Vous aimerez peut-être aussi

- Swot Analysis of StarbucksDocument17 pagesSwot Analysis of StarbucksLUJING SUN0% (1)

- Capital Structure TheoryDocument8 pagesCapital Structure TheoryAnna MahmudPas encore d'évaluation

- 1 Value Chain Analysis - SMIDocument10 pages1 Value Chain Analysis - SMIToto SubagyoPas encore d'évaluation

- Harmonizing Accounting Differences Across The CountriesDocument22 pagesHarmonizing Accounting Differences Across The Countriesankzzy100% (1)

- Strategy Formulation and Implementation OutlineDocument4 pagesStrategy Formulation and Implementation OutlineMariell Joy Cariño-TanPas encore d'évaluation

- Week 7 & 8 - Illegality and Public PolicyDocument58 pagesWeek 7 & 8 - Illegality and Public PolicyMaame BaidooPas encore d'évaluation

- Modes of International Market EntryDocument45 pagesModes of International Market EntryNeelam KamblePas encore d'évaluation

- STRATEGIC ALLIANCE BENEFITSDocument32 pagesSTRATEGIC ALLIANCE BENEFITSZoya Khan100% (1)

- Theories of International Trade and Implications For EIBDocument35 pagesTheories of International Trade and Implications For EIBSama KurimPas encore d'évaluation

- Cost Concepts & Its AnalysisDocument19 pagesCost Concepts & Its AnalysisKenen Bhandhavi100% (1)

- DiversificationDocument56 pagesDiversificationvarsha27k4586Pas encore d'évaluation

- Chapter 06 Lecture NotesDocument16 pagesChapter 06 Lecture NotesMega Pop LockerPas encore d'évaluation

- Ethics in Negotiation-1Document24 pagesEthics in Negotiation-1Farid AhmedPas encore d'évaluation

- Chap6: International Trade TheoriesDocument40 pagesChap6: International Trade TheoriesJoydeb Kumar SahaPas encore d'évaluation

- SM 8 - Strategy EvaluationDocument26 pagesSM 8 - Strategy EvaluationAmit Sethi100% (1)

- Business Policy & Strategic ManagementDocument9 pagesBusiness Policy & Strategic ManagementSåntøsh YådåvPas encore d'évaluation

- Strategic MGMT ch08Document25 pagesStrategic MGMT ch08farazalam08100% (5)

- Daniels11 - The Strategy of International BusinessDocument28 pagesDaniels11 - The Strategy of International BusinessHuman Resource ManagementPas encore d'évaluation

- Daniels14 - Direct Investment and Collaborative StrategiesDocument27 pagesDaniels14 - Direct Investment and Collaborative StrategiesHuman Resource ManagementPas encore d'évaluation

- Pricing For International MarketingDocument44 pagesPricing For International Marketingjuggy1812Pas encore d'évaluation

- Brand ExtensionsDocument24 pagesBrand ExtensionsBikash KalitaPas encore d'évaluation

- Vertical and Horizontal IntegrationDocument15 pagesVertical and Horizontal IntegrationVimala Dharmasivam100% (2)

- Analyzing the External EnvironmentDocument26 pagesAnalyzing the External EnvironmentVijay D Ace100% (1)

- Service Marketing QuestionsDocument10 pagesService Marketing Questionskondwani B J MandaPas encore d'évaluation

- IBM - Unit - VDocument27 pagesIBM - Unit - VYuvaraj d100% (1)

- Strategic ManagementDocument4 pagesStrategic ManagementA CPas encore d'évaluation

- Developing A Sustainable Competitive AdvantageDocument32 pagesDeveloping A Sustainable Competitive AdvantageNeshaTinkzPas encore d'évaluation

- Analyzing Costs, Profits, and Risks for Business PlanningDocument28 pagesAnalyzing Costs, Profits, and Risks for Business Planningmanas_samantaray28Pas encore d'évaluation

- Principled Negotiation and The Negotiator's DilemmaDocument9 pagesPrincipled Negotiation and The Negotiator's DilemmaAlberto Peixoto NetoPas encore d'évaluation

