Vous aimerez peut-être aussi

- Abstract On Formation of SebiDocument2 pagesAbstract On Formation of Sebireshmi duttaPas encore d'évaluation

- Capital Market ReformsDocument8 pagesCapital Market ReformsRiyas ParakkattilPas encore d'évaluation

- Chapter 2 - Rbi, Sebi, IrdaDocument66 pagesChapter 2 - Rbi, Sebi, IrdasejalPas encore d'évaluation

- Role and Functions of IRDADocument2 pagesRole and Functions of IRDAEknath BirariPas encore d'évaluation

- Commercial Banks in IndiaDocument29 pagesCommercial Banks in IndiaVarsha SinghPas encore d'évaluation

- Introduction To Indian Financial SystemDocument31 pagesIntroduction To Indian Financial SystemManoher Reddy100% (2)

- Indian Bnking SystemDocument16 pagesIndian Bnking SystemPriya PriyaPas encore d'évaluation

- AmalgamationDocument14 pagesAmalgamationKrishnakant Mishra100% (1)

- Regulatory Framework For Financial Services in IndiaDocument25 pagesRegulatory Framework For Financial Services in IndiaBishnu PhukanPas encore d'évaluation

- Payment and Small BanksDocument27 pagesPayment and Small BanksDr.Satish RadhakrishnanPas encore d'évaluation

- Regulatory Framework For Banking in IndiaDocument12 pagesRegulatory Framework For Banking in IndiaSidhant NaikPas encore d'évaluation

- Priority Sector LendingDocument9 pagesPriority Sector Lendingjhumli100% (1)

- Jntuk Mba III Sem r13Document26 pagesJntuk Mba III Sem r13j2ee.sridhar7319Pas encore d'évaluation

- The Sick Unit & Case Study NICCO BATTERIESDocument18 pagesThe Sick Unit & Case Study NICCO BATTERIESabhinav75% (4)

- Investors Grievance and RedressalDocument5 pagesInvestors Grievance and RedressalVernica AyemiPas encore d'évaluation

- Residential Status and Tax Incidence: Dr. Niti SaxenaDocument11 pagesResidential Status and Tax Incidence: Dr. Niti SaxenaYusufPas encore d'évaluation

- INTRODUCTION To NPADocument3 pagesINTRODUCTION To NPApradeeppinku50% (4)

- HDFC Amc Mock TestDocument19 pagesHDFC Amc Mock Testyogidildar100% (1)

- Depository ServicesDocument7 pagesDepository ServicesakhilPas encore d'évaluation

- IRDADocument17 pagesIRDAHemant DeshmukhPas encore d'évaluation

- Banking Sector Reforms in IndiaDocument8 pagesBanking Sector Reforms in IndiaJashan Singh GillPas encore d'évaluation

- Globalization ProjectDocument10 pagesGlobalization ProjectSourab DebnathPas encore d'évaluation

- Book Building: Presented By: Rajni Sharma MBA, Final YearDocument23 pagesBook Building: Presented By: Rajni Sharma MBA, Final YearmebtedaiPas encore d'évaluation

- Consumer Protection Act & Redressal Machinery Undre The ActDocument4 pagesConsumer Protection Act & Redressal Machinery Undre The ActPrinceSingh198Pas encore d'évaluation

- Investor Protection Measures by SEBIDocument3 pagesInvestor Protection Measures by SEBIAnonymous J53erBT30QPas encore d'évaluation

- Note On Public IssueDocument9 pagesNote On Public IssueKrish KalraPas encore d'évaluation

- Brief History of RBI: Hilton Young CommissionDocument24 pagesBrief History of RBI: Hilton Young CommissionharishPas encore d'évaluation

- Company Regulatory Legislations in IndiaDocument42 pagesCompany Regulatory Legislations in IndiaAngad SinghPas encore d'évaluation

- International BanksDocument21 pagesInternational BanksPrince KaliaPas encore d'évaluation

- The Narasimham CommitteeDocument18 pagesThe Narasimham CommitteeParul SaxenaPas encore d'évaluation

- Exempted Income Under Section 10Document21 pagesExempted Income Under Section 10Vaishali SharmaPas encore d'évaluation

