Vous aimerez peut-être aussi

- DIS10.1 Ethical Hacking and CountermeasuresDocument14 pagesDIS10.1 Ethical Hacking and CountermeasuresJaspal Singh RanaPas encore d'évaluation

- AutoCAD Exercises (Free Ebook) - Tutorial45Document11 pagesAutoCAD Exercises (Free Ebook) - Tutorial45Kursistat PejePas encore d'évaluation

- The Impact of Digitalisation On Indian Banking SectorDocument5 pagesThe Impact of Digitalisation On Indian Banking SectorEditor IJTSRDPas encore d'évaluation

- Technologies in Banking SectorDocument43 pagesTechnologies in Banking SectorDhaval Majithia100% (3)

- Best Practices For Tomcat SecurityDocument12 pagesBest Practices For Tomcat SecurityAmit AroraPas encore d'évaluation

- Lean and Green Banking in India 2012Document20 pagesLean and Green Banking in India 2012Prof Dr Chowdari Prasad100% (2)

- ElectricCalcs R30Document21 pagesElectricCalcs R30DSAMJ23Pas encore d'évaluation

- HR As A Strategic Business PartnerDocument36 pagesHR As A Strategic Business PartnerProf Dr Chowdari PrasadPas encore d'évaluation

- Disruptive TechnologyDocument15 pagesDisruptive TechnologybinalamitPas encore d'évaluation

- Ansys Mesh IntroductionDocument27 pagesAnsys Mesh IntroductionmustafaleedsPas encore d'évaluation

- CPP Notes - Object Oriented Programming Using CPPDocument22 pagesCPP Notes - Object Oriented Programming Using CPPKunal S KasarPas encore d'évaluation

- Digital Banking in India 2016Document21 pagesDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- Digital Banking in India 2016Document21 pagesDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- Prof Chowdari Prasad CV 26112018Document11 pagesProf Chowdari Prasad CV 26112018Prof Dr Chowdari PrasadPas encore d'évaluation

- Computer Systems Servicing NC II CGDocument238 pagesComputer Systems Servicing NC II CGRickyJeciel100% (2)

- S 1 - Overview of The Fintech IndustryDocument29 pagesS 1 - Overview of The Fintech IndustryPPPas encore d'évaluation

- Digitalization in Banking SectorDocument7 pagesDigitalization in Banking SectorEditor IJTSRDPas encore d'évaluation

- Online BankingDocument39 pagesOnline Bankingsumit sharma100% (1)

- ROLE OF IT IN ENHANCING BANKING SERVICES Marketing Research Sharda 2016Document43 pagesROLE OF IT IN ENHANCING BANKING SERVICES Marketing Research Sharda 2016paras pantPas encore d'évaluation

- Digital Literacy For Banks With ItDocument5 pagesDigital Literacy For Banks With ItHemanth Kumar KoppulaPas encore d'évaluation

- E-Banking in India - Problems and Prospects: ISSN (PRINT) : 2393-8374, (ONLINE) : 2394-0697, VOLUME-5, ISSUE-1, 2018Document5 pagesE-Banking in India - Problems and Prospects: ISSN (PRINT) : 2393-8374, (ONLINE) : 2394-0697, VOLUME-5, ISSUE-1, 2018Ankit JainPas encore d'évaluation

- Impact of Technology On The Service SectorDocument27 pagesImpact of Technology On The Service SectorRahul Bakshi60% (5)

- A Study On Digital Banking System and MeDocument6 pagesA Study On Digital Banking System and MepranalirandilPas encore d'évaluation

- Venki ArticleDocument4 pagesVenki Articleramyasiva20002311Pas encore d'évaluation

- The Role of Financial Institution Facilities in Ensuring Customer Contentment in Commercial Banking Institutions in Bamenda-CameroonDocument10 pagesThe Role of Financial Institution Facilities in Ensuring Customer Contentment in Commercial Banking Institutions in Bamenda-CameroonInternational Journal of Innovative Science and Research TechnologyPas encore d'évaluation

- BBA, LL.B. First Semester-October 2021 Research Paper TopicDocument11 pagesBBA, LL.B. First Semester-October 2021 Research Paper TopicSPARSH SHARMAPas encore d'évaluation

- Final Report 1Document9 pagesFinal Report 1deadlygamer6996Pas encore d'évaluation

