Vous aimerez peut-être aussi

- Regulatory and Comm Aspects of Power Generation - 24.06.2019Document56 pagesRegulatory and Comm Aspects of Power Generation - 24.06.2019dks12Pas encore d'évaluation

- C& I For SupercriticalDocument93 pagesC& I For SupercriticalPrudhvi RajPas encore d'évaluation

- Otsc - Control Final-BoilerDocument85 pagesOtsc - Control Final-BoilerKumar100% (1)

- BHELDocument4 pagesBHELNageswara Reddy GajjalaPas encore d'évaluation

- Benson BoilerDocument20 pagesBenson BoilerjigsprajapatiPas encore d'évaluation

- 1.1 Background of Project 1.2 Assignment & Objectives 1.3 Instruction To Reader 1.4 Limitation 1.5 Organisational ProfileDocument87 pages1.1 Background of Project 1.2 Assignment & Objectives 1.3 Instruction To Reader 1.4 Limitation 1.5 Organisational Profilezerocool86100% (1)

- Steam Turbine: Life Time Calculations and Life Limitings FactorsDocument38 pagesSteam Turbine: Life Time Calculations and Life Limitings FactorsPPG CoverPas encore d'évaluation

- 1c Low Mass Flux Once Through Boiler Design Application and PDFDocument52 pages1c Low Mass Flux Once Through Boiler Design Application and PDFfrlamontPas encore d'évaluation

- Super Critical PresentationDocument46 pagesSuper Critical PresentationSam100% (1)

- Oxyfuel Combustion: R&D ActivitiesDocument21 pagesOxyfuel Combustion: R&D ActivitiesPablo Cadena100% (1)

- Checklist - Stress AnalysisDocument2 pagesChecklist - Stress AnalysisRamalingam PrabhakaranPas encore d'évaluation

- File - 20220523 - 210015 - Pid FGDDocument11 pagesFile - 20220523 - 210015 - Pid FGDThắng NguyễnPas encore d'évaluation

- T10206-DN02-P1ZEN - 860012 FGD Capability Test Procedure - Rev 0Document13 pagesT10206-DN02-P1ZEN - 860012 FGD Capability Test Procedure - Rev 0Thắng NguyễnPas encore d'évaluation

- UntitledDocument8 pagesUntitledPMG Bhuswal ProjectPas encore d'évaluation

- 0260-101-01-TR-PVM-U-020-03 Sizing Calculation of FurnaceDocument9 pages0260-101-01-TR-PVM-U-020-03 Sizing Calculation of Furnaceanil peralaPas encore d'évaluation

- Presentation of Kawasaki FGD and SCR SystemDocument20 pagesPresentation of Kawasaki FGD and SCR Systemjitendrashukla10836Pas encore d'évaluation

- Catalog Steam Turbines 2013 Engl PDFDocument36 pagesCatalog Steam Turbines 2013 Engl PDFvamsiklPas encore d'évaluation

- Supercritical Boiler Cleanup Cycle: Ranjan KumarDocument23 pagesSupercritical Boiler Cleanup Cycle: Ranjan Kumarscentpcbarauni BARAUNIPas encore d'évaluation

- Turbo Generator & Its AuxiliariesDocument89 pagesTurbo Generator & Its AuxiliariesPapun ScribdPas encore d'évaluation

- LMZ TechDocument29 pagesLMZ TechGajanan JagtapPas encore d'évaluation

- Presentation Synopsis: 18 Unit Level Professional Circle ConventionDocument9 pagesPresentation Synopsis: 18 Unit Level Professional Circle ConventionSCE Stage2Pas encore d'évaluation

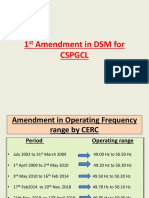

- 1 Amendment in DSM For CSPGCLDocument19 pages1 Amendment in DSM For CSPGCLashish jainPas encore d'évaluation

