Vous aimerez peut-être aussi

- CNLU Research Project on Treasury BillsDocument14 pagesCNLU Research Project on Treasury BillsDeepak ChauhanPas encore d'évaluation

- IPO Book Building GuideDocument29 pagesIPO Book Building GuideWashim SarkarPas encore d'évaluation

- DMEE ConfigurationDocument45 pagesDMEE Configurationgnikisi-1100% (1)

- IPO Book Building ExplainedDocument12 pagesIPO Book Building ExplainedPriyambada DasPas encore d'évaluation

- What Is It Book BuildingDocument5 pagesWhat Is It Book BuildingPratik N. PatelPas encore d'évaluation

- Book Building MechanismDocument18 pagesBook Building MechanismMohan Bedrodi100% (1)

- Issue Type Offer Price Demand Payment ReservationsDocument14 pagesIssue Type Offer Price Demand Payment ReservationssmileysashiPas encore d'évaluation

- BOOK BUILDING ACTS AS SCIENTIFIC METHOD FOR DETERMINING IPO PRICESDocument9 pagesBOOK BUILDING ACTS AS SCIENTIFIC METHOD FOR DETERMINING IPO PRICESLin Jian Hui EricPas encore d'évaluation

- Overview and Executive SummaryDocument61 pagesOverview and Executive SummaryAkshay SablePas encore d'évaluation

- Book BuildingDocument19 pagesBook Buildingmonilsonaiya_91Pas encore d'évaluation

- 2011012945COM15109GE14Unit 2nd Red Herring Prospectus and Book Building Mechanism Explainedred herringDocument34 pages2011012945COM15109GE14Unit 2nd Red Herring Prospectus and Book Building Mechanism Explainedred herringLone AryanPas encore d'évaluation

- Book BuildingDocument3 pagesBook Buildingrupika_borntowin2Pas encore d'évaluation

- IpoDocument3 pagesIpoVinod GudimaniPas encore d'évaluation

- Unit - Iv: Security Markets: Stock ExchangesDocument99 pagesUnit - Iv: Security Markets: Stock Exchangesjagrutisolanki01Pas encore d'évaluation

- Initial Public OfferDocument29 pagesInitial Public OfferAjay MadaanPas encore d'évaluation

- FinalDocument29 pagesFinalapi-3732797Pas encore d'évaluation

- Book BuildingDocument24 pagesBook Buildingmariam_abbasi5100% (2)

- Security Analysis: Semester III, Class of 2009 ICFAI Business School Capital Issue (Session 4) Nupur HetamsariaDocument18 pagesSecurity Analysis: Semester III, Class of 2009 ICFAI Business School Capital Issue (Session 4) Nupur Hetamsariaattitudefirstpankaj8625Pas encore d'évaluation

- Project Report: Public Issue (Book Building Method)Document21 pagesProject Report: Public Issue (Book Building Method)Saurabh BandekarPas encore d'évaluation

- Primary Issue: What Is Book Building?Document9 pagesPrimary Issue: What Is Book Building?mitalptPas encore d'évaluation

- Analysis On Public IssueDocument21 pagesAnalysis On Public IssueSaurabh BandekarPas encore d'évaluation

- Book BuildingDocument3 pagesBook BuildingrvgrockerPas encore d'évaluation

- Initial Public Offering: How Companies List On The Stock ExchangeDocument2 pagesInitial Public Offering: How Companies List On The Stock ExchangeRadha KaushikPas encore d'évaluation

- About Public Issues: More About Book BuildingDocument6 pagesAbout Public Issues: More About Book BuildingBalaji RavigopalPas encore d'évaluation

- Book BuildingDocument40 pagesBook Buildingvineet ranjanPas encore d'évaluation

- What Is An Initial Public OfferDocument4 pagesWhat Is An Initial Public OfferGadmali YadavPas encore d'évaluation

- Concepts and Process of Book BuildingDocument4 pagesConcepts and Process of Book BuildingGopalsamy SelvaduraiPas encore d'évaluation

- What Is A Red Herring?Document4 pagesWhat Is A Red Herring?Dev Kamal ChauhanPas encore d'évaluation

- Bombay Stock ExchangeDocument10 pagesBombay Stock Exchangeaddy9760Pas encore d'évaluation

- Book Building IPO GuideDocument2 pagesBook Building IPO GuideSarada NagPas encore d'évaluation