- Evolution of The Indian Financial SectorDocument18 pagesEvolution of The Indian Financial SectorVikash JontyPas encore d'évaluation

- Financial ServicesDocument2 pagesFinancial ServicesAlok Ranjan100% (1)

- Tandon Committee Report On Working CapitalDocument4 pagesTandon Committee Report On Working CapitalMohitAhujaPas encore d'évaluation

- Presentation On Government (Gilt Edged) SecuritiesDocument22 pagesPresentation On Government (Gilt Edged) Securitieshiteshnandwana100% (1)

- Lecture 5 - Capacity of Parties PDFDocument15 pagesLecture 5 - Capacity of Parties PDFYahya Minhas100% (1)

- Contents of Offer DocumentDocument56 pagesContents of Offer Documentsandeep_agrawal95100% (2)

- Theories of LiquidityDocument21 pagesTheories of LiquidityAashima Sharma Bhasin100% (1)

- Recent Trend in New Issue MarketDocument14 pagesRecent Trend in New Issue MarketAbhi SinhaPas encore d'évaluation

- Study On Bank AudtiDocument17 pagesStudy On Bank AudtiKUNAL GUPTAPas encore d'évaluation

- Introduction To Retail BankingDocument6 pagesIntroduction To Retail BankingS100% (1)

- Investor Protection Measures by SebiDocument3 pagesInvestor Protection Measures by SebiMitu Rana100% (1)

- Financial Statements of Banking CompaniesDocument122 pagesFinancial Statements of Banking CompaniesBiswajit PaulPas encore d'évaluation

- Final PHD Commerce Thesis PDFDocument450 pagesFinal PHD Commerce Thesis PDFMegha Jain BhandariPas encore d'évaluation

- Priority Sector Lending in IndiaDocument40 pagesPriority Sector Lending in IndiaImdad Hazarika100% (1)

- Foreign BanksDocument9 pagesForeign Banks1986anuPas encore d'évaluation

- IntershipDocument65 pagesIntershipainashaikhPas encore d'évaluation

- Case Study On Merchant BankingDocument9 pagesCase Study On Merchant BankingPearl BajpaiPas encore d'évaluation

- Narasimham Committee Report I & IIDocument5 pagesNarasimham Committee Report I & IITejas Makwana0% (3)

- New Issue MarketDocument18 pagesNew Issue Marketoureducation.inPas encore d'évaluation

- Ifim Unit 1 - NotesDocument17 pagesIfim Unit 1 - NotesJyot DhamiPas encore d'évaluation

- Banking Sector ReformsDocument8 pagesBanking Sector ReformsNaveen ChandnaPas encore d'évaluation

- Banking Sector Reforms - Narasimham Committee - Main RecommendationsDocument13 pagesBanking Sector Reforms - Narasimham Committee - Main RecommendationsSakthirama Vadivelu0% (1)

- Banking Sector ReformsDocument14 pagesBanking Sector ReformsPravin ThoratPas encore d'évaluation

- Presented by Group 18: Neha Srivastava Sneha Shivam Garg TarunaDocument41 pagesPresented by Group 18: Neha Srivastava Sneha Shivam Garg TarunaNeha SrivastavaPas encore d'évaluation

- Practical Exercise 2. Banking Sector Reforms - Narasimham Committee - Main RecommendationsDocument13 pagesPractical Exercise 2. Banking Sector Reforms - Narasimham Committee - Main RecommendationsSakthirama VadiveluPas encore d'évaluation

- Module VIII Reading Material Branch Managers TNGDocument273 pagesModule VIII Reading Material Branch Managers TNGIrshadAhmedPas encore d'évaluation

- Chapter 1 Banking An Operations 2Document27 pagesChapter 1 Banking An Operations 2ManavAgarwalPas encore d'évaluation

- Banking An Operations 2 Full PortionDocument126 pagesBanking An Operations 2 Full PortionManavAgarwalPas encore d'évaluation

- Banking Operations 2 Answer KeyDocument48 pagesBanking Operations 2 Answer KeyManavAgarwalPas encore d'évaluation