- Mid Term Exam - International MKTDocument3 pagesMid Term Exam - International MKTThanh Hang100% (1)

- Strategic Management: Concepts and CasesDocument23 pagesStrategic Management: Concepts and CasesRushabh VoraPas encore d'évaluation

- Strategic AlliancesDocument19 pagesStrategic Alliancesmonam100% (1)

- The Strategy of International BusinessDocument5 pagesThe Strategy of International BusinessSania MaQsOoDPas encore d'évaluation

- Top Most Important Questions & Answers For Strategic ManagementDocument28 pagesTop Most Important Questions & Answers For Strategic ManagementAnonymous iIONVEmz100% (1)

- Income and Substitution Effects of A Wage ChangeDocument24 pagesIncome and Substitution Effects of A Wage ChangemanashchoudhuryPas encore d'évaluation

- Perfect CompetitionDocument30 pagesPerfect CompetitionBhavesh BajajPas encore d'évaluation

- R21 Currency Exchange Rates PDFDocument34 pagesR21 Currency Exchange Rates PDFAbhijeet PatilPas encore d'évaluation

- Chapter-13 Evaluation of Countries For Operations: Presented By: Raju ShresthaDocument35 pagesChapter-13 Evaluation of Countries For Operations: Presented By: Raju Shresthaajambar khatriPas encore d'évaluation

- International Marketing EnvironmentDocument29 pagesInternational Marketing EnvironmentsujeetleopardPas encore d'évaluation

- Pricing DecisionDocument3 pagesPricing DecisionRohit RastogiPas encore d'évaluation

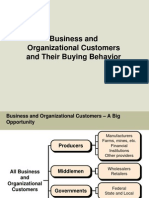

- Business and Organizational Customers and Their Buying BehaviorDocument16 pagesBusiness and Organizational Customers and Their Buying BehaviorFinola FernandesPas encore d'évaluation

- Perfect CompetitionDocument3 pagesPerfect CompetitionShreejit MenonPas encore d'évaluation

- Different Levels of StrategyDocument12 pagesDifferent Levels of StrategyELMUNTHIR BEN AMMARPas encore d'évaluation

- The Power Matrix of Supplier-Buyer RelationshipDocument32 pagesThe Power Matrix of Supplier-Buyer Relationshipselas_381983Pas encore d'évaluation

- Competitive AdvantageDocument16 pagesCompetitive AdvantageakashPas encore d'évaluation

- 3 - The Core Competence of The CorporationDocument17 pages3 - The Core Competence of The Corporationshivam1992Pas encore d'évaluation

- Pepsi and Coke Financial ManagementDocument11 pagesPepsi and Coke Financial ManagementNazish Sohail100% (1)

- International Marketing Research NotesDocument5 pagesInternational Marketing Research NotesKiranUmaraniPas encore d'évaluation

- Vogel's Approximation Method ProjectDocument9 pagesVogel's Approximation Method ProjectAkash Gupta100% (1)

- S10-ME - Nature of The IndustryDocument8 pagesS10-ME - Nature of The IndustryFun Toosh345Pas encore d'évaluation

- Chap 006Document38 pagesChap 006falcore316Pas encore d'évaluation

- Strategic Management - OverviewDocument16 pagesStrategic Management - OverviewdionisiusPas encore d'évaluation

- Demand Forecasting Using QualitativeDocument2 pagesDemand Forecasting Using QualitativeSri Krishna KuttipaiyaPas encore d'évaluation

- Meaning of Transfer PricingDocument2 pagesMeaning of Transfer Pricingpanda_alekh100% (1)

- Sourcing Materials and ServicesDocument31 pagesSourcing Materials and ServicesAndrea TaganginPas encore d'évaluation

- Purchase System & AuditDocument26 pagesPurchase System & Auditzakria100100Pas encore d'évaluation

- Price Discrimination Notes: 1 PreliminariesDocument12 pagesPrice Discrimination Notes: 1 Preliminarieserdoo17Pas encore d'évaluation

- Organizational Analysis & ProcessesDocument34 pagesOrganizational Analysis & ProcessesSreenath100% (1)