- Financial Markets & Services: Assignment - 1Document18 pagesFinancial Markets & Services: Assignment - 1Rita AgrawalPas encore d'évaluation

- Bookbuilding 1Document7 pagesBookbuilding 1Shibu AbrahamPas encore d'évaluation

- Book Building ProcessDocument17 pagesBook Building Processmukesha.kr100% (9)

- Ipo Book BuildingDocument12 pagesIpo Book BuildingGaurav DwivediPas encore d'évaluation

- Security Analysis and Portfolio Management: Presented By, Saitha MeeranDocument8 pagesSecurity Analysis and Portfolio Management: Presented By, Saitha Meeransaidha meeranPas encore d'évaluation

- Book BuildingDocument7 pagesBook BuildingAnonymous 3yqNzCxtTzPas encore d'évaluation

- Equity Share Public IssuesDocument9 pagesEquity Share Public IssuesmyselfmeriPas encore d'évaluation

- Capital Market - Part-6 - Book Building and Buy-BackDocument7 pagesCapital Market - Part-6 - Book Building and Buy-Backenvim66Pas encore d'évaluation

- Financial Management: Class of 2011 ICFAI Business School Ipos (Session 26)Document19 pagesFinancial Management: Class of 2011 ICFAI Business School Ipos (Session 26)shashankkapur22Pas encore d'évaluation

- Book BuildingDocument2 pagesBook Buildingpriyesh04Pas encore d'évaluation

- Book BuildingDocument2 pagesBook BuildinghmgamitPas encore d'évaluation

- ABC of Primary MarketDocument34 pagesABC of Primary MarketNaveen RanaPas encore d'évaluation

- 209 - F - IndiabullsDocument75 pages209 - F - IndiabullsPeacock Live ProjectsPas encore d'évaluation

- Chapter-2 Review of LiteratureDocument54 pagesChapter-2 Review of Literaturebalki123Pas encore d'évaluation

- Primary MarketDocument25 pagesPrimary Marketkunaldaga78Pas encore d'évaluation

- Initial Public Offering (IPO)Document5 pagesInitial Public Offering (IPO)Sarvepalli JwalachaitanyakumarPas encore d'évaluation

- Ipo Book Bldg.Document32 pagesIpo Book Bldg.Akanksha RajanPas encore d'évaluation

- Red Herring Prospectus & Initial Public OfferingDocument8 pagesRed Herring Prospectus & Initial Public OfferingMathan RajPas encore d'évaluation

- IPO and Its ProcessDocument4 pagesIPO and Its ProcessNaveen JohnPas encore d'évaluation

- IPO Guide: Initial Public Offering ProcessDocument22 pagesIPO Guide: Initial Public Offering ProcessP.h. ModiPas encore d'évaluation

- Cash Money Markets: Minimum Correct Answers For This Module: 6/12Document15 pagesCash Money Markets: Minimum Correct Answers For This Module: 6/12Jovan SsenkandwaPas encore d'évaluation

- BidForm MGLDocument2 pagesBidForm MGLanu radhaPas encore d'évaluation

- Indian Securities Market GuideDocument52 pagesIndian Securities Market GuideAdarsh SaxenaPas encore d'évaluation

- Session 3-4 - FISMDocument17 pagesSession 3-4 - FISMHarshil ShahPas encore d'évaluation

- Financial Markets FinalsDocument49 pagesFinancial Markets FinalsKevin PrincePas encore d'évaluation

- Basic of Stock MarketDocument5 pagesBasic of Stock MarketAnkit ChauhanPas encore d'évaluation

- Gurjantt IPO MarketDocument29 pagesGurjantt IPO MarkettomcruisePas encore d'évaluation

- Summary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoD'EverandSummary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoPas encore d'évaluation

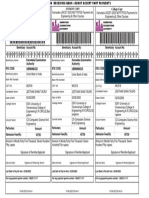

- Challan KPCET3AL079E810085 14022023 182210Document1 pageChallan KPCET3AL079E810085 14022023 182210PavanPas encore d'évaluation

- Gurukulworld Schoolpad in externalApiManager printCertificateAlreadyGeneratedApi MTAyMA MZK MTgzNDA MTMDocument2 pagesGurukulworld Schoolpad in externalApiManager printCertificateAlreadyGeneratedApi MTAyMA MZK MTgzNDA MTMFor subscribing channels ytPas encore d'évaluation

