Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Silabi3-51 Sore (14x Pertemuan)Document15 pagesSilabi3-51 Sore (14x Pertemuan)Abdul Ro'uf FarizkiPas encore d'évaluation

- Chapter Ten: Business Model AnalysisDocument57 pagesChapter Ten: Business Model AnalysisJanry SimanungkalitPas encore d'évaluation

- Common Stock ValuationDocument57 pagesCommon Stock ValuationNaeemPas encore d'évaluation

- Exam Financial Statement AnalysisDocument18 pagesExam Financial Statement AnalysisBuketPas encore d'évaluation

- Cases in Corporate GovernanceDocument177 pagesCases in Corporate GovernanceTrâm AnhPas encore d'évaluation

- Financial Reporting Quality Fair ValueDocument13 pagesFinancial Reporting Quality Fair ValueÁgnes SchwarczPas encore d'évaluation

- BCG Findings Recommendations/ Hallazgos y Recomendaciones Escuelas 12nov2014 EspanolDocument25 pagesBCG Findings Recommendations/ Hallazgos y Recomendaciones Escuelas 12nov2014 EspanolEmily RamosPas encore d'évaluation

- Acca Ifrs 13Document3 pagesAcca Ifrs 13yung kenPas encore d'évaluation

- A Contingency Framework For The Design of Accounting Information SystemDocument15 pagesA Contingency Framework For The Design of Accounting Information SystemAdeel RanaPas encore d'évaluation

- SAP Foreign Currency Valuation ProcessDocument15 pagesSAP Foreign Currency Valuation ProcessSrinivas MsrPas encore d'évaluation

- Level II - Derivatives: Pricing and Valuation of Forward CommitmentsDocument52 pagesLevel II - Derivatives: Pricing and Valuation of Forward CommitmentsDerrick NyakibaPas encore d'évaluation

- Byjus Base ModelDocument8 pagesByjus Base Modelsharma.kunal70Pas encore d'évaluation

- SAP MM SkillsDocument2 pagesSAP MM SkillsRahul100% (1)

- Inventory Masters in TallyDocument29 pagesInventory Masters in Tallyjk balooPas encore d'évaluation

- RL360° Personal Investment Management Service Key FeaturesDocument6 pagesRL360° Personal Investment Management Service Key FeaturesRL360°Pas encore d'évaluation

- In Re:) Chapter 11) Collins & Aikman Corporation, Et Al.1) Case No. 05-55927 (SWR) ) (Jointly Administered) Debtors.) ) (Tax Identification #13-3489233) ) ) Honorable Steven W. RhodesDocument35 pagesIn Re:) Chapter 11) Collins & Aikman Corporation, Et Al.1) Case No. 05-55927 (SWR) ) (Jointly Administered) Debtors.) ) (Tax Identification #13-3489233) ) ) Honorable Steven W. RhodesChapter 11 DocketsPas encore d'évaluation

- PWC Graduate Brochure 2016Document40 pagesPWC Graduate Brochure 2016vikasdstar1669Pas encore d'évaluation

- Pakistan Refinery Limited (Annual Report 2008)Document84 pagesPakistan Refinery Limited (Annual Report 2008)Monis Ali100% (1)

- Global SAP Implementation Case Study For PDFDocument28 pagesGlobal SAP Implementation Case Study For PDFSid MehtaPas encore d'évaluation

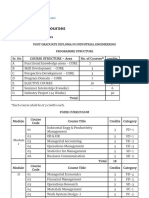

- PGDIE program structure and elective coursesDocument7 pagesPGDIE program structure and elective coursesRoshan SinghPas encore d'évaluation

- DNA GrowthDocument17 pagesDNA Growthabhishek chauhanPas encore d'évaluation

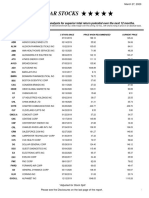

- Five Star StocksDocument5 pagesFive Star StocksJeff SturgeonPas encore d'évaluation

- Excel Workings Bedford Clinics Practice ValuationDocument6 pagesExcel Workings Bedford Clinics Practice Valuationalka murarka33% (3)

- MBA CBCS Sem I and II SyllabusDocument20 pagesMBA CBCS Sem I and II SyllabusNilesh AdhikariPas encore d'évaluation

- Prospectus 20190502 (Visa Stamped)Document60 pagesProspectus 20190502 (Visa Stamped)Georgio RomaniPas encore d'évaluation

- Syllabus PDFDocument3 pagesSyllabus PDFBenjamin ChillamPas encore d'évaluation

- Using BAdIs For Custom Valuation and Generation in XStepsDocument23 pagesUsing BAdIs For Custom Valuation and Generation in XStepsNani kPas encore d'évaluation

- Final of Load Star Balance SheetDocument96 pagesFinal of Load Star Balance SheetnikeshalaPas encore d'évaluation

- Reverse DCFDocument6 pagesReverse DCFErvin Khouw0% (1)

- Crystal Insurance IPO Note BreakdownDocument8 pagesCrystal Insurance IPO Note BreakdownAshraf Uz ZamanPas encore d'évaluation