Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- It Is in The Agricultural Sector That The Battle For Long Term Economic Development Will Be Won or LostDocument1 pageIt Is in The Agricultural Sector That The Battle For Long Term Economic Development Will Be Won or LostPranjal Gupta50% (2)

- Teaching Me Softly: A Syllabus For A Subject On Soft Skills: March 2015Document8 pagesTeaching Me Softly: A Syllabus For A Subject On Soft Skills: March 2015Charu ModiPas encore d'évaluation

- Marketing Management MCQDocument42 pagesMarketing Management MCQAbdul Rehman Chahal75% (4)

- Soft Skills For Business Success Deloitte Access Economics FINALDocument41 pagesSoft Skills For Business Success Deloitte Access Economics FINALWah Khaing100% (1)

- Time Value of MoneyDocument24 pagesTime Value of MoneyCharu Modi100% (1)

- Public Private PartnershipsDocument14 pagesPublic Private PartnershipsCharu ModiPas encore d'évaluation

- MCQ On Marketing ManagementDocument2 pagesMCQ On Marketing ManagementCharu Modi67% (3)

- E MarketingDocument13 pagesE MarketingCharu ModiPas encore d'évaluation

- Sales of Goods ActDocument56 pagesSales of Goods ActCharu ModiPas encore d'évaluation

- Faculty Development Program ScheduleDocument1 pageFaculty Development Program ScheduleCharu ModiPas encore d'évaluation

- Data Analysis and InterpretationDocument12 pagesData Analysis and InterpretationCharu ModiPas encore d'évaluation

- Derivatives As Risk Management Tool For CorporatesDocument86 pagesDerivatives As Risk Management Tool For CorporatesCharu ModiPas encore d'évaluation

- MAMDocument13 pagesMAMCharu ModiPas encore d'évaluation

- Subjects: Entrepreneurship Development Business EnvironmentDocument11 pagesSubjects: Entrepreneurship Development Business EnvironmentCharu ModiPas encore d'évaluation

- Mock Test Marketing Officer 29 Feb, 2012 Explanations Quantitative Aptitude (51-55) : Posts Post Post Post Post Com. I II III IVDocument9 pagesMock Test Marketing Officer 29 Feb, 2012 Explanations Quantitative Aptitude (51-55) : Posts Post Post Post Post Com. I II III IVCharu ModiPas encore d'évaluation

- Model Curriculum PGDM 060912Document154 pagesModel Curriculum PGDM 060912Charu ModiPas encore d'évaluation

- Syllabus@PGDM 1st YearDocument84 pagesSyllabus@PGDM 1st Yearmail_garaiPas encore d'évaluation

- Risk ManagementDocument27 pagesRisk ManagementCharu Modi100% (1)

- 5 IIM Graduates Who Quit Job To Become EntrepreneursDocument19 pages5 IIM Graduates Who Quit Job To Become EntrepreneursCharu ModiPas encore d'évaluation

- Fodder ScamDocument3 pagesFodder ScamCharu ModiPas encore d'évaluation

- Daftar PustakaDocument4 pagesDaftar PustakaIvana HalingkarPas encore d'évaluation

- Organic Forest Coffee in ThailandDocument7 pagesOrganic Forest Coffee in ThailandTheerasitPas encore d'évaluation

- Hairy Small-Leaf Ticktrefoil: Desmodium Ciliare (Muhl. Ex Willd.) DC. - Plant Fact Sheet - Plant Materials Center, Beltsville, MDDocument2 pagesHairy Small-Leaf Ticktrefoil: Desmodium Ciliare (Muhl. Ex Willd.) DC. - Plant Fact Sheet - Plant Materials Center, Beltsville, MDMaryland Native Plant ResourcesPas encore d'évaluation

- Project Report On Ngo in Koraput District in OdishaDocument39 pagesProject Report On Ngo in Koraput District in OdishaSambeet ParidaPas encore d'évaluation

