEurozone Crisis: Impacts: Prepared ForAkif AhmedPas encore d'évaluation

- The Reform of Europe: A Political Guide to the FutureD'EverandThe Reform of Europe: A Political Guide to the FutureÉvaluation : 2 sur 5 étoiles2/5 (1)

- The European Debt Crisis: HistoryDocument7 pagesThe European Debt Crisis: Historyaquash16scribdPas encore d'évaluation

- Eurozone Debt ProblemsDocument3 pagesEurozone Debt Problemsdt7inPas encore d'évaluation

- Bob Chapman The Euro Zone and The Crisis of Sovereign Debt 4 2 2012Document4 pagesBob Chapman The Euro Zone and The Crisis of Sovereign Debt 4 2 2012sankaratPas encore d'évaluation

- The Europea Debt: Why We Should Care?Document4 pagesThe Europea Debt: Why We Should Care?Qraen UchenPas encore d'évaluation

- Global Ebrief Subject: What The Past Could Mean For Greece, JapanDocument5 pagesGlobal Ebrief Subject: What The Past Could Mean For Greece, Japandwrich27Pas encore d'évaluation

- European Meltdown: Still Ahead or Better Outcome PossibleDocument18 pagesEuropean Meltdown: Still Ahead or Better Outcome PossiblepriyakshreyaPas encore d'évaluation

- Debt CrisisDocument8 pagesDebt CrisisUshma PandeyPas encore d'évaluation

- 09-06-11 - EOTM - European Mini Figure UnionDocument5 pages09-06-11 - EOTM - European Mini Figure Unionjake9781Pas encore d'évaluation

- Eurozone 8 11 11 PDFDocument8 pagesEurozone 8 11 11 PDFAbhishek AgrawalPas encore d'évaluation

- European Debt Crisis EssayDocument5 pagesEuropean Debt Crisis EssayJTMSPas encore d'évaluation

- The European Debt Crisis - A Beginner's GuideDocument10 pagesThe European Debt Crisis - A Beginner's GuideAbhishek SharmaPas encore d'évaluation

- Hayman Capital Management Letter To Investors (Nov 2011)Document12 pagesHayman Capital Management Letter To Investors (Nov 2011)Absolute Return100% (1)

- European Debt Crisis 2009 - 2011: The PIIGS and The Rest From Maastricht To PapandreouDocument39 pagesEuropean Debt Crisis 2009 - 2011: The PIIGS and The Rest From Maastricht To PapandreouAnuj KantPas encore d'évaluation

- Barcap Global BanksDocument10 pagesBarcap Global BanksNicholas AngPas encore d'évaluation

- Eurozone CrisisDocument22 pagesEurozone CrisisSazal MahnaPas encore d'évaluation

- Global Economy N.130: Agreement On Rescuing The Euro Zone Risks of Financial Contagion Briefs DecipheringDocument5 pagesGlobal Economy N.130: Agreement On Rescuing The Euro Zone Risks of Financial Contagion Briefs Decipheringapi-116406422Pas encore d'évaluation

- Summary and Analysis of The Euro: How a Common Currency Threatens the Future of Europe: Based on the Book by Joseph E. StiglitzD'EverandSummary and Analysis of The Euro: How a Common Currency Threatens the Future of Europe: Based on the Book by Joseph E. StiglitzÉvaluation : 5 sur 5 étoiles5/5 (3)

- Financial Crisis: Bank Run. Since Banks Lend Out Most of The Cash They Receive in Deposits (See FractionalDocument8 pagesFinancial Crisis: Bank Run. Since Banks Lend Out Most of The Cash They Receive in Deposits (See FractionalRabia MalikPas encore d'évaluation

- Lessons From The Global Financial Crisis: What Has Happened?Document11 pagesLessons From The Global Financial Crisis: What Has Happened?palashndcPas encore d'évaluation

- Euro Crisis ThesisDocument5 pagesEuro Crisis Thesisangeljordancincinnati100% (2)

