Vous aimerez peut-être aussi

- Export Growth Sources of Bangladesh RMGDocument88 pagesExport Growth Sources of Bangladesh RMGAziz HoquePas encore d'évaluation

- Public FinnceDocument57 pagesPublic FinnceJim MathilakathuPas encore d'évaluation

- How to reduce inflation's impactsDocument42 pagesHow to reduce inflation's impactsDao Diep ThaoPas encore d'évaluation

- Philippine: Group 2Document26 pagesPhilippine: Group 2Jayvee FelipePas encore d'évaluation

- Introduction To Macroeconomics: Business Economics U52004Document31 pagesIntroduction To Macroeconomics: Business Economics U52004Vivek Mishra100% (1)

- Globalization and Global DisinflationDocument36 pagesGlobalization and Global DisinflationOkechukwu MeniruPas encore d'évaluation

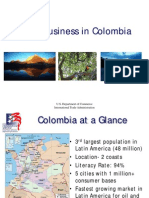

- Doing Business in Colombia September2012Document29 pagesDoing Business in Colombia September2012acmartineziiPas encore d'évaluation

- 3m ReportDocument22 pages3m Reportapi-321324040Pas encore d'évaluation

- PHPZ FB L6 WDocument5 pagesPHPZ FB L6 Wfred607Pas encore d'évaluation

- MDC China Retail Sector - Macro TrendsDocument9 pagesMDC China Retail Sector - Macro TrendsTanvi KapoorPas encore d'évaluation

- IFS (2009) Public Finances PaperDocument22 pagesIFS (2009) Public Finances PaperJoePas encore d'évaluation

- Autogrill Group - 1H2011 Financial Results: Milan, 29 July 2011Document66 pagesAutogrill Group - 1H2011 Financial Results: Milan, 29 July 2011subiadinjaraPas encore d'évaluation

- MAEC Doc FinDocument8 pagesMAEC Doc FinDivya NaikPas encore d'évaluation

- What Impact Would The Queen's Death Have On Our Economy?Document41 pagesWhat Impact Would The Queen's Death Have On Our Economy?Abhishek DebPas encore d'évaluation

- OMalley BBR 2012Document4 pagesOMalley BBR 2012Anonymous Feglbx5Pas encore d'évaluation

- The Fashion Channel Case StudyDocument4 pagesThe Fashion Channel Case StudyAnuj ChandaPas encore d'évaluation

- p130309 Brazil World CrisisDocument24 pagesp130309 Brazil World CrisisHassaan QaziPas encore d'évaluation

- Section-C, Group-7 (The Fashion Channel)Document4 pagesSection-C, Group-7 (The Fashion Channel)Aman kumar JhaPas encore d'évaluation

- Argentina: Economic Activity and EmploymentDocument4 pagesArgentina: Economic Activity and EmploymentBelen GuevaraPas encore d'évaluation

- ITC Financial Analysis and SWOT of Leading ConglomerateDocument7 pagesITC Financial Analysis and SWOT of Leading ConglomeratePrashant AminPas encore d'évaluation

- Economics AQA Section2 Workbook AnswersDocument27 pagesEconomics AQA Section2 Workbook AnswersABDULLAH KhanPas encore d'évaluation

- Economics Unit 4 Frequently Asked QuestionsDocument23 pagesEconomics Unit 4 Frequently Asked QuestionsachinthaPas encore d'évaluation

- Macroeconomics Ganesh Kumar NDocument44 pagesMacroeconomics Ganesh Kumar NHimanshu JainPas encore d'évaluation

- The Future of Export-Led Growth: A General AssessmentDocument24 pagesThe Future of Export-Led Growth: A General AssessmentSiddharth SharmaPas encore d'évaluation

- 13 International CompetitivenessDocument7 pages13 International Competitivenesssaywhat133Pas encore d'évaluation

- Fiscal Policy by DR KennethDocument51 pagesFiscal Policy by DR KennethkennyPas encore d'évaluation