- Technological Innovations in Indian Banking Sector: Aruna R. ShetDocument4 pagesTechnological Innovations in Indian Banking Sector: Aruna R. ShetNikhil patilPas encore d'évaluation

- Technological Innovations in Indian Banking Sector: Aruna R. ShetDocument4 pagesTechnological Innovations in Indian Banking Sector: Aruna R. ShetNikhil patilPas encore d'évaluation

- Role of Information Technology in Indian Banking SectorDocument5 pagesRole of Information Technology in Indian Banking SectorIOSRjournal100% (1)

- 20Q91A6634 SnehithaDocument11 pages20Q91A6634 SnehithaachugatlasindhuPas encore d'évaluation

- Role of Information Technology in Indian Banking Sector: Dr.G.Tulasi Rao, T.Lokeswara RaoDocument5 pagesRole of Information Technology in Indian Banking Sector: Dr.G.Tulasi Rao, T.Lokeswara RaoNikhil patilPas encore d'évaluation

- MIS PresentationDocument14 pagesMIS Presentationgebarap913Pas encore d'évaluation

- Internet Banking Hurdles and SolutionsDocument18 pagesInternet Banking Hurdles and SolutionsProf Dr Chowdari Prasad100% (2)

- BRM PROJECT FinalDocument19 pagesBRM PROJECT FinalrastehertaPas encore d'évaluation

- Impact of Internet On Banking SectorDocument13 pagesImpact of Internet On Banking SectorInamul HaquePas encore d'évaluation

- Innovation in Indian Banking Sector UseDocument14 pagesInnovation in Indian Banking Sector UseKamran YousafPas encore d'évaluation

- 362-Article Text-835-1-10-20221116Document18 pages362-Article Text-835-1-10-20221116Bagmee SampannaPas encore d'évaluation

- Final Report 1Document9 pagesFinal Report 1deadlygamer6996Pas encore d'évaluation

- BFSI Transformation Leaders Conclave 2024, Mumbai Sahara StarDocument3 pagesBFSI Transformation Leaders Conclave 2024, Mumbai Sahara Starkapil_jPas encore d'évaluation

- 185-192 Rrijm20230803022Document8 pages185-192 Rrijm20230803022JakePas encore d'évaluation

- A Study On Significance of Digitization in Banking ServicesDocument4 pagesA Study On Significance of Digitization in Banking ServicesInternational Journal of Application or Innovation in Engineering & ManagementPas encore d'évaluation

- Article JyotiranjanHota April12Document3 pagesArticle JyotiranjanHota April12Lipsa MohapatraPas encore d'évaluation

- The Impact of Digitalisation On Indian Banking Sector: October 2018Document6 pagesThe Impact of Digitalisation On Indian Banking Sector: October 2018Altaf ShaikhPas encore d'évaluation

- Role of It in Banking Sector PDFDocument4 pagesRole of It in Banking Sector PDFVEERADHI GOMATHI RANIPas encore d'évaluation

- Review of Literature 1Document4 pagesReview of Literature 1revahykrish93Pas encore d'évaluation

- Customer Awareness On Technology Products of Karur Vysya BankDocument7 pagesCustomer Awareness On Technology Products of Karur Vysya BankAnonymous fLcXtRxSPas encore d'évaluation

- Impact of Technology On Banking Sector in India: International Journal of Scientific Research June 2012Document5 pagesImpact of Technology On Banking Sector in India: International Journal of Scientific Research June 2012Shubham RajPas encore d'évaluation

- Finaacial Innovative and Creativity in Banking Sector.Document5 pagesFinaacial Innovative and Creativity in Banking Sector.SakshiPas encore d'évaluation

- (20687249 - Review of Economic and Business Studies) Application of Artificial Intelligence in Investment BanksDocument6 pages(20687249 - Review of Economic and Business Studies) Application of Artificial Intelligence in Investment BankssamarPas encore d'évaluation

- Payment Through FintechDocument4 pagesPayment Through FintechShubham sharmaPas encore d'évaluation

- Group 5: Digital Business TransformationDocument12 pagesGroup 5: Digital Business TransformationArunima SinghPas encore d'évaluation

- E-Banking: Panchyat Degree College, BargarhDocument49 pagesE-Banking: Panchyat Degree College, BargarhKunjabana DantaPas encore d'évaluation

- Role of Banking in ItDocument53 pagesRole of Banking in Itajaydas2k4Pas encore d'évaluation

