Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Lussier 3 Ech 05Document50 pagesLussier 3 Ech 05ssregens82Pas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Building Multi-Tier Web Applications in Virtual EnvironmentsDocument30 pagesBuilding Multi-Tier Web Applications in Virtual Environmentsssregens82Pas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Orchestro State Inventory Management 2015Document8 pagesOrchestro State Inventory Management 2015ssregens82Pas encore d'évaluation

- Supplier General QualificationsDocument3 pagesSupplier General Qualificationsssregens82Pas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Static Picture Effects For Powerpoint Slides: Reproductio N Instructions Printing Instructions Removing InstructionsDocument17 pagesStatic Picture Effects For Powerpoint Slides: Reproductio N Instructions Printing Instructions Removing Instructionsssregens82Pas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- CHP 3Document2 pagesCHP 3ssregens82Pas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Risk and Rates of Return: Learning ObjectivesDocument36 pagesRisk and Rates of Return: Learning Objectivesssregens82Pas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Problems, Problem Spaces and Search: Dr. Suthikshn KumarDocument47 pagesProblems, Problem Spaces and Search: Dr. Suthikshn Kumarssregens82Pas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Judicial Power of Supreme CourtDocument2 pagesJudicial Power of Supreme Courtssregens82Pas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Chapter 1 BowersoxDocument38 pagesChapter 1 Bowersoxssregens82100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Vcost DemoDocument2 pagesVcost Demossregens82Pas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Week 8 AssignmentDocument5 pagesWeek 8 Assignmentssregens82100% (2)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Transportation and Logistics OptimizationDocument18 pagesTransportation and Logistics Optimizationssregens82Pas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- AMIS 525 Pop Quiz - Chapters 22 and 23Document5 pagesAMIS 525 Pop Quiz - Chapters 22 and 23ssregens82Pas encore d'évaluation

- Signs For Income VarianceDocument1 pageSigns For Income Variancessregens82Pas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Time Value PracticeDocument1 pageTime Value Practicessregens82Pas encore d'évaluation

- Regular Flow Irregular Flow Irregular Flow DepreciationDocument1 pageRegular Flow Irregular Flow Irregular Flow Depreciationssregens82Pas encore d'évaluation

- V Ac - SC V (Aa Ar) - (Sa SR) V (Aa Ar) - (Aa SR) + (Aa SR) - (Sa SR) V ( (Aa Ar) - (Aa SR) ) + ( (Aa SR) - (Sa SR) )Document1 pageV Ac - SC V (Aa Ar) - (Sa SR) V (Aa Ar) - (Aa SR) + (Aa SR) - (Sa SR) V ( (Aa Ar) - (Aa SR) ) + ( (Aa SR) - (Sa SR) )ssregens82Pas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- I (P Q) - (V Q) - F: The Fundamental EquationDocument1 pageI (P Q) - (V Q) - F: The Fundamental Equationssregens82Pas encore d'évaluation

- TPRICEDocument1 pageTPRICEssregens82Pas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

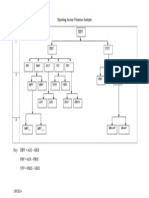

- Operating Income Variances DiagramDocument1 pageOperating Income Variances Diagramssregens82Pas encore d'évaluation

- Ri RoiDocument1 pageRi Roissregens82Pas encore d'évaluation

- Total For 5 Years Each YearDocument1 pageTotal For 5 Years Each Yearssregens82Pas encore d'évaluation

- Percent DoneDocument1 pagePercent Donessregens82Pas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Process StepsDocument1 pageProcess Stepsssregens82Pas encore d'évaluation

- KSFEDocument10 pagesKSFEjojuthimothyPas encore d'évaluation

- Kingdom Annual Audited Results Dec 2009Document11 pagesKingdom Annual Audited Results Dec 2009Kristi DuranPas encore d'évaluation

- Buyers CreditDocument8 pagesBuyers Creditsudhir.kochhar3530Pas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Npa's ContentDocument46 pagesNpa's ContentPiyushVarmaPas encore d'évaluation

