Vous aimerez peut-être aussi

- Investment FundamentalsDocument16 pagesInvestment FundamentalsJay-Jay N. ImperialPas encore d'évaluation

- Corporate Accounting MCQDocument11 pagesCorporate Accounting MCQsharrine60% (5)

- McPhee Distillers Statements v03 CPDocument13 pagesMcPhee Distillers Statements v03 CPcmag10Pas encore d'évaluation

- Evaluacion Salud FinancieraDocument17 pagesEvaluacion Salud FinancieraWilliam VicuñaPas encore d'évaluation

- Material Complementario - Cafes Monte BiancoDocument20 pagesMaterial Complementario - Cafes Monte BiancoGlenda ChiquilloPas encore d'évaluation

- Chapter 1 and 2 MC and TFDocument17 pagesChapter 1 and 2 MC and TFAngela de MesaPas encore d'évaluation

- t10 2010 Jun QDocument10 pagest10 2010 Jun QAjay TakiarPas encore d'évaluation

- Feasibility Report For Making A School HRM ProjectDocument19 pagesFeasibility Report For Making A School HRM ProjectSherdil MahmoodPas encore d'évaluation

- Feasibility Report For Making A School HRM ProjectDocument19 pagesFeasibility Report For Making A School HRM ProjectSherdil MahmoodPas encore d'évaluation

- A1.2 Roic TreeDocument9 pagesA1.2 Roic TreemonemPas encore d'évaluation

- Boston Chicken CaseDocument7 pagesBoston Chicken CaseDji YangPas encore d'évaluation

- Msdi Alcala de Henares, SpainDocument24 pagesMsdi Alcala de Henares, SpainVineet NairPas encore d'évaluation

- FM09-CH 24Document16 pagesFM09-CH 24namitabijwePas encore d'évaluation

- Test 01 21 - Tri3 - FINA309Document9 pagesTest 01 21 - Tri3 - FINA309Kateryna Ternova100% (1)

- FA GP5 Assignment 1Document4 pagesFA GP5 Assignment 1saurabhPas encore d'évaluation

- Financial Ratios Analysis Project at Nestle and Engro Foods: Executive SummaryDocument9 pagesFinancial Ratios Analysis Project at Nestle and Engro Foods: Executive SummaryMuhammad Muzamil HussainPas encore d'évaluation

- Butler CaseDocument12 pagesButler CaseJosh BenjaminPas encore d'évaluation

- O.M. Scott - Sons CompanyDocument31 pagesO.M. Scott - Sons Companysultan altamashPas encore d'évaluation

- AACT 2173 FM Lesson 4 Tutorial (Additional)Document11 pagesAACT 2173 FM Lesson 4 Tutorial (Additional)Ashvin Kaur100% (1)

- ACCOUNTINGDocument27 pagesACCOUNTINGUzzal HaquePas encore d'évaluation

- 911 BIZ201 Assessment 3 Student WorkbookDocument7 pages911 BIZ201 Assessment 3 Student WorkbookAkshita ChordiaPas encore d'évaluation

- Cafe Monte BiancoDocument21 pagesCafe Monte BiancoWilliam Torrez OrozcoPas encore d'évaluation

- ReportDocument8 pagesReportZain AliPas encore d'évaluation

- FM Aaj KaDocument15 pagesFM Aaj Kakaranzen50% (2)

- Cash Flow Analysis: Selected Item 2019 ($M) 2018 ($M) 2017 ($M) 2016 ($M)Document7 pagesCash Flow Analysis: Selected Item 2019 ($M) 2018 ($M) 2017 ($M) 2016 ($M)fintech100% (1)

- Petron Corporation Vertical Analysis of Balance Sheet RatiosDocument2 pagesPetron Corporation Vertical Analysis of Balance Sheet RatiosMeyPas encore d'évaluation

- Capital Budgeting Methods and Cash Flow AnalysisDocument42 pagesCapital Budgeting Methods and Cash Flow AnalysiskornelusPas encore d'évaluation

- FIn 201 AnswersDocument5 pagesFIn 201 AnswersShahinPas encore d'évaluation

- Kota Fibres ExhibitsDocument13 pagesKota Fibres ExhibitsHaemiwan FathonyPas encore d'évaluation

- Boston Creamery Case StudyDocument3 pagesBoston Creamery Case Studypathak2277Pas encore d'évaluation

- PGPM FLEX MIDTERM Danforth - Donnalley Laundry Products CompanyDocument3 pagesPGPM FLEX MIDTERM Danforth - Donnalley Laundry Products Companyhayagreevan vPas encore d'évaluation

- Butler Lumber CoDocument2 pagesButler Lumber Cokumarsharma123Pas encore d'évaluation

- Income Statement SimDocument5 pagesIncome Statement Simjustwon100% (1)

