Vous aimerez peut-être aussi

- Econometrics Notes PDFDocument8 pagesEconometrics Notes PDFumamaheswariPas encore d'évaluation

- IntroEconmerics AcFn 5031 (q1)Document302 pagesIntroEconmerics AcFn 5031 (q1)yesuneh98Pas encore d'évaluation

- Multicollinearity Among The Regressors Included in The Regression ModelDocument13 pagesMulticollinearity Among The Regressors Included in The Regression ModelNavyashree B MPas encore d'évaluation

- DP1HL1 IntroDocument85 pagesDP1HL1 IntroSenam DzakpasuPas encore d'évaluation

- Homoscedastic That Is, They All Have The Same Variance: HeteroscedasticityDocument11 pagesHomoscedastic That Is, They All Have The Same Variance: HeteroscedasticityNavyashree B M100% (1)

- DummyDocument20 pagesDummymushtaque61Pas encore d'évaluation

- Public Finance SolutionDocument24 pagesPublic Finance SolutionChan Zachary100% (1)

- Chapter 6 Dummy Variable AssignmentDocument4 pagesChapter 6 Dummy Variable Assignmentharis100% (1)

- Studenmund Ch01 v2Document31 pagesStudenmund Ch01 v2tsy0703Pas encore d'évaluation

- AutocorrelationDocument172 pagesAutocorrelationJenab Peteburoh100% (1)

- Stationarity and Unit Root TestingDocument21 pagesStationarity and Unit Root TestingAwAtef LHPas encore d'évaluation

- Regression TechniquesDocument5 pagesRegression Techniquesvisu009Pas encore d'évaluation

- Topic 6 Two Variable Regression Analysis Interval Estimation and Hypothesis TestingDocument36 pagesTopic 6 Two Variable Regression Analysis Interval Estimation and Hypothesis TestingOliver Tate-DuncanPas encore d'évaluation

- HeteroscedasticityDocument7 pagesHeteroscedasticityBristi RodhPas encore d'évaluation

- Financial Econometrics 2010-2011Document483 pagesFinancial Econometrics 2010-2011axelkokocur100% (1)

- Complete Business Statistics: Simple Linear Regression and CorrelationDocument50 pagesComplete Business Statistics: Simple Linear Regression and Correlationmallick5051rajatPas encore d'évaluation

- Econometrics Ch6 ApplicationsDocument49 pagesEconometrics Ch6 ApplicationsMihaela SirițanuPas encore d'évaluation

- Module 2 - Research MethodologyDocument18 pagesModule 2 - Research MethodologyPRATHAM MOTWANI100% (1)

- Unbalanced Panel Data PDFDocument51 pagesUnbalanced Panel Data PDFrbmalasaPas encore d'évaluation

- Final Project - Climate Change PlanDocument32 pagesFinal Project - Climate Change PlanHannah LeePas encore d'évaluation

- Micro Perfect and MonopolyDocument57 pagesMicro Perfect and Monopolytegegn mogessiePas encore d'évaluation

- 178.200 06-4Document34 pages178.200 06-4api-3860979Pas encore d'évaluation

- Introduction To Introduction To Econometrics Econometrics Econometrics Econometrics (ECON 352) (ECON 352)Document12 pagesIntroduction To Introduction To Econometrics Econometrics Econometrics Econometrics (ECON 352) (ECON 352)Nhatty Wero100% (2)

- Term Paper Eco No MetricDocument34 pagesTerm Paper Eco No MetricmandeepkumardagarPas encore d'évaluation

- Panel Econometrics HistoryDocument65 pagesPanel Econometrics HistoryNaresh SehdevPas encore d'évaluation

- Business Economics MainDocument8 pagesBusiness Economics MainJaskaran MannPas encore d'évaluation

- Ex08 PDFDocument29 pagesEx08 PDFSalman FarooqPas encore d'évaluation

- Solution Manual For Using Econometrics A Practical Guide 6 e 6th Edition A H StudenmundDocument6 pagesSolution Manual For Using Econometrics A Practical Guide 6 e 6th Edition A H Studenmundlyalexanderzh52Pas encore d'évaluation

- Chapter # 6: Multiple Regression Analysis: The Problem of EstimationDocument43 pagesChapter # 6: Multiple Regression Analysis: The Problem of EstimationRas DawitPas encore d'évaluation

- 3 Multiple Linear Regression: Estimation and Properties: Ezequiel Uriel Universidad de Valencia Version: 09-2013Document37 pages3 Multiple Linear Regression: Estimation and Properties: Ezequiel Uriel Universidad de Valencia Version: 09-2013penyia100% (1)