- Modernization and Life ExtansionDocument67 pagesModernization and Life ExtansionDangolPas encore d'évaluation

- Development of Steam DrumDocument8 pagesDevelopment of Steam DrumRaja SellappanPas encore d'évaluation

- Basic Governer ControlsDocument14 pagesBasic Governer ControlspankajPas encore d'évaluation

- Turbine ModelsDocument4 pagesTurbine Modelsstupid143Pas encore d'évaluation

- BoilerOpt Overview and Results 7-18-16-UsefulDocument53 pagesBoilerOpt Overview and Results 7-18-16-Usefultrung2iPas encore d'évaluation

- LP Turbine Exhaust Loss CurveDocument1 pageLP Turbine Exhaust Loss CurveShameer MajeedPas encore d'évaluation

- 1-4 Start Up Boost LeafletDocument4 pages1-4 Start Up Boost LeafletsdiamanPas encore d'évaluation

- 3-77-06 Field Weld Ends Pumps& Valves Conrolled Circulation & CC UnitsDocument10 pages3-77-06 Field Weld Ends Pumps& Valves Conrolled Circulation & CC UnitsJKKPas encore d'évaluation

- Hindalco Details PDFDocument264 pagesHindalco Details PDFSiddhant SatpathyPas encore d'évaluation

- Anthracite Firing at Central Power Stations For The - Foster WheelerDocument21 pagesAnthracite Firing at Central Power Stations For The - Foster WheelerThanh Luan NguyenPas encore d'évaluation

- 50-83-02 Spec. For Arc & Capacitor Discharge Weldingt of Pr. & Non-Pr. PartsDocument6 pages50-83-02 Spec. For Arc & Capacitor Discharge Weldingt of Pr. & Non-Pr. PartsJKKPas encore d'évaluation

- C&i SystemsDocument116 pagesC&i SystemsbamzPas encore d'évaluation

- QMS Paper PDFDocument13 pagesQMS Paper PDFPrisman Cahya NugrahaPas encore d'évaluation

- S 774201Document34 pagesS 774201Ben KerryPas encore d'évaluation

- Power Plant and Calculations - Power Plant Equipments Standard Operating Procedures (SOP)Document7 pagesPower Plant and Calculations - Power Plant Equipments Standard Operating Procedures (SOP)RajeshPas encore d'évaluation

- Chapter-2 Steam Cycle TheoryDocument20 pagesChapter-2 Steam Cycle TheoryPhanindra Kumar J100% (1)

- Flexible Operation in Coal Based Plant: By-SNEHESH BANERJEE, Operation Services, CCDocument27 pagesFlexible Operation in Coal Based Plant: By-SNEHESH BANERJEE, Operation Services, CCLakshmi NarayanPas encore d'évaluation

- Schematic Diagram of Sealing & Cooling Water For CepDocument12 pagesSchematic Diagram of Sealing & Cooling Water For Cepjp mishraPas encore d'évaluation

- TurbineDocument23 pagesTurbineKarthikeyanPas encore d'évaluation

- Steam Turbine Unloading and Shut-Down of Operation Turbine/Generator Shut-Down DiagramDocument5 pagesSteam Turbine Unloading and Shut-Down of Operation Turbine/Generator Shut-Down Diagramparthibanemails5779Pas encore d'évaluation

- CHP Flow DiagramDocument2 pagesCHP Flow DiagramShajal ChowdhuryPas encore d'évaluation

- ATT01 UTR01MEK - F21DM001 A Functional DescriptionDocument23 pagesATT01 UTR01MEK - F21DM001 A Functional DescriptionSUNILPas encore d'évaluation

- Paper 6 FRF-lube - Oil - MixingDocument34 pagesPaper 6 FRF-lube - Oil - MixingsoorajssPas encore d'évaluation

- 08C - Protection - SeqDocument16 pages08C - Protection - SeqService Port100% (1)

