Vous aimerez peut-être aussi

- General Relationship Between Banker and CustomerDocument11 pagesGeneral Relationship Between Banker and Customermanjunath manjunathPas encore d'évaluation

- Banker-Customer Relationship GuideDocument45 pagesBanker-Customer Relationship GuideSoumendra RoyPas encore d'évaluation

- Special Types of CustomersDocument17 pagesSpecial Types of CustomersAakash Jain100% (1)

- PAYING AND COLLECTING BANKERSDocument21 pagesPAYING AND COLLECTING BANKERSFRANCIS JOSEPH67% (3)

- Duties and Obligations of Paying Bankers and Collecting BankersDocument27 pagesDuties and Obligations of Paying Bankers and Collecting Bankersrajin_rammstein70% (10)

- Types of Banks PDFDocument4 pagesTypes of Banks PDFaakash patilPas encore d'évaluation

- Ancillary Services of BanksDocument19 pagesAncillary Services of BanksAtanu MaityPas encore d'évaluation

- Relationship Between Banker and CustomerDocument16 pagesRelationship Between Banker and CustomeraliishaanPas encore d'évaluation

- Special bank customer typesDocument3 pagesSpecial bank customer typesPoke clipsPas encore d'évaluation

- Banking Regulation ActDocument19 pagesBanking Regulation Actgattani.swatiPas encore d'évaluation

- Special Bank CustomersDocument14 pagesSpecial Bank CustomersFRANCIS JOSEPH100% (2)

- Modes of Charging SecuritiesDocument11 pagesModes of Charging SecuritiesKopal Agarwal50% (4)

- Precautions in Case of Special CustomersDocument6 pagesPrecautions in Case of Special CustomersPoke clips100% (2)

- Winding Up of Banking CompaniesDocument18 pagesWinding Up of Banking CompaniesSandeep Bhosale100% (5)

- Borrowing Power of Company PDFDocument12 pagesBorrowing Power of Company PDFmanishaamba7547Pas encore d'évaluation

- Cooperative BankingDocument8 pagesCooperative BankingvmktptPas encore d'évaluation

- Company Meetings: Meaning and Definition of CompanyDocument14 pagesCompany Meetings: Meaning and Definition of CompanyMohsin AliPas encore d'évaluation

- Special Types of Banker's CustomersDocument7 pagesSpecial Types of Banker's Customerssagarg94gmailcom100% (1)

- Modes of Creating Charges in Banking and InsuranceDocument22 pagesModes of Creating Charges in Banking and InsuranceAdharsh Venkatesan100% (1)

- Banker's RightDocument10 pagesBanker's Rightsagarg94gmailcomPas encore d'évaluation

- Loans and Advances - IRCBDocument68 pagesLoans and Advances - IRCBDr Linda Mary Simon100% (1)

- Banking Ombudsman Scheme in India: A Brief AnalysisDocument18 pagesBanking Ombudsman Scheme in India: A Brief AnalysisVicky DPas encore d'évaluation

- Special CustomersDocument16 pagesSpecial CustomersAnuj KakkarPas encore d'évaluation

- Collecting BankerDocument12 pagesCollecting Bankersagarg94gmailcom100% (3)

- HDFC Bank Services GuideDocument9 pagesHDFC Bank Services GuideRajesh Maharajan50% (2)

- Banking Regulation Act 1949Document17 pagesBanking Regulation Act 1949Sargam MehtaPas encore d'évaluation

- An Assignment On Indian Banking SystemDocument19 pagesAn Assignment On Indian Banking Systemjourneyis life100% (2)

- Principles of Bank LendingDocument14 pagesPrinciples of Bank LendingRishav Malik100% (1)

- Nature and Development of Banking LawDocument4 pagesNature and Development of Banking Lawarti50% (2)

- 32 Nature and Scope of BankingDocument20 pages32 Nature and Scope of Bankingpatilamol019100% (1)

- Special Type of CustomersDocument2 pagesSpecial Type of Customers122087041 YOGESHWAR DPas encore d'évaluation

- Banking Law - Lecture NotesDocument10 pagesBanking Law - Lecture NotesRANDAN SADIQ100% (6)

- Difference Between A Private LTD and Public LTDDocument4 pagesDifference Between A Private LTD and Public LTDShoaib Shaik0% (1)