- Introduction To Econometrics - Stock & Watson - CH 12 SlidesDocument46 pagesIntroduction To Econometrics - Stock & Watson - CH 12 SlidesAntonio AlvinoPas encore d'évaluation

- Chap 8 AnswersDocument7 pagesChap 8 Answerssharoz0saleemPas encore d'évaluation

- Structure Project Topics For Projects 2016Document4 pagesStructure Project Topics For Projects 2016Mariu VornicuPas encore d'évaluation

- Dev't PPA I (Chap-4)Document48 pagesDev't PPA I (Chap-4)ferewe tesfaye100% (1)

- Chapter 1: The Nature of Econometrics and Economic Data: Ruslan AliyevDocument27 pagesChapter 1: The Nature of Econometrics and Economic Data: Ruslan AliyevMurselPas encore d'évaluation

- Multiple Choice Test Bank Questions No Feedback - Chapter 3: y + X + X + X + UDocument3 pagesMultiple Choice Test Bank Questions No Feedback - Chapter 3: y + X + X + X + Uimam awaluddinPas encore d'évaluation

- Statistics For EconomicsDocument58 pagesStatistics For EconomicsKintu GeraldPas encore d'évaluation

- The Three Box Solution Cheat SheetDocument1 pageThe Three Box Solution Cheat SheetAndrea CattaneoPas encore d'évaluation

- Hoff (2000), 'The Modern Theory of Underdevelopment Traps'Document58 pagesHoff (2000), 'The Modern Theory of Underdevelopment Traps'Joe OglePas encore d'évaluation

- Liquidity Preference As Behavior Towards Risk Review of Economic StudiesDocument23 pagesLiquidity Preference As Behavior Towards Risk Review of Economic StudiesCuenta EliminadaPas encore d'évaluation

- Autocorrelation: What Happens If The Error Terms Are Correlated?Document18 pagesAutocorrelation: What Happens If The Error Terms Are Correlated?Nusrat Jahan MoonPas encore d'évaluation

- Financial Econometrics IntroductionDocument13 pagesFinancial Econometrics IntroductionPrabath Suranaga MorawakagePas encore d'évaluation

- Nature of Regression AnalysisDocument22 pagesNature of Regression Analysiswhoosh2008Pas encore d'évaluation

- Economics Unit OutlineDocument8 pagesEconomics Unit OutlineHaris APas encore d'évaluation

- Sample Exam Questions (And Answers)Document22 pagesSample Exam Questions (And Answers)Diem Hang VuPas encore d'évaluation

- Cases RCCDocument41 pagesCases RCCrderijkPas encore d'évaluation

- CAPMDocument34 pagesCAPMadityav_13100% (1)

- 1-Value at Risk (Var) Models, Methods & Metrics - Excel Spreadsheet Walk Through Calculating Value at Risk (Var) - Comparing Var Models, Methods & MetricsDocument65 pages1-Value at Risk (Var) Models, Methods & Metrics - Excel Spreadsheet Walk Through Calculating Value at Risk (Var) - Comparing Var Models, Methods & MetricsVaibhav KharadePas encore d'évaluation

- Unit 9 Linear Regression: StructureDocument18 pagesUnit 9 Linear Regression: StructurePranav ViswanathanPas encore d'évaluation

- Economics Open Closed SystemsDocument37 pagesEconomics Open Closed Systemsmahathir rafsanjaniPas encore d'évaluation

- Solution For HW 1Document15 pagesSolution For HW 1Ashtar Ali Bangash0% (1)

- AutocorrelationDocument46 pagesAutocorrelationBabar AdeebPas encore d'évaluation

- Multiple Linear Regression: y BX BX BXDocument14 pagesMultiple Linear Regression: y BX BX BXPalaniappan SellappanPas encore d'évaluation

- Chap 013Document67 pagesChap 013Bruno MarinsPas encore d'évaluation

- Harvard Economics 2020a Problem Set 3Document2 pagesHarvard Economics 2020a Problem Set 3JPas encore d'évaluation

- Micro Chapter 04Document15 pagesMicro Chapter 04deeptitripathi09Pas encore d'évaluation

- Weil GrowthDocument72 pagesWeil GrowthJavier Burbano ValenciaPas encore d'évaluation

- TAPPI T 810 Om-06 Bursting Strength of Corrugated and Solid FiberboardDocument5 pagesTAPPI T 810 Om-06 Bursting Strength of Corrugated and Solid FiberboardNguyenSongHaoPas encore d'évaluation