- BBC - Steam Turbine - 100 MWDocument42 pagesBBC - Steam Turbine - 100 MWvenkata madhavPas encore d'évaluation

- Lalitpur Superthermal Power Project - 3 X 660 MWDocument10 pagesLalitpur Superthermal Power Project - 3 X 660 MWpramod_nandaPas encore d'évaluation

- Off - Site Facilities Coal Transportation Handling: 1 June 2010 PMI Revision 00 1Document40 pagesOff - Site Facilities Coal Transportation Handling: 1 June 2010 PMI Revision 00 1Ezhil Vendhan PalanisamyPas encore d'évaluation

- Thermax - NTPC PresentationDocument57 pagesThermax - NTPC PresentationPiyush MalviyaPas encore d'évaluation

- Fuel FiringDocument39 pagesFuel Firingnetygen1Pas encore d'évaluation

- NTPCVBR1Document91 pagesNTPCVBR1DenkaPas encore d'évaluation

- Familiarisation of PP-3 Power PlantsDocument11 pagesFamiliarisation of PP-3 Power PlantsPushpendra Mishra100% (1)

- Spiral Wound Gasket: Bharat Heavy Electricals Limited Tiruchirappalli-620 014Document54 pagesSpiral Wound Gasket: Bharat Heavy Electricals Limited Tiruchirappalli-620 014Ramalingam PrabhakaranPas encore d'évaluation

- CHP - ECL Chairman Review PresentationDocument29 pagesCHP - ECL Chairman Review PresentationdebajyotiPas encore d'évaluation

- 13 Internal Walkway and PerformanceDocument24 pages13 Internal Walkway and PerformanceDSGPas encore d'évaluation

- 8 95 01 Weld Procedure Spec ChattanoogaDocument40 pages8 95 01 Weld Procedure Spec ChattanoogaJKKPas encore d'évaluation

- TARIFF DESIGN For GENERATING STATIONSDocument16 pagesTARIFF DESIGN For GENERATING STATIONSNaveen Chodagiri100% (1)

- Electricity Pricing (PFC Modified)Document43 pagesElectricity Pricing (PFC Modified)havejsnjPas encore d'évaluation

- Tariff Structure: 2014-19: Salient Features of CERC (Terms and Conditions of Tariff) Regulations, 2014Document8 pagesTariff Structure: 2014-19: Salient Features of CERC (Terms and Conditions of Tariff) Regulations, 2014netygen1Pas encore d'évaluation

- Recapitulation of Concepts.: /var/www/apps/conversion/tmp/scratch - 1/209957082Document7 pagesRecapitulation of Concepts.: /var/www/apps/conversion/tmp/scratch - 1/209957082Ezhil Vendhan PalanisamyPas encore d'évaluation

- Project Planning and Interface With Govt. Agencies: S.D.Mathur AGM (Systems)Document41 pagesProject Planning and Interface With Govt. Agencies: S.D.Mathur AGM (Systems)Ezhil Vendhan PalanisamyPas encore d'évaluation

- Water TreatmentDocument27 pagesWater TreatmentEzhil Vendhan PalanisamyPas encore d'évaluation

- Off - Site Facilities Coal Transportation Handling: 1 June 2010 PMI Revision 00 1Document40 pagesOff - Site Facilities Coal Transportation Handling: 1 June 2010 PMI Revision 00 1Ezhil Vendhan PalanisamyPas encore d'évaluation

- AIM Training Report - ATANUDocument9 pagesAIM Training Report - ATANUEzhil Vendhan PalanisamyPas encore d'évaluation

- Project Management in Thermal Power Plant-Ntpc'S ExperienceDocument58 pagesProject Management in Thermal Power Plant-Ntpc'S ExperienceEzhil Vendhan Palanisamy100% (1)

- Site Visit Report - GeneralDocument3 pagesSite Visit Report - GeneralEzhil Vendhan PalanisamyPas encore d'évaluation