- Tandon Committee RecommendationsDocument2 pagesTandon Committee RecommendationsPrincess Suganya80% (5)

- PPTDocument24 pagesPPTbpreetybansal100% (2)

- History and Functions of the Reserve Bank of IndiaDocument5 pagesHistory and Functions of the Reserve Bank of IndiaJay Ram100% (1)

- Arguments in Favour and Against Nationalisation of Commercial BanksDocument4 pagesArguments in Favour and Against Nationalisation of Commercial Banksvijayadarshini vPas encore d'évaluation

- Special Types of CustomersDocument29 pagesSpecial Types of CustomersRevathi VadakkedamPas encore d'évaluation

- Paying BankerDocument18 pagesPaying Bankersagarg94gmailcom90% (10)

- Pledged by Non OwnerDocument2 pagesPledged by Non OwnerAdan Hooda50% (2)

- Main Role and Functions of RBIDocument9 pagesMain Role and Functions of RBImalathi100% (1)

- Salient Features of Trade Union ActDocument1 pageSalient Features of Trade Union ActIndrajit Dutta100% (1)

- LIQUIDATION CASE STUDIES ON COMPANIESDocument7 pagesLIQUIDATION CASE STUDIES ON COMPANIESsuresh100% (1)

- Borrowing Powers of A CompanyDocument5 pagesBorrowing Powers of A CompanyimadPas encore d'évaluation

- Garnishee OrderDocument15 pagesGarnishee OrderH B CHIRAG 1950311100% (1)

- Income Tax Authorities - Power and HierarchyDocument13 pagesIncome Tax Authorities - Power and HierarchyHIMANSHI HIMANSHIPas encore d'évaluation

- Project Report On "Debentures"Document14 pagesProject Report On "Debentures"Imran Shaikh88% (8)

- Company Law-Kinds of MeetingDocument8 pagesCompany Law-Kinds of MeetingIrfan Baari100% (1)

- Basic Principles of Sound LendingDocument20 pagesBasic Principles of Sound LendingEknath Birari90% (21)

- Introduction and Company Profile of SbiDocument4 pagesIntroduction and Company Profile of Sbiharman singh100% (1)

- Bank Duties and RightsDocument6 pagesBank Duties and RightsSthita Prajna Mohanty100% (1)

- History, Salient Features and Social Control of Banking Regulation Act, 1949Document9 pagesHistory, Salient Features and Social Control of Banking Regulation Act, 1949Anuj Kamal67% (3)

- Legal Aspect of Banker Customer RelationshipDocument26 pagesLegal Aspect of Banker Customer RelationshipPranjal Srivastava100% (10)

- Banker-Customer Relationship: Rights and ResponsibilitiesDocument33 pagesBanker-Customer Relationship: Rights and ResponsibilitiesFerdous AlaminPas encore d'évaluation

- Chapter Four The Bank - Customer RelashinshipDocument11 pagesChapter Four The Bank - Customer RelashinshipNigus MollaPas encore d'évaluation

- Banker Customer RelationshipDocument35 pagesBanker Customer RelationshipAtia IbnatPas encore d'évaluation

- T-4 CRMDocument26 pagesT-4 CRMNamanPas encore d'évaluation

- Understanding the Relationship Between Bankers and CustomersDocument9 pagesUnderstanding the Relationship Between Bankers and CustomersAbiyPas encore d'évaluation

- Banking Law and OperationsDocument35 pagesBanking Law and OperationsViraja GuruPas encore d'évaluation

- Duties and Rights of Bankers and CustomersDocument33 pagesDuties and Rights of Bankers and CustomersMichael TochukwuPas encore d'évaluation

- 2632 10346 1 PB PDFDocument10 pages2632 10346 1 PB PDFRajyaLakshmiPas encore d'évaluation

- Factoring - BangladeshDocument58 pagesFactoring - Bangladeshrajin_rammstein100% (1)

- 6 Standard STR PresentationDocument31 pages6 Standard STR Presentationrajin_rammsteinPas encore d'évaluation

- Why Credit Goes Bad & CRMDocument22 pagesWhy Credit Goes Bad & CRMrajin_rammsteinPas encore d'évaluation

- Sanction, Documentation and Disbursement of CreditDocument32 pagesSanction, Documentation and Disbursement of Creditrajin_rammstein100% (1)

- Documentation NCC BankDocument35 pagesDocumentation NCC Bankrajin_rammsteinPas encore d'évaluation