- Apply for Interbank Funds TransferDocument2 pagesApply for Interbank Funds TransferEr Mosin ShaikhPas encore d'évaluation

- MNCL - ALL - BankDetailsDocument1 pageMNCL - ALL - BankDetailsyagnesh2610Pas encore d'évaluation

- Payment 1Document7 pagesPayment 1peacetours andtravels07Pas encore d'évaluation

- Pankaj Meena 9782898891 South Nts 312r, 312bDocument2 pagesPankaj Meena 9782898891 South Nts 312r, 312bgaurav580Pas encore d'évaluation

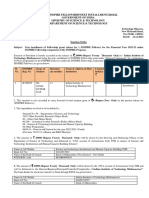

- Fellowship - Consolidated - Sanction - Order - 2022-23 (List-4) PDFDocument80 pagesFellowship - Consolidated - Sanction - Order - 2022-23 (List-4) PDFShubh tiwari TiwariPas encore d'évaluation

- JR AgrometDocument12 pagesJR AgrometPritam DasPas encore d'évaluation

- Request For Electronic Policy Payout: Policy Number Name of Policy Holder Aadhaar Number PAN Mobile NumberDocument1 pageRequest For Electronic Policy Payout: Policy Number Name of Policy Holder Aadhaar Number PAN Mobile Numberrovensingh007Pas encore d'évaluation

- Fee Structure 2021-22Document4 pagesFee Structure 2021-22harsh bhargavaPas encore d'évaluation

- NEFTDocument6 pagesNEFTParoj DuttaPas encore d'évaluation

- Yelahanka IFC Number - Google SearchDocument1 pageYelahanka IFC Number - Google SearchSIBU KATHULLAH SPas encore d'évaluation

- Claimant Statement Form Death Claim 2Document3 pagesClaimant Statement Form Death Claim 2Anitha AnuPas encore d'évaluation

- NEFT Vs RTGS PaymentsDocument4 pagesNEFT Vs RTGS PaymentsrajeevjprPas encore d'évaluation

- Find HDFC Bank IFSC code and address for Palwal branchDocument1 pageFind HDFC Bank IFSC code and address for Palwal branchSatish DagarPas encore d'évaluation

- Death Claimant StatementDocument4 pagesDeath Claimant Statementcet.ranchi7024Pas encore d'évaluation

- Fees Structur 2021-22Document7 pagesFees Structur 2021-22Avadhut MaliPas encore d'évaluation

- Challan KUGET2HV499G204899 09092023 210859Document1 pageChallan KUGET2HV499G204899 09092023 210859fPas encore d'évaluation

- Darshan TradingDocument61 pagesDarshan TradingShobha SinghPas encore d'évaluation

- Claimant Statement Form (Death Claims) : Customer Helpline No: 1860 266 7766Document3 pagesClaimant Statement Form (Death Claims) : Customer Helpline No: 1860 266 7766Tarun RustagiPas encore d'évaluation

- Tax invoices for Sugam Park maintenance chargesDocument62 pagesTax invoices for Sugam Park maintenance chargesKaran VermaPas encore d'évaluation

- Nationalized Electronic Funds Transfer-Mandate Form: (To Be Filled in by The Applicant in BLOCK LETTER)Document1 pageNationalized Electronic Funds Transfer-Mandate Form: (To Be Filled in by The Applicant in BLOCK LETTER)Amit BhargavaPas encore d'évaluation

- 50 - A Note On The Book Building ProcessDocument12 pages50 - A Note On The Book Building ProcessArunangshu DuttaPas encore d'évaluation

- KVB RTGS ChallanDocument2 pagesKVB RTGS ChallankohsaindiaPas encore d'évaluation

- Multinational Bank SlogansDocument55 pagesMultinational Bank SlogansSachin SahooPas encore d'évaluation

- Challan KUGET1WU518E105464 19082023 174441Document1 pageChallan KUGET1WU518E105464 19082023 174441Jeethan TauroPas encore d'évaluation

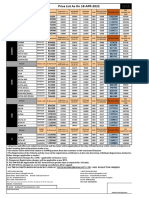

- PRICE LISTDocument1 pagePRICE LISTKolkata Jyote MotorsPas encore d'évaluation

- Npab FMTDocument7 pagesNpab FMTRAJESH DHOKALEPas encore d'évaluation

- 070123-PAI & AAI Claim FormsDocument6 pages070123-PAI & AAI Claim FormsVikas Singh ChandelPas encore d'évaluation