- Technology & BankingDocument15 pagesTechnology & Bankingswati100491% (11)

- Banking Technology and Service Quality: Evidence From Private Sector Banks in KeralaDocument6 pagesBanking Technology and Service Quality: Evidence From Private Sector Banks in KeralaVaibhav DafalePas encore d'évaluation

- Problem Statements NFC2.0Document13 pagesProblem Statements NFC2.0VimanPas encore d'évaluation

- Digital Transformation in India - S Banking SectorDocument4 pagesDigital Transformation in India - S Banking SectorT ForsythPas encore d'évaluation

- Caeden Banking CorporationDocument5 pagesCaeden Banking CorporationLilibeth OrongPas encore d'évaluation

- Digitalization in Banking SectorDocument3 pagesDigitalization in Banking SectorEditor IJTSRDPas encore d'évaluation

- New Technological Innovations in The Banking SectorDocument5 pagesNew Technological Innovations in The Banking SectorlapogkPas encore d'évaluation

- E Generation of Banking in IndiaDocument2 pagesE Generation of Banking in IndiaSharath Srinivas BuduguntePas encore d'évaluation

- Building Profitable Customer Relationships With CRM & E-Governance in BanksDocument12 pagesBuilding Profitable Customer Relationships With CRM & E-Governance in BanksJeya StalinPas encore d'évaluation

- Awareness and Adoption of Technology in Banking Especially by Rural Areas Customers: A Study of Udaipur Rural BeltDocument14 pagesAwareness and Adoption of Technology in Banking Especially by Rural Areas Customers: A Study of Udaipur Rural BeltnofaPas encore d'évaluation

- Computer Tarm PaperDocument5 pagesComputer Tarm PaperMd Hasibur RahmanPas encore d'évaluation

- Minor Research Project VaradDocument10 pagesMinor Research Project Varadabhinandan sharmaPas encore d'évaluation

- Publications - 2016 - Fa - IB CRM Fahad - 33401-36346-1-PB - 2 PDFDocument13 pagesPublications - 2016 - Fa - IB CRM Fahad - 33401-36346-1-PB - 2 PDFFahadPas encore d'évaluation

- Paper 21-The Impacts of ICTs On BanksDocument6 pagesPaper 21-The Impacts of ICTs On BanksMayorPas encore d'évaluation

- Analysis and Design of Next-Generation Software Architectures: 5G, IoT, Blockchain, and Quantum ComputingD'EverandAnalysis and Design of Next-Generation Software Architectures: 5G, IoT, Blockchain, and Quantum ComputingPas encore d'évaluation

- Second Innings September 2019Document52 pagesSecond Innings September 2019Prof Dr Chowdari PrasadPas encore d'évaluation

- 10 International Conference On Problem and Possibilities in Online Education in ManagementDocument39 pages10 International Conference On Problem and Possibilities in Online Education in ManagementProf Dr Chowdari PrasadPas encore d'évaluation

- A Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsDocument15 pagesA Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsProf Dr Chowdari PrasadPas encore d'évaluation

- Social Entrepreneurship2015Document45 pagesSocial Entrepreneurship2015Prof Dr Chowdari PrasadPas encore d'évaluation

- Performance of Crowd Funding in India: Issues and ChallengesDocument19 pagesPerformance of Crowd Funding in India: Issues and ChallengesProf Dr Chowdari Prasad100% (1)

- Consumer Protection Act 1986Document41 pagesConsumer Protection Act 1986Prof Dr Chowdari Prasad100% (1)

- Tapmi Update 2013Document120 pagesTapmi Update 2013Prof Dr Chowdari PrasadPas encore d'évaluation

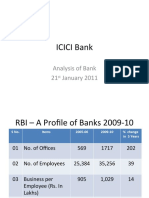

- Icici Bank: Analysis of Bank 21 January 2011Document6 pagesIcici Bank: Analysis of Bank 21 January 2011Prof Dr Chowdari PrasadPas encore d'évaluation

- List of Books On Micro FinanceDocument32 pagesList of Books On Micro FinanceProf Dr Chowdari Prasad71% (7)

- Recent Trends of PE Funding in IndiaDocument38 pagesRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadPas encore d'évaluation

- Myths of Microfinance - Global South Development Magazine JAN 2011Document42 pagesMyths of Microfinance - Global South Development Magazine JAN 2011Silver Lining CreationPas encore d'évaluation