- Retail Banking Products at AssetDocument15 pagesRetail Banking Products at Assetrajin_rammsteinPas encore d'évaluation

- Retail Banking at Strategic Sales ApproachDocument23 pagesRetail Banking at Strategic Sales Approachrajin_rammsteinPas encore d'évaluation

- Retail Banking Products at LiabilityDocument25 pagesRetail Banking Products at Liabilityrajin_rammsteinPas encore d'évaluation

- Voucher Preparation: Md. Sahidul AlamDocument18 pagesVoucher Preparation: Md. Sahidul Alamrajin_rammsteinPas encore d'évaluation

- What Makes A Good LoaNDocument25 pagesWhat Makes A Good LoaNrajin_rammsteinPas encore d'évaluation

- Processing and Operation of Cash Credit1 FinalDocument42 pagesProcessing and Operation of Cash Credit1 Finalrajin_rammsteinPas encore d'évaluation

- Question - 1. Write A Letter To Your Friend Describing Your Experience in Banking ServiceDocument15 pagesQuestion - 1. Write A Letter To Your Friend Describing Your Experience in Banking Servicerajin_rammsteinPas encore d'évaluation

- AML Overview 03Document20 pagesAML Overview 03rajin_rammsteinPas encore d'évaluation

- Treasury ManagementDocument16 pagesTreasury Managementrajin_rammsteinPas encore d'évaluation

- Banker Customer RelationshipDocument25 pagesBanker Customer Relationshiprajin_rammstein100% (1)

- ALM: Management of NPA: Sk. Nazibul Islam Faculty Member, BIBMDocument43 pagesALM: Management of NPA: Sk. Nazibul Islam Faculty Member, BIBMrajin_rammsteinPas encore d'évaluation

- EconomicsDocument2 pagesEconomicsrajin_rammsteinPas encore d'évaluation

- Evaluate Portfolio Performance with Treynor, Sharpe, Jensen and Information MeasuresDocument20 pagesEvaluate Portfolio Performance with Treynor, Sharpe, Jensen and Information Measuresrajin_rammsteinPas encore d'évaluation

- Policy On Loan Classification and ProvisioningDocument8 pagesPolicy On Loan Classification and Provisioningrajin_rammsteinPas encore d'évaluation

- Fundamental analysis techniques for commodity pricesDocument46 pagesFundamental analysis techniques for commodity pricesGeeta Kaur BhatiaPas encore d'évaluation

- Principles of Sound Lending, Credit PolicyDocument54 pagesPrinciples of Sound Lending, Credit Policyrajin_rammsteinPas encore d'évaluation

- CRG and Credit Decision LatestDocument33 pagesCRG and Credit Decision Latestrajin_rammstein100% (1)

- ReportDocument21 pagesReportrajin_rammsteinPas encore d'évaluation

- Evaluate Portfolio Performance with Treynor, Sharpe, Jensen and Information MeasuresDocument20 pagesEvaluate Portfolio Performance with Treynor, Sharpe, Jensen and Information Measuresrajin_rammsteinPas encore d'évaluation

- Evaluate Portfolio Performance with Treynor, Sharpe, Jensen and Information MeasuresDocument20 pagesEvaluate Portfolio Performance with Treynor, Sharpe, Jensen and Information Measuresrajin_rammsteinPas encore d'évaluation

- Evaluate Portfolio Performance with Treynor, Sharpe, Jensen and Information MeasuresDocument20 pagesEvaluate Portfolio Performance with Treynor, Sharpe, Jensen and Information Measuresrajin_rammsteinPas encore d'évaluation

- BB SUPERVISION ON BANKINGDocument11 pagesBB SUPERVISION ON BANKINGrajin_rammsteinPas encore d'évaluation

- Guarantee and IndemnityDocument7 pagesGuarantee and Indemnityrajin_rammsteinPas encore d'évaluation

- AgreementForm10045975 29-8-2023 113636Document33 pagesAgreementForm10045975 29-8-2023 113636greenrootfinancialservicesPas encore d'évaluation

- Business Credit Application ReviewDocument12 pagesBusiness Credit Application ReviewKent WhitePas encore d'évaluation

- اسقاطات الانكليزي احمد فوزيDocument17 pagesاسقاطات الانكليزي احمد فوزيali alkassemPas encore d'évaluation

