Vous aimerez peut-être aussi

- Presented by Naman Kohli A29 Neha Sopori A31 Pravesh Phogat A Rahul Gaddh A Saurabh Rai A Sirin Sam A57Document35 pagesPresented by Naman Kohli A29 Neha Sopori A31 Pravesh Phogat A Rahul Gaddh A Saurabh Rai A Sirin Sam A57Neha Sopori100% (1)

- BANKING SYSTEM The Indian Money Market Is Classified Into: TheDocument11 pagesBANKING SYSTEM The Indian Money Market Is Classified Into: Themkprabhu100% (1)

- Banking Types and Roles in IndiaDocument24 pagesBanking Types and Roles in IndiaMayank Sharan GargPas encore d'évaluation

- Development of local currency bond markets in India: key reforms and experiencesDocument33 pagesDevelopment of local currency bond markets in India: key reforms and experiencesRohit BhardwajPas encore d'évaluation

- Banking Reforms 1991Document7 pagesBanking Reforms 1991asitbhatiaPas encore d'évaluation

- Specialized BanksDocument29 pagesSpecialized BankskhusbuPas encore d'évaluation

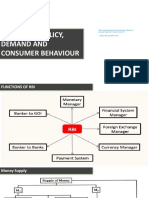

- Monetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreDocument23 pagesMonetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreBhavya NarangPas encore d'évaluation

- RBI Credit Authorization SchemeDocument6 pagesRBI Credit Authorization SchemeOngwang KonyakPas encore d'évaluation

- Jan Mar 2007 BulletinDocument17 pagesJan Mar 2007 BulletinAyeshaJangdaPas encore d'évaluation

- Union Bank Performance Report/TITLEDocument35 pagesUnion Bank Performance Report/TITLEIshank GuptaPas encore d'évaluation

- Presentation On The Articles "Priority Sector Lending and Statement of Intent "Document17 pagesPresentation On The Articles "Priority Sector Lending and Statement of Intent "Gaurav SawlaniPas encore d'évaluation

- Banking SectorDocument12 pagesBanking SectorasifanisPas encore d'évaluation

- Financial Sector Reforms in India Since 1991Document11 pagesFinancial Sector Reforms in India Since 1991AMAN KUMAR SINGHPas encore d'évaluation

- Indian financial reforms focused on banking sectorDocument10 pagesIndian financial reforms focused on banking sectornagendra yanamalaPas encore d'évaluation

- ACFrOgAIPqeduC6xn4YwZGZULnMkaBXsvoe10JiZ-5Gnt4qvbUJXSXRHFCv6h5nRQP2TLyrabhEZf-59scu6F351RDSAZxite5CfZhqyGduD7KdgdhzTwKMK4QoI9hB6T8PAPD3ipWT0lTuM-y5husUPIYygwxVMlMXT-K2USA==Document12 pagesACFrOgAIPqeduC6xn4YwZGZULnMkaBXsvoe10JiZ-5Gnt4qvbUJXSXRHFCv6h5nRQP2TLyrabhEZf-59scu6F351RDSAZxite5CfZhqyGduD7KdgdhzTwKMK4QoI9hB6T8PAPD3ipWT0lTuM-y5husUPIYygwxVMlMXT-K2USA==Manleen KaurPas encore d'évaluation

- Bajaj Finance Limited Q2 FY15 Presentation: 14 October 2014Document33 pagesBajaj Finance Limited Q2 FY15 Presentation: 14 October 2014adi99123Pas encore d'évaluation

- Main Aims For The Central Bank of IndusDocument2 pagesMain Aims For The Central Bank of IndusKanishq BawejaPas encore d'évaluation

- RBI Notifications - December Lyst3017 PDFDocument11 pagesRBI Notifications - December Lyst3017 PDFAnkita TiwariPas encore d'évaluation

- RbiDocument44 pagesRbiRohit MalviyaPas encore d'évaluation

- RBI keeps repo rate unchanged and other banking newsDocument51 pagesRBI keeps repo rate unchanged and other banking newsunikxocizmPas encore d'évaluation

- Recent Trends in Monetary Policy of India: Submitted By: Jayant Sharma Venus BhatiaDocument18 pagesRecent Trends in Monetary Policy of India: Submitted By: Jayant Sharma Venus BhatiaJayant SharmaPas encore d'évaluation

- 2) Overview of BankingDocument48 pages2) Overview of BankingAltamashPas encore d'évaluation

- Project Report: Banking ReformsDocument9 pagesProject Report: Banking ReformsS.S.Rules100% (1)

- Assignment FinancialSectorReforms1991Document4 pagesAssignment FinancialSectorReforms1991Swathi SriPas encore d'évaluation

- Assignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryDocument9 pagesAssignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryRohit VermaPas encore d'évaluation

- Monetary Policy: Wipinson WDocument20 pagesMonetary Policy: Wipinson WWipinson WilsonPas encore d'évaluation

- Monetary Policies by Rbi in RecessionDocument21 pagesMonetary Policies by Rbi in Recessionsamruddhi_khalePas encore d'évaluation