- European Debt Crisis Research PaperDocument5 pagesEuropean Debt Crisis Research Paperafmcbmoag100% (1)

- Greek CrisisDocument10 pagesGreek Crisisvigneshkarthik2333% (3)

- Global Meltdown: A Warning Sign ?Document4 pagesGlobal Meltdown: A Warning Sign ?Alvin GeorgePas encore d'évaluation

- Will The Euro Survive 2012 ZDDocument3 pagesWill The Euro Survive 2012 ZDBruegelPas encore d'évaluation

- The Eurozone Debt CrisisDocument4 pagesThe Eurozone Debt CrisisIbrahim KakarPas encore d'évaluation

- Eurozone Crisis Research PaperDocument10 pagesEurozone Crisis Research Papergpwrbbbkf100% (1)

- George Soros On Soverign CrisesDocument8 pagesGeorge Soros On Soverign Crisesdoshi.dhruvalPas encore d'évaluation

- European Sovereign Debt Crisis - Wikipedia, The Free EncyclopediaDocument38 pagesEuropean Sovereign Debt Crisis - Wikipedia, The Free EncyclopediatsnikhilPas encore d'évaluation

- IMF Debt Markets - December 2013Document63 pagesIMF Debt Markets - December 2013Gold Silver WorldsPas encore d'évaluation

- Greece Crisis ExplainedDocument14 pagesGreece Crisis ExplainedAshish DuttPas encore d'évaluation

- Eurozone CrisisDocument33 pagesEurozone CrisisNgọc Lê Nguyễn BảoPas encore d'évaluation

- The Corona Crash: How the Pandemic Will Change CapitalismD'EverandThe Corona Crash: How the Pandemic Will Change CapitalismPas encore d'évaluation

- Q&A: Greek Debt Crisis: What Went Wrong in Greece?Document7 pagesQ&A: Greek Debt Crisis: What Went Wrong in Greece?starperformerPas encore d'évaluation

- Thesis On Eurozone CrisisDocument9 pagesThesis On Eurozone Crisisgbx272pg100% (2)

- The Greek - Sovereign Debt CrisisDocument13 pagesThe Greek - Sovereign Debt Crisischakri5555Pas encore d'évaluation

- Let's Talk About Our Future. Now!Document28 pagesLet's Talk About Our Future. Now!saitamPas encore d'évaluation

- European World CrisisDocument25 pagesEuropean World CrisisNaqi ShaukatPas encore d'évaluation

- Yahoo Compliance Guide For Law Enforcement 2008Document17 pagesYahoo Compliance Guide For Law Enforcement 2008Media ElitesPas encore d'évaluation

- An Industrial-Strength Audio Search AlgorithmDocument7 pagesAn Industrial-Strength Audio Search AlgorithmfermintvPas encore d'évaluation

- Talking With Alfred: Steven ShapinDocument9 pagesTalking With Alfred: Steven ShapinMrJohnGalt09Pas encore d'évaluation

- Obtaining Records From Social Networking WebsitesDocument5 pagesObtaining Records From Social Networking WebsitesMrJohnGalt09Pas encore d'évaluation

- HID iCLASS SecurityDocument13 pagesHID iCLASS SecurityMrJohnGalt09Pas encore d'évaluation

- GarysGuide SXSW 2012Document15 pagesGarysGuide SXSW 2012MrJohnGalt09Pas encore d'évaluation

- 60424Document4 pages60424MrJohnGalt09Pas encore d'évaluation

- Notes On PledgeDocument4 pagesNotes On Pledgefe rose sindinganPas encore d'évaluation

- Sbi Fast: Cash Management Product - State Bank of IndiaDocument6 pagesSbi Fast: Cash Management Product - State Bank of IndiaNisha MonishaPas encore d'évaluation

- Forwarded To Bank: Applicant Status ViewDocument4 pagesForwarded To Bank: Applicant Status ViewNANDANI kumariPas encore d'évaluation

