Vous aimerez peut-être aussi

- Profit and Loss Account For The Year Ended 31 March, 2012Document6 pagesProfit and Loss Account For The Year Ended 31 March, 2012Sandeep GalipelliPas encore d'évaluation

- Profit and Loss Account For The Year Ended 31 March, 2012Document6 pagesProfit and Loss Account For The Year Ended 31 March, 2012Sandeep GalipelliPas encore d'évaluation

- Procedure On Financing of Two-Wheeler Loan at Centurian Bank by Sneha SalgaonkarDocument57 pagesProcedure On Financing of Two-Wheeler Loan at Centurian Bank by Sneha SalgaonkarAarti Kulkarni0% (2)

- What Is IrdaDocument14 pagesWhat Is IrdaSandeep GalipelliPas encore d'évaluation

- SebiDocument18 pagesSebiSandeep Galipelli50% (2)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Analytical Procedures AreDocument3 pagesAnalytical Procedures Aresamuel debebePas encore d'évaluation

- Music License Agreement - En-GbDocument0 pageMusic License Agreement - En-GbSudeep SharmaPas encore d'évaluation

- Red Book & Internal Auditing: Presented By: Maxene M. Bardwell, CPA, CIA, CFE, CISA, CIGA, CITP, CrmaDocument78 pagesRed Book & Internal Auditing: Presented By: Maxene M. Bardwell, CPA, CIA, CFE, CISA, CIGA, CITP, CrmaАндрей МиксоновPas encore d'évaluation

- The Impact of Risk Based Audit on Financial Performance in Commercial Banks in KenyaDocument88 pagesThe Impact of Risk Based Audit on Financial Performance in Commercial Banks in KenyaAn NguyenPas encore d'évaluation

- CSWIP 3 1 Course ScheduleDocument2 pagesCSWIP 3 1 Course ScheduleDeepakPas encore d'évaluation

- C4 - Advanced TaxationDocument509 pagesC4 - Advanced TaxationtayoPas encore d'évaluation

- Anti-Money Laundering and Combating The Financing of TerrorismDocument124 pagesAnti-Money Laundering and Combating The Financing of TerrorismLaurette M. BackerPas encore d'évaluation

- MCSR (General Rules)Document78 pagesMCSR (General Rules)akshayryukPas encore d'évaluation

- What Is Change Management The Definitive GuideBonus Chapter PDFDocument78 pagesWhat Is Change Management The Definitive GuideBonus Chapter PDFAnonymous RoAnGpAPas encore d'évaluation

- Auditors LiabilityDocument2 pagesAuditors Liabilitycessd3Pas encore d'évaluation

- Companies Act, 1956Document11 pagesCompanies Act, 1956MOUSOM ROYPas encore d'évaluation

- Wema-Bank-Financial Statement-2018Document75 pagesWema-Bank-Financial Statement-2018john stonesPas encore d'évaluation

- M SamiDocument5 pagesM SamiMah rukh M.yaqoobPas encore d'évaluation

- Blank Taxi Receipt TemplateDocument4 pagesBlank Taxi Receipt TemplatedigrajPas encore d'évaluation

- CMD 735-5 (2019)Document18 pagesCMD 735-5 (2019)nguymikePas encore d'évaluation

- Fasb Concept Statement 6 PDFDocument2 pagesFasb Concept Statement 6 PDFStephaniePas encore d'évaluation

- Friends Flower Shop Quarterly ProfitDocument11 pagesFriends Flower Shop Quarterly ProfitHitesh BalPas encore d'évaluation

- Audit and Internal ReviewDocument7 pagesAudit and Internal ReviewkhengmaiPas encore d'évaluation

- Accountancy FirmDocument2 pagesAccountancy FirmAarti SarafPas encore d'évaluation

- Voluntary Winding Up and Removal of NamesDocument21 pagesVoluntary Winding Up and Removal of Namessreedevi sureshPas encore d'évaluation

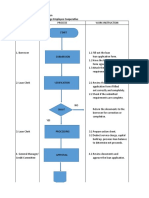

- Process Flow of Loan Application UMTEMPCO - UM Tagum College Employee CooperativeDocument4 pagesProcess Flow of Loan Application UMTEMPCO - UM Tagum College Employee CooperativeJao FloresPas encore d'évaluation

- Construction Resume SamplesDocument7 pagesConstruction Resume Samplesafjzcgeoylbkku100% (2)

- Project InternDocument12 pagesProject Internaashish dua100% (1)

- Financial Accounting Quiz - Accounting CoachDocument3 pagesFinancial Accounting Quiz - Accounting CoachSudip BhattacharyaPas encore d'évaluation

- Auditor's Responsibilities Relating The Subsequent Event in An Audit of The Financial StatementsDocument6 pagesAuditor's Responsibilities Relating The Subsequent Event in An Audit of The Financial StatementsHarutraPas encore d'évaluation

- FA PPT Group-2 NEWDocument19 pagesFA PPT Group-2 NEWRaksha ShettyPas encore d'évaluation

- Week 4 Professional StandardDocument14 pagesWeek 4 Professional StandardFITRI SAHIDAHPas encore d'évaluation

- ACCT1AB Chapter 1 PDFDocument3 pagesACCT1AB Chapter 1 PDFErica Jane Garcia DuquePas encore d'évaluation

- Norm Brodsky OneDocument243 pagesNorm Brodsky OneRock LocksleyPas encore d'évaluation

- Cash and Liquidity ManagementDocument7 pagesCash and Liquidity Managementanthonymugala100% (1)