- SC To Paper 2 Code 01Document7 pagesSC To Paper 2 Code 01ShaguftaPas encore d'évaluation

- Sample Questions: InstructionDocument1 pageSample Questions: InstructionShaguftaPas encore d'évaluation

- Tricks To Solve Time and Distance ProblemsDocument36 pagesTricks To Solve Time and Distance ProblemsvidhyaadhiyamanPas encore d'évaluation

- RBI Assistants Exam Previous Year Solved PaperDocument17 pagesRBI Assistants Exam Previous Year Solved PaperShaguftaPas encore d'évaluation

- Sample Questions: InstructionDocument1 pageSample Questions: InstructionShaguftaPas encore d'évaluation

- Business Plan For A Fast Food Outlet AuthorsDocument6 pagesBusiness Plan For A Fast Food Outlet AuthorsShaguftaPas encore d'évaluation

- GK MonthwiseDocument5 pagesGK MonthwiseShaguftaPas encore d'évaluation

- CA Feb 2014 PDFDocument18 pagesCA Feb 2014 PDFsindhukotaruPas encore d'évaluation

- Gen of WasteDocument34 pagesGen of WasteShaguftaPas encore d'évaluation

- Political 1Document7 pagesPolitical 1ShaguftaPas encore d'évaluation

- AbcdDocument3 pagesAbcdShaguftaPas encore d'évaluation

- Template For Political MarketingDocument4 pagesTemplate For Political MarketingShaguftaPas encore d'évaluation

- IOCL ReportDocument16 pagesIOCL Reportmannu.abhimanyu309893% (14)

- BP Green LifepointDocument37 pagesBP Green LifepointShaguftaPas encore d'évaluation

- Done - Daniel Ekerumeh AduodehDocument62 pagesDone - Daniel Ekerumeh AduodehShaguftaPas encore d'évaluation

- Bus Ethics QuizDocument43 pagesBus Ethics QuizcleofecaloPas encore d'évaluation

- Literature ReviewDocument2 pagesLiterature ReviewShaguftaPas encore d'évaluation

- Customer Satisfaction Survey On BanksDocument32 pagesCustomer Satisfaction Survey On BanksAnkit Singh81% (21)

- The Predictive Nature of Financial Ratios: Adam TurkDocument9 pagesThe Predictive Nature of Financial Ratios: Adam TurkShaguftaPas encore d'évaluation

- IBB June 2012 PDFDocument30 pagesIBB June 2012 PDFAyeshaJangdaPas encore d'évaluation

- BP Green LifepointDocument37 pagesBP Green LifepointShaguftaPas encore d'évaluation

- BP Green LifepointDocument37 pagesBP Green LifepointShaguftaPas encore d'évaluation

- DissertationDocument12 pagesDissertationShaguftaPas encore d'évaluation

- AbcdDocument3 pagesAbcdShaguftaPas encore d'évaluation

- SEZinIndiapwc ReportDocument62 pagesSEZinIndiapwc ReportJeetika LambaPas encore d'évaluation

- 45 ..Islamic BankingDocument47 pages45 ..Islamic BankingShaguftaPas encore d'évaluation

- ChinaDocument1 pageChinaShaguftaPas encore d'évaluation

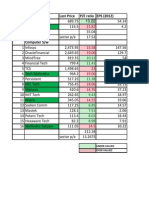

- Sr. No Company Last Price P/E Ratio EPS (2012) : Under Valued Over ValuedDocument5 pagesSr. No Company Last Price P/E Ratio EPS (2012) : Under Valued Over ValuedShaguftaPas encore d'évaluation

- Doing Business With ChinaDocument28 pagesDoing Business With ChinanrkscribdacPas encore d'évaluation

- Backup Reading ITmarketDocument5 pagesBackup Reading ITmarketShaguftaPas encore d'évaluation

- Shortcrete PDFDocument4 pagesShortcrete PDFhelloPas encore d'évaluation

- Teaching Strategies, Styles and Qualities of ADocument6 pagesTeaching Strategies, Styles and Qualities of AjixPas encore d'évaluation