- An Insight On The Financials of The 3 Largest Public Sector Bank in India Presented By: Group 8 Section A Mba-Jan 13Document22 pagesAn Insight On The Financials of The 3 Largest Public Sector Bank in India Presented By: Group 8 Section A Mba-Jan 13Mohit BatraPas encore d'évaluation

- Role of Financial Systems and Key ReformsDocument20 pagesRole of Financial Systems and Key ReformssumashekharPas encore d'évaluation

- Banking Sector: Presented By:-Nidhi Rachita Shweta Shubhi Priyanka SapnaDocument25 pagesBanking Sector: Presented By:-Nidhi Rachita Shweta Shubhi Priyanka Sapnamoti009Pas encore d'évaluation

- Impact of Recession On BanksDocument45 pagesImpact of Recession On BanksgiadcunhaPas encore d'évaluation

- Reserve Bank of IndiaDocument33 pagesReserve Bank of Indiaabhishek00soodPas encore d'évaluation

- Regulatory Bodies in India - RBI - 2Document38 pagesRegulatory Bodies in India - RBI - 2omesh gehlotPas encore d'évaluation

- Monetary PolicyDocument34 pagesMonetary PolicychengadPas encore d'évaluation

- State Bank of IndiaDocument30 pagesState Bank of IndiaSahil ChhibberPas encore d'évaluation

- Pre and Post Reforms in Indian Financial SystemDocument16 pagesPre and Post Reforms in Indian Financial SystemsunilPas encore d'évaluation

- Team - Finacs - Mergers & Acquisition Document in Banking IndustryDocument21 pagesTeam - Finacs - Mergers & Acquisition Document in Banking IndustryankurchorariaPas encore d'évaluation

- Credit Control in India by RbiDocument3 pagesCredit Control in India by RbiRitisha MishraPas encore d'évaluation

- Banking IndustryDocument122 pagesBanking IndustryRitesh BhansaliPas encore d'évaluation

- PESTEL Analysis of Opportunities and Challenges in the Indian Banking SectorDocument4 pagesPESTEL Analysis of Opportunities and Challenges in the Indian Banking SectorVibhav Upadhyay100% (1)

- Narasimhan CommitteeDocument10 pagesNarasimhan CommitteeAshwini VPas encore d'évaluation

- Rural Banking: Presented By: Hema SinghDocument34 pagesRural Banking: Presented By: Hema SinghRitika HiiPas encore d'évaluation

- Banking Finance and Insurance: A Report On Financial Analysis of IDBI BankDocument8 pagesBanking Finance and Insurance: A Report On Financial Analysis of IDBI BankRaven FormournePas encore d'évaluation

- State Bank of Pakistan Central Bank Role, Functions & Monetary Policy ToolsDocument25 pagesState Bank of Pakistan Central Bank Role, Functions & Monetary Policy ToolsTariq Abbasi50% (2)

- Monetar Y Policy and Role of Rbi: Submitted To-Presented byDocument40 pagesMonetar Y Policy and Role of Rbi: Submitted To-Presented byShrutiPas encore d'évaluation

- RBI's Role in Regulating Banks and Implementing Monetary PolicyDocument47 pagesRBI's Role in Regulating Banks and Implementing Monetary Policyatanu7590Pas encore d'évaluation

- Financial InclusionDocument37 pagesFinancial Inclusionparvati anilkumarPas encore d'évaluation

- Monetary PolicyDocument23 pagesMonetary PolicyManjunath ShettigarPas encore d'évaluation

- Central BankingDocument25 pagesCentral BankingRiya WilsonPas encore d'évaluation

- Pakistan Islamic Banking Bulletin Nov 2007/TITLEDocument20 pagesPakistan Islamic Banking Bulletin Nov 2007/TITLEAyeshaJangdaPas encore d'évaluation

- Reforms of Debt Market: Submitted by - Damishk Verma Ashish Patel Chetna Srivastava Indresh PratapDocument25 pagesReforms of Debt Market: Submitted by - Damishk Verma Ashish Patel Chetna Srivastava Indresh Pratapbb2Pas encore d'évaluation

- 4163IIBF Vision March 2015Document8 pages4163IIBF Vision March 2015Madhumita PandeyPas encore d'évaluation

- Internship ReportDocument159 pagesInternship ReportSufi ShahPas encore d'évaluation

- RBI's Monetary Policy Objectives and ToolsDocument6 pagesRBI's Monetary Policy Objectives and ToolspundirsandeepPas encore d'évaluation

- Advertising and Personal SellingDocument14 pagesAdvertising and Personal Sellingaryansachdeva2122002Pas encore d'évaluation

- Annual Report 2007-2008 (ENG) - 20100603063436Document89 pagesAnnual Report 2007-2008 (ENG) - 20100603063436Rakshya ShresthaPas encore d'évaluation

- Commercial Banks: Sector UpdateDocument19 pagesCommercial Banks: Sector UpdateAdeel RanaPas encore d'évaluation

