Vous aimerez peut-être aussi

- Present Status of Agriculture in IndiaDocument36 pagesPresent Status of Agriculture in IndiawaragainstlovePas encore d'évaluation

- Assamese Its Formation and DevelopmentDocument424 pagesAssamese Its Formation and DevelopmentwaragainstlovePas encore d'évaluation

- Another Answer: The "Barter" System - It Was Suggested That "Barter"Document6 pagesAnother Answer: The "Barter" System - It Was Suggested That "Barter"waragainstlovePas encore d'évaluation

- IndiaDocument28 pagesIndiaHarsh KhandelwalPas encore d'évaluation

- PDSDocument20 pagesPDSwaragainstlovePas encore d'évaluation

- Articles From: Grade B Officer Jobs RBI Assistant Exam Syllabus Best Books, PreparationDocument3 pagesArticles From: Grade B Officer Jobs RBI Assistant Exam Syllabus Best Books, PreparationwaragainstlovePas encore d'évaluation

- Roject Ased Earning: © Ncert Not To Be RepublishedDocument24 pagesRoject Ased Earning: © Ncert Not To Be RepublishedwaragainstlovePas encore d'évaluation

- Role of Customs in International Relations Parthasarathi ShomeDocument15 pagesRole of Customs in International Relations Parthasarathi ShomewaragainstlovePas encore d'évaluation

- Ecology and The Environment: Taking Care of What We've Been GivenDocument53 pagesEcology and The Environment: Taking Care of What We've Been GivenwaragainstlovePas encore d'évaluation

- Global Climate Change:: Health Risks - and Preventive StrategiesDocument47 pagesGlobal Climate Change:: Health Risks - and Preventive StrategieswaragainstlovePas encore d'évaluation

- Mannig J. Simidian: MacroeconomicsDocument11 pagesMannig J. Simidian: MacroeconomicswaragainstlovePas encore d'évaluation

- E-Governance Project of Sangli-Miraj-Kupwad Municipal Corporation (SMC)Document42 pagesE-Governance Project of Sangli-Miraj-Kupwad Municipal Corporation (SMC)waragainstlovePas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Unit 2 - Sources of FinanceDocument20 pagesUnit 2 - Sources of Finance2154 taibakhatunPas encore d'évaluation

- Cash Book Practice QuesDocument3 pagesCash Book Practice Quesnehal dagarPas encore d'évaluation

- Electoral Bond Application Form EnglishDocument2 pagesElectoral Bond Application Form EnglishJitendra RavalPas encore d'évaluation

- Portfolio Management ASSIGN..Document23 pagesPortfolio Management ASSIGN..Farah Farah Essam Abbas HamisaPas encore d'évaluation

- Property of STIDocument2 pagesProperty of STIab galePas encore d'évaluation

- Fs AnalysisDocument14 pagesFs Analysisyusuf pashaPas encore d'évaluation

- Credit Scandal - LGCDocument10 pagesCredit Scandal - LGCRechel JovellanosPas encore d'évaluation

- Chapter 18Document12 pagesChapter 18ks1043210Pas encore d'évaluation

- All All: 90011056262 Incoming: 5, Outgoing: 4Document1 pageAll All: 90011056262 Incoming: 5, Outgoing: 4Elfrian Banar SPas encore d'évaluation

- Payment Information New Balance Minimum Payment Due Payment Due Date Account SummaryDocument6 pagesPayment Information New Balance Minimum Payment Due Payment Due Date Account SummaryEng. Sameh AlsahafiPas encore d'évaluation

- Adjustment Entries II - Accounting-Workbook - Zaheer-SwatiDocument6 pagesAdjustment Entries II - Accounting-Workbook - Zaheer-SwatiZaheer SwatiPas encore d'évaluation

- Financial Reporting in PakistanDocument7 pagesFinancial Reporting in Pakistanamna hafeezPas encore d'évaluation

- Module 8. International Financial Market and Innovations ObjectivesDocument9 pagesModule 8. International Financial Market and Innovations ObjectivesSalma AbdullahPas encore d'évaluation

- Sbi MF SipDocument2 pagesSbi MF Sipstuti1987Pas encore d'évaluation

- Mas 01 Basic Considerations Reo CpaDocument10 pagesMas 01 Basic Considerations Reo CpaMila Casandra CastañedaPas encore d'évaluation

- CMA Volume 2 MergedDocument153 pagesCMA Volume 2 MergedShyaambhavi NsPas encore d'évaluation

- Debt Collector ScriptDocument4 pagesDebt Collector ScriptElcana Mathieu0% (1)

- Vanguard Long-Term Government Bond ETF 10+Document2 pagesVanguard Long-Term Government Bond ETF 10+Roberto PerezPas encore d'évaluation

- Fabm 2-5Document24 pagesFabm 2-5Andrei Bana100% (2)

- Session 4 - Internal Control Procedures in AccountingDocument15 pagesSession 4 - Internal Control Procedures in AccountingRej PanganibanPas encore d'évaluation

- Dissertation On Mutual Funds in IndiaDocument5 pagesDissertation On Mutual Funds in IndiaPaperHelperUK100% (1)

- Partnership PDFDocument1 pagePartnership PDFAoiPas encore d'évaluation

- ForexDocument16 pagesForexSandeepa ThirthahalliPas encore d'évaluation

- Lesson PlanDocument5 pagesLesson PlanMa. Katrina BusaPas encore d'évaluation

- SBCL Purchase 38+2% DoaDocument15 pagesSBCL Purchase 38+2% DoaVIP smailPas encore d'évaluation

- Soa300722Document1 pageSoa300722Andy NainggolanPas encore d'évaluation

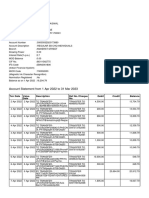

- Bank StatementDocument15 pagesBank StatementUmasankarPas encore d'évaluation

- BBAW2103Document13 pagesBBAW2103Nurul IzzatyPas encore d'évaluation

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Deeksha SinghPas encore d'évaluation

- 555841534IN MF MOTILAL FACTSHEET 31-07-2021 FinalDocument151 pages555841534IN MF MOTILAL FACTSHEET 31-07-2021 FinalVisnu SankarPas encore d'évaluation