- Problem 9-30Document15 pagesProblem 9-30Lê Chấn PhongPas encore d'évaluation

- Eyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsDocument5 pagesEyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsSofía MargaritaPas encore d'évaluation

- The Quaker Oats Company and Subsidiaries Consolidated Statements of IncomeDocument3 pagesThe Quaker Oats Company and Subsidiaries Consolidated Statements of IncomeNaseer AhmedPas encore d'évaluation

- MCD2010 - T8 SolutionsDocument9 pagesMCD2010 - T8 SolutionsJasonPas encore d'évaluation

- Accrual Accounting and ValuationDocument49 pagesAccrual Accounting and ValuationSonyaTanSiYing100% (1)

- TN 7Document11 pagesTN 7patternprojectPas encore d'évaluation

- Consolidated Income StatementsDocument34 pagesConsolidated Income StatementsJuBin DeliwalaPas encore d'évaluation

- Anagene Case StudyDocument1 pageAnagene Case StudySam Man0% (3)

- Petron Corp Financial AnalysisDocument2 pagesPetron Corp Financial AnalysisNeil NaduaPas encore d'évaluation

- Abbott AnalysisDocument35 pagesAbbott Analysisahmad bilal sabirPas encore d'évaluation

- Ch15 SolnsDocument3 pagesCh15 SolnskerenkangPas encore d'évaluation

- Sweet Dreams Inc. Case AnalysisDocument13 pagesSweet Dreams Inc. Case Analysisdontcare3267% (3)

- Eataly restaurant financialsDocument20 pagesEataly restaurant financialsJanua CoeliPas encore d'évaluation

- XLS915-XLS-ENG DesarrolladoDocument10 pagesXLS915-XLS-ENG DesarrolladoYessu Amhed Condori RavichaguaPas encore d'évaluation

- Case Study On B.J. Plastic Molding Company: Submitted By: Aziz Ullah KhanDocument4 pagesCase Study On B.J. Plastic Molding Company: Submitted By: Aziz Ullah KhanNitika GabaPas encore d'évaluation

- MFAAssessment IDocument10 pagesMFAAssessment IManoj PPas encore d'évaluation

- Hampton MachineDocument7 pagesHampton MachineMurali SubramaniamPas encore d'évaluation

- Real Options and Capital Budgeting (I Wish I Had A Crystal Ball)Document4 pagesReal Options and Capital Budgeting (I Wish I Had A Crystal Ball)Ian S. DaosPas encore d'évaluation

- Accounting and Finance Chapter SolutionsDocument14 pagesAccounting and Finance Chapter SolutionsNayyar Abbas0% (1)

- Just For Feet Working Capital Management Case Study - Current Ratio, Quick Ratio, Inventory Turnover AnalysisDocument3 pagesJust For Feet Working Capital Management Case Study - Current Ratio, Quick Ratio, Inventory Turnover AnalysisAshim KarPas encore d'évaluation

- Abington-Hill Toys Financial Ratio Analysis Reveals High Risk ConditionDocument6 pagesAbington-Hill Toys Financial Ratio Analysis Reveals High Risk ConditionYafei Zhang100% (1)

- Final Report On Attock - IbfDocument25 pagesFinal Report On Attock - IbfSanam Aamir0% (1)

- Abhishek Industries Annual Report 2009-2010Document63 pagesAbhishek Industries Annual Report 2009-2010raovarun8Pas encore d'évaluation

- Financial Ratios NestleDocument23 pagesFinancial Ratios NestleSehrash SashaPas encore d'évaluation

- Optimizing Cash Flow Through Accounts Payable ManagementDocument9 pagesOptimizing Cash Flow Through Accounts Payable Managementarzoo26Pas encore d'évaluation

- Assets Liabilities & Net Worth: Check 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 28,127Document7 pagesAssets Liabilities & Net Worth: Check 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 28,127Sofía MargaritaPas encore d'évaluation

- Cost Accounting and Control OutputDocument21 pagesCost Accounting and Control OutputApril Joy ObedozaPas encore d'évaluation

- Problem 11-14 Kirsi Products 1: East Division's ROI For Last YearDocument2 pagesProblem 11-14 Kirsi Products 1: East Division's ROI For Last YearJevinPas encore d'évaluation

- KUANGLU RESTAURANT , BUSINESS PLANDocument10 pagesKUANGLU RESTAURANT , BUSINESS PLANDonjulie HovePas encore d'évaluation

- BWFF2013 - Exp of AssgDocument22 pagesBWFF2013 - Exp of AssgHoo LMinPas encore d'évaluation

- Candela CorporationDocument11 pagesCandela CorporationAnastasia LittsiouPas encore d'évaluation

- Eco Products Inc Final SCDocument13 pagesEco Products Inc Final SCRobert Mambo50% (2)

- Islamic Banking in Contemporary World & Islamization of Banks in PakistanDocument36 pagesIslamic Banking in Contemporary World & Islamization of Banks in PakistanSherdil MahmoodPas encore d'évaluation