- ASM1 ProgramingDocument14 pagesASM1 ProgramingTran Cong Hoang (BTEC HN)Pas encore d'évaluation

- Plantas Con Madre Plants That Teach and PDFDocument15 pagesPlantas Con Madre Plants That Teach and PDFJetPas encore d'évaluation

- Trainer Manual Internal Quality AuditDocument32 pagesTrainer Manual Internal Quality AuditMuhammad Erwin Yamashita100% (5)

- OMN-TRA-SSR-OETC-Course Workbook 2daysDocument55 pagesOMN-TRA-SSR-OETC-Course Workbook 2daysMANIKANDAN NARAYANASAMYPas encore d'évaluation

- Successful School LeadershipDocument132 pagesSuccessful School LeadershipDabney90100% (2)

- Schematic Circuits: Section C - ElectricsDocument1 pageSchematic Circuits: Section C - ElectricsIonut GrozaPas encore d'évaluation

- Ems Speed Sensor Com MotorDocument24 pagesEms Speed Sensor Com MotorKarina RickenPas encore d'évaluation

- CH 2 PDFDocument85 pagesCH 2 PDFSajidPas encore d'évaluation

- File 1038732040Document70 pagesFile 1038732040Karen Joyce Costales MagtanongPas encore d'évaluation

- Civil Engineering Literature Review SampleDocument6 pagesCivil Engineering Literature Review Sampleea442225100% (1)

- Modicon PLC CPUS Technical Details.Document218 pagesModicon PLC CPUS Technical Details.TrbvmPas encore d'évaluation

- Top249 1 PDFDocument52 pagesTop249 1 PDFCarlos Henrique Dos SantosPas encore d'évaluation

- ILI9481 DatasheetDocument143 pagesILI9481 DatasheetdetonatPas encore d'évaluation

- BS en 50216-6 2002Document18 pagesBS en 50216-6 2002Jeff Anderson Collins100% (3)

- Parts List 38 254 13 95: Helical-Bevel Gear Unit KA47, KH47, KV47, KT47, KA47B, KH47B, KV47BDocument4 pagesParts List 38 254 13 95: Helical-Bevel Gear Unit KA47, KH47, KV47, KT47, KA47B, KH47B, KV47BEdmundo JavierPas encore d'évaluation

- LampiranDocument26 pagesLampiranSekar BeningPas encore d'évaluation

- Chapter 3 PayrollDocument5 pagesChapter 3 PayrollPheng Tiosen100% (2)

- Angelina JolieDocument14 pagesAngelina Joliemaria joannah guanteroPas encore d'évaluation

- Boq Cme: 1 Pole Foundation Soil WorkDocument1 pageBoq Cme: 1 Pole Foundation Soil WorkyuwonoPas encore d'évaluation

- Amberjet™ 1500 H: Industrial Grade Strong Acid Cation ExchangerDocument2 pagesAmberjet™ 1500 H: Industrial Grade Strong Acid Cation ExchangerJaime SalazarPas encore d'évaluation

- Change LogDocument145 pagesChange LogelhohitoPas encore d'évaluation

- Remediation of AlphabetsDocument34 pagesRemediation of AlphabetsAbdurahmanPas encore d'évaluation

- Harish Raval Rajkot.: Civil ConstructionDocument4 pagesHarish Raval Rajkot.: Civil ConstructionNilay GandhiPas encore d'évaluation

- JOB Performer: Q .1: What Is Permit?Document5 pagesJOB Performer: Q .1: What Is Permit?Shahid BhattiPas encore d'évaluation

- Cable Schedule - Instrument - Surfin - Malanpur-R0Document3 pagesCable Schedule - Instrument - Surfin - Malanpur-R0arunpandey1686Pas encore d'évaluation

- EHVACDocument16 pagesEHVACsidharthchandak16Pas encore d'évaluation

- Citing Correctly and Avoiding Plagiarism: MLA Format, 7th EditionDocument4 pagesCiting Correctly and Avoiding Plagiarism: MLA Format, 7th EditionDanish muinPas encore d'évaluation

- Cognitive-Behavioral Interventions For PTSDDocument20 pagesCognitive-Behavioral Interventions For PTSDBusyMindsPas encore d'évaluation

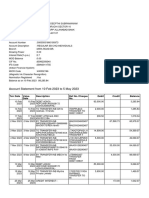

- Feb-May SBI StatementDocument2 pagesFeb-May SBI StatementAshutosh PandeyPas encore d'évaluation