- FR Formulation&Infrastructure For EtsDocument27 pagesFR Formulation&Infrastructure For EtsEzhil Vendhan PalanisamyPas encore d'évaluation

- Project Management in Thermal Power Plant-Ntpc'S ExperienceDocument58 pagesProject Management in Thermal Power Plant-Ntpc'S ExperienceEzhil Vendhan PalanisamyPas encore d'évaluation

- Burner Block AlignmentDocument12 pagesBurner Block AlignmentEzhil Vendhan PalanisamyPas encore d'évaluation

- Raw WaterDocument41 pagesRaw WaterEzhil Vendhan PalanisamyPas encore d'évaluation

- PW SystemDocument12 pagesPW SystemEzhil Vendhan PalanisamyPas encore d'évaluation

- O&M BudgetDocument17 pagesO&M BudgetEzhil Vendhan PalanisamyPas encore d'évaluation

- Boiler EffyDocument32 pagesBoiler EffyEzhil Vendhan PalanisamyPas encore d'évaluation

- Power Trading PptFinalDocument54 pagesPower Trading PptFinalEzhil Vendhan PalanisamyPas encore d'évaluation

- Endorsement Sheet For QP: Reference / Standard / Field Quality Plan (RQP / SQP/RFQP/SFQP) To Be Filled in by NTPCDocument33 pagesEndorsement Sheet For QP: Reference / Standard / Field Quality Plan (RQP / SQP/RFQP/SFQP) To Be Filled in by NTPCEzhil Vendhan Palanisamy100% (1)

- Gen ProtectionDocument78 pagesGen ProtectionEzhil Vendhan PalanisamyPas encore d'évaluation

- Critical Chain Project Management N NotesDocument22 pagesCritical Chain Project Management N NotesEzhil Vendhan PalanisamyPas encore d'évaluation

- Steam BlowingDocument28 pagesSteam BlowingEzhil Vendhan Palanisamy100% (1)

- O&M BudgetDocument17 pagesO&M BudgetEzhil Vendhan PalanisamyPas encore d'évaluation

- Burner Block AlignmentDocument12 pagesBurner Block AlignmentEzhil Vendhan PalanisamyPas encore d'évaluation

- Feasibility Report Project Cost APPRAISALDocument30 pagesFeasibility Report Project Cost APPRAISALEzhil Vendhan PalanisamyPas encore d'évaluation

- Gen ProtectionDocument78 pagesGen ProtectionEzhil Vendhan PalanisamyPas encore d'évaluation

- Raw WaterDocument41 pagesRaw WaterEzhil Vendhan PalanisamyPas encore d'évaluation

- Boiler EffyDocument32 pagesBoiler EffyEzhil Vendhan PalanisamyPas encore d'évaluation

- Power Factor & Its ImprovementDocument23 pagesPower Factor & Its ImprovementEzhil Vendhan PalanisamyPas encore d'évaluation

- Energy Audit and DSM: Ceetem-CosDocument38 pagesEnergy Audit and DSM: Ceetem-CosEzhil Vendhan PalanisamyPas encore d'évaluation

- Class 5 EvsDocument33 pagesClass 5 EvsnngowriharibaskarPas encore d'évaluation

- Energy MixDocument10 pagesEnergy MixPara DisePas encore d'évaluation

- SOLID FUELS WRITTEN REPORT (Draft)Document21 pagesSOLID FUELS WRITTEN REPORT (Draft)Stacy Chan0% (1)

- Comparative Analysis of The Modes of Transportation of Petroleum Products Out of Kaduna Refinery and Petro-Chemical Company, NigeriaDocument95 pagesComparative Analysis of The Modes of Transportation of Petroleum Products Out of Kaduna Refinery and Petro-Chemical Company, NigeriaPaco Trooper100% (1)

- 1.A.1 Energy Industries 2019Document116 pages1.A.1 Energy Industries 2019izudindPas encore d'évaluation