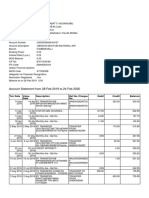

- AccountStatement 3286686240 Oct09 104105Document1 pageAccountStatement 3286686240 Oct09 104105AvijitSinharoyPas encore d'évaluation

- Remedial LawDocument85 pagesRemedial LawRONILO YSMAEL0% (1)

- 01 Metrobank V Junnel's Marketing CorporationDocument4 pages01 Metrobank V Junnel's Marketing CorporationAnonymous bOncqbp8yiPas encore d'évaluation

- OpTransactionHistory30 10 2023Document12 pagesOpTransactionHistory30 10 2023bimalPas encore d'évaluation

- DRC 03Document2 pagesDRC 03sridhar samalaPas encore d'évaluation

- Unifi - Invoice Bulan 2020Document25 pagesUnifi - Invoice Bulan 2020Mich SpikePas encore d'évaluation

- Consumer Protection Laws For Bank CustomersDocument28 pagesConsumer Protection Laws For Bank Customersamritam yadavPas encore d'évaluation

- Urc 522Document6 pagesUrc 522Abhi ShekPas encore d'évaluation

- Technical Specification and Price Proposal 400 KVA Substation-RO1Document8 pagesTechnical Specification and Price Proposal 400 KVA Substation-RO1shanta skymarkPas encore d'évaluation

- Local Govt Accounting ManualDocument17 pagesLocal Govt Accounting ManualRealyn Ambelon100% (1)

- Bharat KoshDocument15 pagesBharat Koshbhartisingh0812Pas encore d'évaluation

- SC Sales & Use Tax Seminar Manual Key PointsDocument206 pagesSC Sales & Use Tax Seminar Manual Key PointsBarbara SalmeronPas encore d'évaluation

- UGC Recognizes CA Course as Post GraduationDocument36 pagesUGC Recognizes CA Course as Post Graduationsunil1287Pas encore d'évaluation

- Pgm2017 ProsDocument76 pagesPgm2017 ProsAnto PaulPas encore d'évaluation

- 2-Day Course On Design and Build Contract - Obligations and ResponsibilitiesDocument4 pages2-Day Course On Design and Build Contract - Obligations and ResponsibilitiesOoi Tze HoongPas encore d'évaluation

- Loyalist College Program Availability List For JAN - 2023 Intake 240522Document6 pagesLoyalist College Program Availability List For JAN - 2023 Intake 240522Jayrajsinh ParmarPas encore d'évaluation

- EBS ConfigurationDocument15 pagesEBS ConfigurationPrateek100% (2)

- Partnership Dispute Over Failed Subdivision Development ProjectDocument32 pagesPartnership Dispute Over Failed Subdivision Development ProjectChristian Miguel Avila AustriaPas encore d'évaluation

- TAXATION SCHEMES EXPLAINEDDocument7 pagesTAXATION SCHEMES EXPLAINEDLeonard CañamoPas encore d'évaluation

- E Passbook 2023 08 30 08 40 08 AmDocument66 pagesE Passbook 2023 08 30 08 40 08 Amkuna gowthamkumarPas encore d'évaluation

- Departmentalized accounting and banking arrangementsDocument4 pagesDepartmentalized accounting and banking arrangementsSurendra SharmaPas encore d'évaluation

- SB Account Statement SummaryDocument15 pagesSB Account Statement SummaryMandalabatti noorasabuPas encore d'évaluation

- ICICI Pru Shubh Raksha One 40769848 MAY 1, 2020 Mr. Mehta Kenil Pradipbhai .Document2 pagesICICI Pru Shubh Raksha One 40769848 MAY 1, 2020 Mr. Mehta Kenil Pradipbhai .AbcPas encore d'évaluation

- CIR v. AlgueDocument3 pagesCIR v. AlguedyosaPas encore d'évaluation

- 99 Ott 12326587075Document1 page99 Ott 12326587075Bransun InternationalPas encore d'évaluation

- AGS Irrigation Raingun QuotationDocument1 pageAGS Irrigation Raingun QuotationAnonymous HdscNyJPas encore d'évaluation

- Bangalore Electricity Supply Company Limited: Thank You!Document12 pagesBangalore Electricity Supply Company Limited: Thank You!Ranjan VPas encore d'évaluation