- TRANSACTION COST THEORY EXPLAINED /TITLEDocument25 pagesTRANSACTION COST THEORY EXPLAINED /TITLEANJUPOONIAPas encore d'évaluation

- Chapter 3 PDFDocument39 pagesChapter 3 PDFQuality OfficePas encore d'évaluation

- Emerging Trends in AdvertisingDocument15 pagesEmerging Trends in AdvertisingSiddharth JainPas encore d'évaluation

- Cliches: A Cliche Is An Expression or Idea or Action That Has Become Trite With OveruseDocument5 pagesCliches: A Cliche Is An Expression or Idea or Action That Has Become Trite With OveruseRahul SrivastavaPas encore d'évaluation

- Jargons For Business CommunicationDocument6 pagesJargons For Business CommunicationSiddharth JainPas encore d'évaluation

- Edward T. Hall's Theories on Cultural Context, Time and SpaceDocument18 pagesEdward T. Hall's Theories on Cultural Context, Time and SpaceSiddharth JainPas encore d'évaluation

- Business Environment - An AnalysisDocument30 pagesBusiness Environment - An AnalysisTannawy SinhaPas encore d'évaluation

- Kinky Demand Curve ModelDocument11 pagesKinky Demand Curve ModelSiddharth JainPas encore d'évaluation

- MaseeiDocument6 pagesMaseeiSiddharth JainPas encore d'évaluation

- Amitybusinessschool: Guidelines FOR DissertationDocument18 pagesAmitybusinessschool: Guidelines FOR Dissertation8130089011Pas encore d'évaluation

- Dominant Characteristics: Questionnaire Divide 100 Points Among Each of Four AlternativesDocument2 pagesDominant Characteristics: Questionnaire Divide 100 Points Among Each of Four AlternativesSiddharth JainPas encore d'évaluation

- MASSEI Assignment 1Document6 pagesMASSEI Assignment 1Siddharth JainPas encore d'évaluation

- Organisational EffectivenessDocument2 pagesOrganisational EffectivenessSiddharth JainPas encore d'évaluation

- MR QuestionnaireDocument2 pagesMR QuestionnaireSiddharth JainPas encore d'évaluation

- Work Culture Questionnaire: Questions Dominant CharacteristicsDocument2 pagesWork Culture Questionnaire: Questions Dominant CharacteristicsSiddharth JainPas encore d'évaluation

- Dominant Characteristics: Questionnaire Divide 100 Points Among Each of Four AlternativesDocument2 pagesDominant Characteristics: Questionnaire Divide 100 Points Among Each of Four AlternativesSiddharth JainPas encore d'évaluation

- MR QuestionnaireDocument2 pagesMR QuestionnaireSiddharth JainPas encore d'évaluation

- Presentation 1Document2 pagesPresentation 1Siddharth JainPas encore d'évaluation

- RTIDocument17 pagesRTISiddharth JainPas encore d'évaluation

- Cat Her inDocument38 pagesCat Her inSiddharth JainPas encore d'évaluation

- 5f47acaf AssignmentDocument1 page5f47acaf AssignmentSiddharth JainPas encore d'évaluation

- Beulah Hill Treasure Trove 1953: Edward I-III, 138 Coins, C. 1364 / (R.H.M. Dolley)Document10 pagesBeulah Hill Treasure Trove 1953: Edward I-III, 138 Coins, C. 1364 / (R.H.M. Dolley)Digital Library Numis (DLN)Pas encore d'évaluation

- Due Diligence ChecklistDocument12 pagesDue Diligence ChecklistNigel A.L. Brooks100% (1)

- Asset-Liability Management in BanksDocument42 pagesAsset-Liability Management in Banksnike_4008a100% (1)

- International Financial Markets FinalDocument46 pagesInternational Financial Markets Finalprashantgorule100% (1)

- Mcdonald'S - Case Study (Global Business Finance Cia-3) : Sakshi Arora 1520457 5Bba-DDocument3 pagesMcdonald'S - Case Study (Global Business Finance Cia-3) : Sakshi Arora 1520457 5Bba-DMadhav Luthra0% (1)