- B. B. ALE Department of Mechanical EngineeringDocument36 pagesB. B. ALE Department of Mechanical EngineeringRam Krishna SinghPas encore d'évaluation

- Chernobyl Notebook 1989Document78 pagesChernobyl Notebook 1989the_assimilator67% (6)

- 3412 eDocument12 pages3412 eBruno Ventura100% (1)

- Greta Thunberg and George Monbiot On The Climate Crisis: TasksDocument5 pagesGreta Thunberg and George Monbiot On The Climate Crisis: TasksFsartPas encore d'évaluation

- Vale Day 2022Document82 pagesVale Day 2022Gatot WinotoPas encore d'évaluation

- Rathore Et AlDocument7 pagesRathore Et AlIqra SarfrazPas encore d'évaluation

- Recent Advances in Liquid Organic Hydrogen Carriers: An Alcohol-Based Hydrogen EconomyDocument15 pagesRecent Advances in Liquid Organic Hydrogen Carriers: An Alcohol-Based Hydrogen EconomySajid Mohy Ul Din100% (1)

- CORSIA - The First Internationally Adopted Approach To Calculate Life-Cycle GHG Emissions For Aviation FuelsDocument9 pagesCORSIA - The First Internationally Adopted Approach To Calculate Life-Cycle GHG Emissions For Aviation FuelsNisarg SonaniPas encore d'évaluation

- Challenges of Using EFB As Boiler FuelDocument15 pagesChallenges of Using EFB As Boiler FuelAnonymous DJrec20% (1)

- What Is GroundwaterDocument44 pagesWhat Is GroundwaterbokanegPas encore d'évaluation

- Atomization and SpraysDocument136 pagesAtomization and Sprayssaeedkheirati100% (1)

- Moisture Content of CoalDocument4 pagesMoisture Content of CoalSaad Ahmed100% (1)

- Internal Combustion EnginesDocument2 pagesInternal Combustion EnginesDhaval PanchalPas encore d'évaluation

- On Biogas Enrichment and Bottling Technology - IITD - IndiaDocument38 pagesOn Biogas Enrichment and Bottling Technology - IITD - Indiaअश्विनी सोनी100% (3)

- PcdpowDocument146 pagesPcdpowAadrita GhoshPas encore d'évaluation

- Shree Cement AR 15 16 PDFDocument231 pagesShree Cement AR 15 16 PDFAbhishek RawatPas encore d'évaluation

- SolteQ Catalog Solarroofs PDFDocument314 pagesSolteQ Catalog Solarroofs PDFAtharva KakdePas encore d'évaluation

- Multiple Choice Questions For Class VIII: Crop Production and ManagementDocument21 pagesMultiple Choice Questions For Class VIII: Crop Production and ManagementMohit GargPas encore d'évaluation

- 03 HRR Flame Height Burning Duration CalculationsDocument2 pages03 HRR Flame Height Burning Duration CalculationsjovanivanPas encore d'évaluation

- ChemistryDocument24 pagesChemistryBushra Amir X-G-APas encore d'évaluation

- Para Jumble / Jumbled Sentence Short Tricks & Questions With SolutionsDocument56 pagesPara Jumble / Jumbled Sentence Short Tricks & Questions With SolutionsPrãkhąř Řäj100% (1)

- Current Affairs: Energy Crisis in PakistanDocument10 pagesCurrent Affairs: Energy Crisis in PakistanArsalan Khan GhauriPas encore d'évaluation

- Mwananchi Gas Concept PaperDocument66 pagesMwananchi Gas Concept PaperIddi OmarPas encore d'évaluation

- Basic Mechanical Engineering 2Nd Edition Pravin Kumar Full ChapterDocument67 pagesBasic Mechanical Engineering 2Nd Edition Pravin Kumar Full Chapterjefferson.kleckner559100% (8)

- Analysis of High Speed Rail S PotentialDocument20 pagesAnalysis of High Speed Rail S PotentialDe'Von JPas encore d'évaluation