- 10 Me 42 BDocument144 pages10 Me 42 BdineshPas encore d'évaluation

- PDF 20699Document102 pagesPDF 20699Jose Mello0% (1)

- Operations Management: Green Facility Location: Case StudyDocument23 pagesOperations Management: Green Facility Location: Case StudyBhavya KhattarPas encore d'évaluation

- Internal/External Permanent Opportunity: P: S: $51,487.97 - $62,766.29 D: F #: TCHC#10LS29 L: # P: 1Document3 pagesInternal/External Permanent Opportunity: P: S: $51,487.97 - $62,766.29 D: F #: TCHC#10LS29 L: # P: 1a4agarwalPas encore d'évaluation

- Zeb OSARSInstallDocument128 pagesZeb OSARSInstallThien TranPas encore d'évaluation

- El Condor1 Reporte ECP 070506Document2 pagesEl Condor1 Reporte ECP 070506pechan07Pas encore d'évaluation

- ABSTRACT (CG To Epichlorohydrin)Document5 pagesABSTRACT (CG To Epichlorohydrin)Amiel DionisioPas encore d'évaluation

- IT Disaster Recovery Planning ChecklistDocument2 pagesIT Disaster Recovery Planning ChecklistYawe Kizito Brian PaulPas encore d'évaluation

- 20-21 Ipads Shopping GuideDocument1 page20-21 Ipads Shopping Guideapi-348013334Pas encore d'évaluation

- ISM JRF BrochureDocument37 pagesISM JRF BrochureVikas Patel100% (1)

- Cost Justifying HRIS InvestmentsDocument21 pagesCost Justifying HRIS InvestmentsNilesh MandlikPas encore d'évaluation

- Lim Resto (Perencanaan Pendirian Usaha Restaurant Fast Food)Document10 pagesLim Resto (Perencanaan Pendirian Usaha Restaurant Fast Food)Walikutay IndonesiaPas encore d'évaluation

- Edu 637 Lesson Plan Gallivan TerryDocument11 pagesEdu 637 Lesson Plan Gallivan Terryapi-161680522Pas encore d'évaluation

- CS8792 CNS Unit5Document17 pagesCS8792 CNS Unit5024CSE DHARSHINI.APas encore d'évaluation

- IS301 P1 Theory June 2021 P1 TheoryDocument20 pagesIS301 P1 Theory June 2021 P1 Theory50902849Pas encore d'évaluation

- Reading #11Document2 pagesReading #11Yojana Vanessa Romero67% (3)

- Episode 1Document10 pagesEpisode 1ethel bacalso100% (1)

- PD Download Fs 1608075814173252Document1 pagePD Download Fs 1608075814173252straullePas encore d'évaluation

- Key GroupsDocument11 pagesKey GroupsJose RodríguezPas encore d'évaluation

- Firearm Laws in PennsylvaniaDocument2 pagesFirearm Laws in PennsylvaniaJesse WhitePas encore d'évaluation

- Best Evidence Rule CasesDocument5 pagesBest Evidence Rule CasesRemy Rose AlegrePas encore d'évaluation

- Maxiim Vehicle Diagnostic ReportDocument3 pagesMaxiim Vehicle Diagnostic ReportCarlos Cobaleda GarcíaPas encore d'évaluation

- Plant Management TafskillsDocument4 pagesPlant Management TafskillsTHEOPHILUS ATO FLETCHERPas encore d'évaluation

- Sevana - Hospital Kiosk ConceptNoteDocument103 pagesSevana - Hospital Kiosk ConceptNotemanojPas encore d'évaluation

- A) Discuss The Managing Director's Pricing Strategy in The Circumstances Described Above. (5 Marks)Document17 pagesA) Discuss The Managing Director's Pricing Strategy in The Circumstances Described Above. (5 Marks)Hannah KayyPas encore d'évaluation

- FFA Test CHP INV and 16Document8 pagesFFA Test CHP INV and 16zainabPas encore d'évaluation

- Quiz 1 - Domain Modeling With Answer KeyDocument5 pagesQuiz 1 - Domain Modeling With Answer Keyprincess100267% (3)

- From 1-73Document95 pagesFrom 1-73Shrijan ChapagainPas encore d'évaluation