- Noon Sugar Mills Financial Analysis (2005-2007Document12 pagesNoon Sugar Mills Financial Analysis (2005-2007Sherdil MahmoodPas encore d'évaluation

- Strategic Cost Management - Chapter 2 1Document4 pagesStrategic Cost Management - Chapter 2 1luistrosamaralainePas encore d'évaluation

- Indian Stock Market Performance After LPGDocument77 pagesIndian Stock Market Performance After LPGRavi SutharPas encore d'évaluation

- OSM3A-E Accounting02 Ngojo Report Chapter 5Document55 pagesOSM3A-E Accounting02 Ngojo Report Chapter 5Patrick Antony NgojoPas encore d'évaluation

- Native Bush Spices Australia Strategic PlanDocument10 pagesNative Bush Spices Australia Strategic PlanPersatuan Ekonomi Usahawan BumiputeraPas encore d'évaluation

- Careers in Credit and BankingDocument33 pagesCareers in Credit and BankingPrajwal WakharePas encore d'évaluation

- Full Download Advanced Accounting 13th Edition Beams Solutions ManualDocument36 pagesFull Download Advanced Accounting 13th Edition Beams Solutions Manualjacksongubmor100% (34)

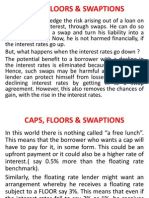

- Five-Caps, Floors & Swaptions 8Document8 pagesFive-Caps, Floors & Swaptions 8Akhilesh SinghPas encore d'évaluation

- Goodwill For Sole Proprietors and Partnerships: Frank Wood's Business Accounting 1, 12Document30 pagesGoodwill For Sole Proprietors and Partnerships: Frank Wood's Business Accounting 1, 12F2070 CHOO KEN HWAPas encore d'évaluation

- Annual Report: March 31, 2011Document23 pagesAnnual Report: March 31, 2011VALUEWALK LLCPas encore d'évaluation

- Stockholder'S Equity: CompositionDocument4 pagesStockholder'S Equity: Compositionalfred_gabriel_1Pas encore d'évaluation

- Depreciation MethodsDocument21 pagesDepreciation MethodsPawan PoynauthPas encore d'évaluation

- Paper 7 - Financial MarketsDocument52 pagesPaper 7 - Financial MarketsBogey PrettyPas encore d'évaluation

- Syailendra Pendapatan Tetap PremiumDocument1 pageSyailendra Pendapatan Tetap PremiumAldo FerlyPas encore d'évaluation

- Altana Optional View (June 2018) 'Skews'Document3 pagesAltana Optional View (June 2018) 'Skews'BlundersPas encore d'évaluation

- Cpale Simulation ExamDocument12 pagesCpale Simulation ExamGenivy SalidoPas encore d'évaluation

- Unit-4 Study MaterialDocument19 pagesUnit-4 Study MaterialSETHUMADHAVAN BPas encore d'évaluation

- Three Steps Forward, Two Steps Back by FreshDocument8 pagesThree Steps Forward, Two Steps Back by FreshTom UhlhornPas encore d'évaluation

- Lesson 3 Profit or LossDocument28 pagesLesson 3 Profit or Lossgatdula.hannahlulu.burgosPas encore d'évaluation

- Quantitative Analyst Chicago Neuberger BermanDocument2 pagesQuantitative Analyst Chicago Neuberger BermanYue CongluPas encore d'évaluation

- TB - Chapter05 - RISK AND RATES OF RETURNDocument86 pagesTB - Chapter05 - RISK AND RATES OF RETURNĐặng Văn TânPas encore d'évaluation

- ZEE Q4FY20 RESULT UPDATEDocument5 pagesZEE Q4FY20 RESULT UPDATEArpit JhanwarPas encore d'évaluation

- T I C A P: Foundation Examinations Autumn 2008Document4 pagesT I C A P: Foundation Examinations Autumn 2008adnanPas encore d'évaluation

- PresentationDocument29 pagesPresentationpermafrostXx0% (1)

- Assignments-Mba Sem-Ii: Subject Code: MB0029Document28 pagesAssignments-Mba Sem-Ii: Subject Code: MB0029Mithesh KumarPas encore d'évaluation

- Case 06 Financial Detective 2016 F1763XDocument6 pagesCase 06 Financial Detective 2016 F1763XJosie KomiPas encore d'évaluation

- Intermediate Accounting 8th Edition Spiceland Solutions Manual DownloadDocument94 pagesIntermediate Accounting 8th Edition Spiceland Solutions Manual DownloadKenneth Travis100% (28)

- Questions & Answers: Cbse Economic Studies Grade 11Document7 pagesQuestions & Answers: Cbse Economic Studies Grade 11MonahVallenosMirandaPas encore d'évaluation