Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Final FIN 200 (All Chapters) FIXEDDocument65 pagesFinal FIN 200 (All Chapters) FIXEDMunPas encore d'évaluation

- Advance Accounting 2 by GuerreroDocument13 pagesAdvance Accounting 2 by Guerreromarycayton100% (7)

- Functions of Business FinanceDocument6 pagesFunctions of Business FinancePrincess AudreyPas encore d'évaluation

- Tax Laws in Tanzania: Taxation Questions & AnswersDocument11 pagesTax Laws in Tanzania: Taxation Questions & AnswersKessy Juma90% (119)

- Financial Management & Policy by James C. Van Horne 12th EditionDocument832 pagesFinancial Management & Policy by James C. Van Horne 12th EditionKashif Mirza82% (34)

- Question and Answer - 49Document30 pagesQuestion and Answer - 49acc-expertPas encore d'évaluation

- Financial Statement Analysis (Fsa)Document32 pagesFinancial Statement Analysis (Fsa)Shashank100% (1)

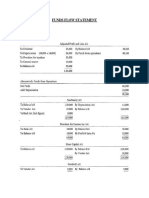

- Funds Flow Statement: Numerical 1Document4 pagesFunds Flow Statement: Numerical 1Neelu AhluwaliaPas encore d'évaluation

- FM Assignment 1Document8 pagesFM Assignment 1SAKSHAM ARJANIPas encore d'évaluation

- Why I Increase My HDMF - Pag-IBIG Contribution - Cebu AccountantDocument4 pagesWhy I Increase My HDMF - Pag-IBIG Contribution - Cebu Accountantmarkanthony_alvario2946Pas encore d'évaluation

- Blackstone 2 Q 22 Earnings Press ReleaseDocument41 pagesBlackstone 2 Q 22 Earnings Press ReleaseLinh Linh NguyenPas encore d'évaluation

- The Product Life Cycle: Understanding Financials Through PhasesDocument9 pagesThe Product Life Cycle: Understanding Financials Through PhasesYuka Tarantoro100% (1)

- Apple Q3 FY19 Consolidated Financial StatementsDocument3 pagesApple Q3 FY19 Consolidated Financial StatementsJack PurcherPas encore d'évaluation

- UMEME 2021 financial results reflect recovery from Covid impactsDocument2 pagesUMEME 2021 financial results reflect recovery from Covid impactsTrial MeisterPas encore d'évaluation

- Project Company Law Ii Sem 6Document13 pagesProject Company Law Ii Sem 6gauravPas encore d'évaluation

- FM 101 Chapter 2 (Cabrera)Document17 pagesFM 101 Chapter 2 (Cabrera)Chelsea PagcaliwaganPas encore d'évaluation

- Measuring Bank Performance & Risk with Key RatiosDocument45 pagesMeasuring Bank Performance & Risk with Key RatiospavithragowthamnsPas encore d'évaluation

- Dokumen - Tips - Laporan Keuangan 5671d4081a509 PDFDocument187 pagesDokumen - Tips - Laporan Keuangan 5671d4081a509 PDFAgustinus Dwichandra12Pas encore d'évaluation

- Intermediate Accountig AkuntansiDocument46 pagesIntermediate Accountig AkuntansiRika LerianiPas encore d'évaluation

- Carlos F Lucero Financial Disclosure Report For 2010Document8 pagesCarlos F Lucero Financial Disclosure Report For 2010Judicial Watch, Inc.Pas encore d'évaluation

- Ratio Analysis of Infowiz Pvt LtdDocument39 pagesRatio Analysis of Infowiz Pvt LtdRahul Mehta0% (1)

- Fy 2016 AuditedDocument222 pagesFy 2016 AuditedError 707Pas encore d'évaluation

- Dividend Theories and LimitationsDocument11 pagesDividend Theories and LimitationsPerah MemonPas encore d'évaluation

- Answer KeyDocument5 pagesAnswer KeyYhancie Mae TorresPas encore d'évaluation

- Module 5 - Profit and Loss Trainer HandoutDocument7 pagesModule 5 - Profit and Loss Trainer Handoutapplefox2022Pas encore d'évaluation

- What Amount Should Be Reported As Diluted Earnings Per Share?Document6 pagesWhat Amount Should Be Reported As Diluted Earnings Per Share?carinaPas encore d'évaluation

- IGCSE-OL - Bus - CH - 5 - Answers To CB ActivitiesDocument3 pagesIGCSE-OL - Bus - CH - 5 - Answers To CB ActivitiesAdrián CastilloPas encore d'évaluation

- 19 Answer Key PDFDocument23 pages19 Answer Key PDFBianca BazanPas encore d'évaluation

- Final Project Report in 1Document91 pagesFinal Project Report in 1MKamranDanish100% (1)

- Business Tax Laws in The PhilippinesDocument12 pagesBusiness Tax Laws in The PhilippinesEthel Joi Manalac MendozaPas encore d'évaluation