- DanielZoharyMariaHopf 2012 DomesticationOfPlantsDocument263 pagesDanielZoharyMariaHopf 2012 DomesticationOfPlantsFrancisco Gil MuñozPas encore d'évaluation

- Za Ss 32 Farming in South Africa Map Work Caps Geography Ver 6Document5 pagesZa Ss 32 Farming in South Africa Map Work Caps Geography Ver 6OnkgopotsePas encore d'évaluation

- POTS Philippines Palm Oil Industry Road MapDocument38 pagesPOTS Philippines Palm Oil Industry Road MapfaridsidikPas encore d'évaluation

- HB 374 - Genuine Agrarian Reform BillDocument25 pagesHB 374 - Genuine Agrarian Reform BillanakpawispartylistPas encore d'évaluation

- Sustainable Agriculture - The Israeli Experience: Raanan KatzirDocument9 pagesSustainable Agriculture - The Israeli Experience: Raanan KatzirDarvvin NediaPas encore d'évaluation

- Lesson 4Document6 pagesLesson 4simmona2101Pas encore d'évaluation

- Dictionary of Agricultural Engineering 2006 EditionDocument361 pagesDictionary of Agricultural Engineering 2006 Editionvhon100% (5)

- NJ Pesticide License Training Courses For Pesticide Applicator RecertificationDocument2 pagesNJ Pesticide License Training Courses For Pesticide Applicator RecertificationRutgersCPEPas encore d'évaluation

- Chaturvedi 2015Document7 pagesChaturvedi 2015Abhishek KhobragadePas encore d'évaluation

- Chapter 101Document20 pagesChapter 101Harsha VardhanPas encore d'évaluation

- Khazana Bawali Historical Wisdom Needing Protection: Narendra ChapalgaonkarDocument5 pagesKhazana Bawali Historical Wisdom Needing Protection: Narendra ChapalgaonkarAbdul KaziPas encore d'évaluation

- Exotic PlantsDocument164 pagesExotic PlantsKenneth100% (9)

- 100% Chemical-Free Solution For Organic Farming: Where Health Is A HabitDocument2 pages100% Chemical-Free Solution For Organic Farming: Where Health Is A Habitamit4118Pas encore d'évaluation

- Conference Proceedings N Fs 1Document404 pagesConference Proceedings N Fs 1erekhajicahsheibesayonPas encore d'évaluation

- LEHNER SuperVario Brochure Engl 3 2023Document4 pagesLEHNER SuperVario Brochure Engl 3 2023Jefferson MagalhaesPas encore d'évaluation

- Vechur CowDocument3 pagesVechur CowAditya KumarPas encore d'évaluation

- Overview of Drip Irrigation: Potential, Issues and ConstraintsDocument24 pagesOverview of Drip Irrigation: Potential, Issues and ConstraintsEngr Muhammad Asif JavaidPas encore d'évaluation

- JH Ankron Vs Government of The Phil Islands CASE DIGESTsDocument2 pagesJH Ankron Vs Government of The Phil Islands CASE DIGESTsVertine Paul Fernandez Beler0% (1)

- FOREST ECOLOGY-presentationDocument13 pagesFOREST ECOLOGY-presentationAndjela Nastic100% (1)

- Lecture 6Document6 pagesLecture 6Esther Suan-LancitaPas encore d'évaluation

- FertilizerDocument220 pagesFertilizerManish Kumar ChoudharyPas encore d'évaluation

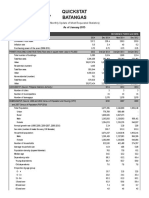

- Quickstat Batangas: (Monthly Update of Most Requested Statistics)Document5 pagesQuickstat Batangas: (Monthly Update of Most Requested Statistics)Martin Owen CallejaPas encore d'évaluation

- Spring 2022 MagazineDocument20 pagesSpring 2022 MagazineOrganicAlberta100% (1)

- GMOs Good and Bad-1Document9 pagesGMOs Good and Bad-1Jordan GriffinPas encore d'évaluation

- Botany of DMTDocument4 pagesBotany of DMTKeirra-lee Clark100% (1)