- Accounting Cycle - Transactions: Fundamentals of Accountancy Business and Management 1 11 3 QuarterDocument4 pagesAccounting Cycle - Transactions: Fundamentals of Accountancy Business and Management 1 11 3 QuarterPaulo Amposta CarpioPas encore d'évaluation

- Romance of Rothschild PDFDocument312 pagesRomance of Rothschild PDFfatihaeePas encore d'évaluation

- A Project Report On "A Study of Internet Banking of State Bank of India''Document73 pagesA Project Report On "A Study of Internet Banking of State Bank of India''Aarti MalikPas encore d'évaluation

- Confidence CementDocument17 pagesConfidence Cementnahidul202Pas encore d'évaluation

- Warring Ton Apartments MIPv1Document7 pagesWarring Ton Apartments MIPv1Mark I'AnsonPas encore d'évaluation

- SRReport 1500301211137 PDFDocument2 pagesSRReport 1500301211137 PDFShahid Ali LodhiPas encore d'évaluation

- Agency and Credit and TransactionsDocument8 pagesAgency and Credit and TransactionsLUISA MARIE DELA CRUZPas encore d'évaluation

- The Capital Market Consolidation Act and The Korean Financial MarketDocument9 pagesThe Capital Market Consolidation Act and The Korean Financial MarketKorea Economic Institute of America (KEI)Pas encore d'évaluation

- Economic SlowdownDocument10 pagesEconomic SlowdownPrapti JainPas encore d'évaluation

- Introduction of Kotak Mahindra GroupDocument10 pagesIntroduction of Kotak Mahindra GroupAbhi JainPas encore d'évaluation

- Land Reforms in IndiaDocument19 pagesLand Reforms in IndiaMahesh Vanam100% (1)

- Disbursement Voucher CacadiranDocument8 pagesDisbursement Voucher CacadiranApril Joy Sumagit Hidalgo100% (1)

- Payment ReminderDocument1 pagePayment ReminderInassani AlifiaPas encore d'évaluation

- Credtrans MidtermsDocument4 pagesCredtrans MidtermsMariePas encore d'évaluation

- Project Proposal-West Timawa PO With Complete AnnexesDocument29 pagesProject Proposal-West Timawa PO With Complete AnnexesStewart Paul TorrePas encore d'évaluation

- EasyMail Services Ltd. Company ProfileDocument12 pagesEasyMail Services Ltd. Company ProfileMd Armanul Haque100% (1)

- Correlog For Pci DssDocument5 pagesCorrelog For Pci DssSaul MancillaPas encore d'évaluation

- PDFDocument7 pagesPDFClaytonPas encore d'évaluation

- Contoh Percakapan Handling Check in and ReservationDocument2 pagesContoh Percakapan Handling Check in and ReservationDede SuryansahPas encore d'évaluation

- GA Tax GuideDocument46 pagesGA Tax Guidedamilano1Pas encore d'évaluation

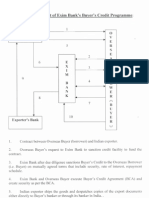

- Procedural Flow Chart of Exim BankDocument3 pagesProcedural Flow Chart of Exim BankMilan DasPas encore d'évaluation

- 10 Best Digital, Mobile, and Online Banking Services in The Philippines - Grit PHDocument45 pages10 Best Digital, Mobile, and Online Banking Services in The Philippines - Grit PHAriely0% (1)

- The MRTP ActDocument12 pagesThe MRTP ActGurpreet SinghPas encore d'évaluation

- Bank Practice and Procedures (Acfn2113) : Prepared By: Tewodros EDocument37 pagesBank Practice and Procedures (Acfn2113) : Prepared By: Tewodros Eመስቀል ኃይላችን ነውPas encore d'évaluation

- Capitec Bank StatementDocument1 pageCapitec Bank Statementbc180204979 ALI FAROOQ100% (3)

- Velarde v. Court of AppealsDocument6 pagesVelarde v. Court of Appealscmv mendozaPas encore d'évaluation

- Bill 00000000000000000000826433Document2 pagesBill 00000000000000000000826433Mohammad WaseemPas encore d'évaluation