- FR FemaDocument33 pagesFR FemarohanPas encore d'évaluation

- Emerging Issues in Finance Sector Inclusion, Deepening, and Development in the People's Republic of ChinaD'EverandEmerging Issues in Finance Sector Inclusion, Deepening, and Development in the People's Republic of ChinaPas encore d'évaluation

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)D'EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Pas encore d'évaluation

- My Pestel AnalysisDocument1 pageMy Pestel AnalysisClaudia CaviezelPas encore d'évaluation

- 1.1 An Overview of International Business and GlobalizationDocument52 pages1.1 An Overview of International Business and GlobalizationFadzil YahyaPas encore d'évaluation

- Interdependence and Gains From TradeDocument5 pagesInterdependence and Gains From TradeDolphPas encore d'évaluation

- Case Study #3: "Quantitative Easing in The Great Recession" (Due Date: May 5 at 6:30PM)Document4 pagesCase Study #3: "Quantitative Easing in The Great Recession" (Due Date: May 5 at 6:30PM)NarinderPas encore d'évaluation

- Meaning and Definition OverheadsDocument3 pagesMeaning and Definition OverheadskunjapPas encore d'évaluation

- XI Economics Class Notes by Ca Parag Gupta: (RKG Institute)Document92 pagesXI Economics Class Notes by Ca Parag Gupta: (RKG Institute)xenxhuPas encore d'évaluation

- Ecs1601 Assignment 1 Second Semester 2020Document7 pagesEcs1601 Assignment 1 Second Semester 2020Musa MavhuPas encore d'évaluation

- Macroeconomics Canadian 8th Edition Sayre Solutions Manual 1Document9 pagesMacroeconomics Canadian 8th Edition Sayre Solutions Manual 1tyrone100% (52)

- Business Environment Assignment - 1Document9 pagesBusiness Environment Assignment - 1Sohel AnsariPas encore d'évaluation

- Nelson, Robert, H. - Economics and ReligionDocument2 pagesNelson, Robert, H. - Economics and ReligionsyiraaufaPas encore d'évaluation

- MAM-3.... Production Possibillity Curve & Opportunity Cost - 26!8!14Document99 pagesMAM-3.... Production Possibillity Curve & Opportunity Cost - 26!8!14Vijay VaghelaPas encore d'évaluation

- CAPE Economics SyllabusDocument69 pagesCAPE Economics SyllabusDana Ali75% (4)

- RAYOVAC'S RECHARGEABLE BATTERY OPPORTUNITYDocument4 pagesRAYOVAC'S RECHARGEABLE BATTERY OPPORTUNITYmonika226Pas encore d'évaluation

- Cap 2 RoadmapDocument1 pageCap 2 RoadmapAihra Nicole DiestroPas encore d'évaluation

- AES Adjusted WACC Case StudyDocument12 pagesAES Adjusted WACC Case StudyTim Castorena33% (3)

- Porters Diamond For ZaraDocument2 pagesPorters Diamond For ZaraSunny Ramesh SadnaniPas encore d'évaluation

- Hood Emerging 1995Document19 pagesHood Emerging 1995oktayPas encore d'évaluation

- The External Environment: Mcgraw-Hill/Irwin © 2005 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument40 pagesThe External Environment: Mcgraw-Hill/Irwin © 2005 The Mcgraw-Hill Companies, Inc., All Rights ReservedTanut VatPas encore d'évaluation

- Pearson trade theory quizDocument31 pagesPearson trade theory quizHemant Deshmukh100% (2)

- I TemplateDocument8 pagesI TemplateNoel Ian SimboriosPas encore d'évaluation

- Intro. To EconomicsDocument7 pagesIntro. To EconomicsJasmine KaurPas encore d'évaluation

- Consumer Sovereignty and Axe Deodorants' Success in IndiaDocument8 pagesConsumer Sovereignty and Axe Deodorants' Success in IndiamythreyakPas encore d'évaluation

- Managerial Economics Compilation ReviewDocument121 pagesManagerial Economics Compilation ReviewMilette CaliwanPas encore d'évaluation

- Measures of Leverage: Test Code: R37 MSOL Q-BankDocument8 pagesMeasures of Leverage: Test Code: R37 MSOL Q-BankMarwa Abd-ElmeguidPas encore d'évaluation

- Economics, Taxation Land ReformDocument8 pagesEconomics, Taxation Land ReformKaren Faye TorrecampoPas encore d'évaluation

- Cost Behavior HandoutsDocument4 pagesCost Behavior Handoutsjamhel25Pas encore d'évaluation

- 13 Costs ProductionDocument54 pages13 Costs ProductionAtif RaoPas encore d'évaluation

- 898 Ch15ARQDocument2 pages898 Ch15ARQNga BuiPas encore d'évaluation

- Jnu Admission BrochureDocument102 pagesJnu Admission BrochureMota Chashma0% (1)

- Chapter 7 Market Structure: Perfect Competition: Economics For Managers, 3e (Farnham)Document25 pagesChapter 7 Market Structure: Perfect Competition: Economics For Managers, 3e (Farnham)ForappForapp100% (1)