- Estratto Codice Civile Tradotto in IngleseDocument38 pagesEstratto Codice Civile Tradotto in IngleseSonia GalliPas encore d'évaluation

- TPG 2021 Annual ReportDocument1 175 pagesTPG 2021 Annual Report魏xxxapplePas encore d'évaluation

- Topic 18-22 - Investments and Basic Derivatives (Compiled)Document37 pagesTopic 18-22 - Investments and Basic Derivatives (Compiled)Eki OmallaoPas encore d'évaluation

- Hongkong DisneyDocument22 pagesHongkong DisneyLiam LêPas encore d'évaluation

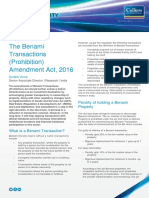

- The Benami Transactions (Prohibition) Amendment Act, 2016: India - PropertyDocument2 pagesThe Benami Transactions (Prohibition) Amendment Act, 2016: India - Propertysubhash parasharPas encore d'évaluation

- Extended Essay - Bm-FinalDocument26 pagesExtended Essay - Bm-Finalapi-581044291Pas encore d'évaluation

- Luxurious Apartment Year-End Trial Balance 2017Document2 pagesLuxurious Apartment Year-End Trial Balance 2017hehePas encore d'évaluation

- Ey Cost of Capital India Survey 2017Document16 pagesEy Cost of Capital India Survey 2017Rahul KmrPas encore d'évaluation

- 7-12. (Byron, Inc.)Document2 pages7-12. (Byron, Inc.)Gray JavierPas encore d'évaluation

- Problems - Investment in Equity SecuritiesDocument10 pagesProblems - Investment in Equity SecuritiesPrince Calica100% (1)

- History of The RenimbiDocument3 pagesHistory of The Renimbikorum8urraPas encore d'évaluation

- BBAGroup8DocumentAnalyzesSugarBowlTransformationDocument22 pagesBBAGroup8DocumentAnalyzesSugarBowlTransformationRafay KhanPas encore d'évaluation

- Eicher Motors: PrintDocument3 pagesEicher Motors: PrintAryan BagdekarPas encore d'évaluation

- Internal ReconstructionDocument8 pagesInternal Reconstructionsmit9993Pas encore d'évaluation

- PDocument21 pagesPjordenPas encore d'évaluation

- JT Seisme 2012 J2 2 Conception Parasismique Ponts 1 Analyses V3Document6 pagesJT Seisme 2012 J2 2 Conception Parasismique Ponts 1 Analyses V3Zn TkPas encore d'évaluation

- Capital Market Instruments and Types in 40 CharactersDocument5 pagesCapital Market Instruments and Types in 40 CharactersMuhammad AbdullahPas encore d'évaluation

- PLMC Investor Presentation September 17 2014 - v001 - l8949n PDFDocument22 pagesPLMC Investor Presentation September 17 2014 - v001 - l8949n PDFguanatosPas encore d'évaluation

- Baird Staffing Research - March 2012.Document65 pagesBaird Staffing Research - March 2012.cojones321Pas encore d'évaluation

- Tutorial 9 & 10-Qs-2Document2 pagesTutorial 9 & 10-Qs-2YunesshwaaryPas encore d'évaluation

- Financing Savings (In Euro) 261.86 313.88 370.20 431.10 Financing Savings (In R$) 1,099.79 1,318.30 1,554.85 1,810.63Document4 pagesFinancing Savings (In Euro) 261.86 313.88 370.20 431.10 Financing Savings (In R$) 1,099.79 1,318.30 1,554.85 1,810.63Andrea AlvaradoPas encore d'évaluation

- Research Methodology - Worksheet PDFDocument3 pagesResearch Methodology - Worksheet PDFDenisa NedelcuPas encore d'évaluation

- Ciq Financials Methodology PDFDocument25 pagesCiq Financials Methodology PDFbhaskar2400Pas encore d'évaluation

- BNP ParibasDocument10 pagesBNP ParibasSUSUWALAPas encore d'évaluation

- AssignmentDocument7 pagesAssignmentDikshita JainPas encore d'évaluation