- Terms and Conditions of Quotation and SaleDocument7 pagesTerms and Conditions of Quotation and SaleNuzuliana EnuzPas encore d'évaluation

- Updated Intercompany Agreements Presentation 06 23Document62 pagesUpdated Intercompany Agreements Presentation 06 23FlorinPas encore d'évaluation

- New In-Principle Approval Format Bank of BarodaDocument13 pagesNew In-Principle Approval Format Bank of BarodaPriyanka VermaPas encore d'évaluation

- The Politics of Mass Consumption in Postwar AmericaDocument5 pagesThe Politics of Mass Consumption in Postwar Americaallure_chPas encore d'évaluation

- Working Capital Management of AccDocument52 pagesWorking Capital Management of AccSoham Khanna75% (4)

- Solution Manual - Chapter 6Document11 pagesSolution Manual - Chapter 6psrikanthmbaPas encore d'évaluation

- FINAL Examination: Basic Finance: Money, Banking and CreditDocument5 pagesFINAL Examination: Basic Finance: Money, Banking and CreditHoward UntalanPas encore d'évaluation

- Fabozzi Ch15 BMAS 7thedDocument42 pagesFabozzi Ch15 BMAS 7thedPriya Ranjan SinghPas encore d'évaluation

- Bharat Microfinance Report 20151Document122 pagesBharat Microfinance Report 20151Primal PatelPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- (Manual Form) Application Solar Up To 12kwDocument16 pages(Manual Form) Application Solar Up To 12kwYeit HauPas encore d'évaluation

- Partnership Memory Aid AteneoDocument10 pagesPartnership Memory Aid AteneoKenette Diane CantubaPas encore d'évaluation

- Hire Purchase and LeasingDocument30 pagesHire Purchase and LeasingShreyas Khanore100% (1)

- An Evaluation of The Efficiency of Loan Collection Policies and Procedures Among Selected MultiDocument7 pagesAn Evaluation of The Efficiency of Loan Collection Policies and Procedures Among Selected MultiSanta Dela Cruz NaluzPas encore d'évaluation

- Deutsche Bank's Corporate and Investment Banking The Anshu Jain WayDocument3 pagesDeutsche Bank's Corporate and Investment Banking The Anshu Jain WaySandeep MishraPas encore d'évaluation

- Bank On YourselfDocument62 pagesBank On YourselfRay Woolson100% (5)

- SV - INFO 31787 Accounting Information Systems Midterm Theory Exam - Summer 2017 Version A1 PDFDocument7 pagesSV - INFO 31787 Accounting Information Systems Midterm Theory Exam - Summer 2017 Version A1 PDFGamersPas encore d'évaluation

- 10 2005 Jun QDocument6 pages10 2005 Jun Qspinster4Pas encore d'évaluation

- Full 2014 2015 PDFDocument282 pagesFull 2014 2015 PDFFarjana Hossain DharaPas encore d'évaluation

- Analyst Meet Presentation (Company Update)Document25 pagesAnalyst Meet Presentation (Company Update)Shyam SunderPas encore d'évaluation

- Analysis of Credit Facilities To Small Scale FarmersDocument88 pagesAnalysis of Credit Facilities To Small Scale FarmersSebastian Grove100% (6)

- Corporate BankingDocument100 pagesCorporate Bankingvinesh1515100% (3)

- NALCO EditedDocument97 pagesNALCO EditedSankha MahapatraPas encore d'évaluation

- Rickshaw SanghDocument6 pagesRickshaw SanghVishnu RaghunathanPas encore d'évaluation

- Working Capital Management: A Study On British American Tobacco Bangladesh Company LTDDocument7 pagesWorking Capital Management: A Study On British American Tobacco Bangladesh Company LTDBagus RhizkyPas encore d'évaluation

- Advance BNK Management - Credit PDFDocument2 pagesAdvance BNK Management - Credit PDFPratheesh TulsiPas encore d'évaluation

- Defendant Board of Governors Motion For Summary Judgment (Lawsuit #3)Document413 pagesDefendant Board of Governors Motion For Summary Judgment (Lawsuit #3)Vern McKinleyPas encore d'évaluation