- Women Achievers Ebook2Document95 pagesWomen Achievers Ebook2Prof Dr Chowdari PrasadPas encore d'évaluation

- Profile of Banks 2010-11Document99 pagesProfile of Banks 2010-11Vishesh KumarPas encore d'évaluation

- The Development Perspective of Finance and Microfinance Sector in China: How Far Is Microfinance Regulations?Document11 pagesThe Development Perspective of Finance and Microfinance Sector in China: How Far Is Microfinance Regulations?Prof Dr Chowdari PrasadPas encore d'évaluation

- MFI National ConferenceDocument12 pagesMFI National ConferenceProf Dr Chowdari PrasadPas encore d'évaluation

- Sibm, RBCBDocument20 pagesSibm, RBCBProf Dr Chowdari PrasadPas encore d'évaluation

- Syndicate Institute of Bank Management, ManipalDocument67 pagesSyndicate Institute of Bank Management, ManipalProf Dr Chowdari PrasadPas encore d'évaluation

- TAPMI ManipalDocument18 pagesTAPMI ManipalProf Dr Chowdari Prasad100% (1)

- HWM ReadmeDocument3 pagesHWM ReadmeFabian VargasPas encore d'évaluation

- Barangay Service Management SystemDocument5 pagesBarangay Service Management SystemJohn Paulo AragonesPas encore d'évaluation

- HDL Description of AluDocument8 pagesHDL Description of AluRavi HattiPas encore d'évaluation

- 01 Intelligent Systems-IntroductionDocument82 pages01 Intelligent Systems-Introduction1balamanianPas encore d'évaluation

- Mark MorrisseyDocument43 pagesMark MorrisseyKara SwisherPas encore d'évaluation

- Award BIOS Beep CodesDocument2 pagesAward BIOS Beep CodesdanielsernaPas encore d'évaluation

- IOS Application Security Part 4 - Runtime Analysis Using Cycript (Yahoo Weather App)Document11 pagesIOS Application Security Part 4 - Runtime Analysis Using Cycript (Yahoo Weather App)MelodySongPas encore d'évaluation

- Komal Devi CVDocument8 pagesKomal Devi CVMuhammed Amjad IslamPas encore d'évaluation

- EafrDocument8 pagesEafrNour El-Din SafwatPas encore d'évaluation

- RFIDTaiwan Experience PDFDocument10 pagesRFIDTaiwan Experience PDFCibyBaby PunnamparambilPas encore d'évaluation

- Autocad Part 1Document1 000 pagesAutocad Part 1Anonymous 9qKdViDP4Pas encore d'évaluation

- Solix Enterprise ArchivingDocument2 pagesSolix Enterprise ArchivingLinda WatsonPas encore d'évaluation

- Skills For Employment Investment Project (SEIP) : Standards/ Curriculum Format For Graphics DesignDocument10 pagesSkills For Employment Investment Project (SEIP) : Standards/ Curriculum Format For Graphics DesignSun SetPas encore d'évaluation

- UsingDocument28 pagesUsingCristo_Alanis_8381Pas encore d'évaluation

- Project G2 EightPuzzleDocument22 pagesProject G2 EightPuzzleCarlos Ronquillo CastroPas encore d'évaluation

- DDE Communication Between InTouchDocument8 pagesDDE Communication Between InTouchAlexDavid VelardePas encore d'évaluation

- MC251Document10 pagesMC251Deepak SinghPas encore d'évaluation

- Intervehicle-Communication-Assisted Localization: Nabil Mohamed Drawil, Member, IEEE, and Otman Basir, Member, IEEEDocument14 pagesIntervehicle-Communication-Assisted Localization: Nabil Mohamed Drawil, Member, IEEE, and Otman Basir, Member, IEEENeeraj KumarPas encore d'évaluation

- Ict 3Document7 pagesIct 3Shanto SahaPas encore d'évaluation

- What Will Print Out?: Answer:empty StringDocument6 pagesWhat Will Print Out?: Answer:empty StringiwastruePas encore d'évaluation

- PLSQL 2 2Document23 pagesPLSQL 2 2ssmilePas encore d'évaluation

- Himanshu Manral ResumeDocument1 pageHimanshu Manral ResumeSatish Acharya NamballaPas encore d'évaluation

- Velammal Institute of Technology Chennai: V.SathishDocument26 pagesVelammal Institute of Technology Chennai: V.SathishShubhuPas encore d'évaluation