- Euro Monitor International - Global Wine TrendsDocument32 pagesEuro Monitor International - Global Wine TrendsJuan Pardo100% (1)

- Global Ice Cream - Data MonitorDocument44 pagesGlobal Ice Cream - Data MonitorPrathibha Prabakaran100% (1)

- Macroeconomic Insights from Recent DataDocument44 pagesMacroeconomic Insights from Recent DataRahul AuddyPas encore d'évaluation

- AMLO - A Contract With MexicoDocument36 pagesAMLO - A Contract With MexicodespiertmexPas encore d'évaluation

- Cuba: Economic Restructuring, Recent Trends and Main ChallengesDocument14 pagesCuba: Economic Restructuring, Recent Trends and Main ChallengesRobert WileyPas encore d'évaluation

- ECON 635 Lecture Notes: Four Functions of Public FinanceDocument45 pagesECON 635 Lecture Notes: Four Functions of Public FinancetilahunthmPas encore d'évaluation

- Case 5Document4 pagesCase 5abhilashPas encore d'évaluation

- Econ1102 Week 6Document53 pagesEcon1102 Week 6AAA820Pas encore d'évaluation

- A1 11-Asm1-Mac 2Document36 pagesA1 11-Asm1-Mac 2Hai Giang DucPas encore d'évaluation

- Bản Sao BT-phân-tích-kinh-tế-vinamilkDocument5 pagesBản Sao BT-phân-tích-kinh-tế-vinamilkPhạm Thị Ngọc DungPas encore d'évaluation

- EY Focus On The Trinidad and Tobago Budget 2018Document50 pagesEY Focus On The Trinidad and Tobago Budget 2018rose_kissme96Pas encore d'évaluation

- Presentation About Chamber of Industry CalzadoDocument21 pagesPresentation About Chamber of Industry CalzadoFrancisco Prado BarraganPas encore d'évaluation

- 2281 w03 QP 1Document16 pages2281 w03 QP 1mstudy1234560% (1)

- GDP Growth RatesDocument12 pagesGDP Growth RatesAllauddinaghaPas encore d'évaluation

- As Economics Unit 2 Macroeconomic Performance Lesson 2Document21 pagesAs Economics Unit 2 Macroeconomic Performance Lesson 2api-53255207Pas encore d'évaluation

- Economic Slowdown and Macro Economic PoliciesDocument38 pagesEconomic Slowdown and Macro Economic PoliciesRachitaRattanPas encore d'évaluation

- 2281 w05 QP 1Document12 pages2281 w05 QP 1mstudy123456Pas encore d'évaluation

- Module 5: Indian Economy: 5.1 Main Features of Indian Economy and Major Issues of DevelopmentDocument22 pagesModule 5: Indian Economy: 5.1 Main Features of Indian Economy and Major Issues of DevelopmentAnonymous nTxB1EPvPas encore d'évaluation

- Comparing the economies of France and UAEDocument16 pagesComparing the economies of France and UAEuowdubaiPas encore d'évaluation

- Principles of Economics - Part BDocument5 pagesPrinciples of Economics - Part BCarol HelenPas encore d'évaluation

- Macronia Country CaseDocument3 pagesMacronia Country CaseDahagam SaumithPas encore d'évaluation

- Quality ManagementDocument22 pagesQuality ManagementChizunyashaPas encore d'évaluation

- 1 National Income AccountingDocument18 pages1 National Income Accountingsatriana_ekaPas encore d'évaluation

- Conference CallDocument15 pagesConference CallLightRIPas encore d'évaluation

- Keats April 21 2011Document31 pagesKeats April 21 2011Sanjay JagatsinghPas encore d'évaluation

- Economy of ColombiaDocument13 pagesEconomy of Colombia28_himanshu_1987Pas encore d'évaluation

- Economic Growth (1st Part)Document58 pagesEconomic Growth (1st Part)LilaPas encore d'évaluation

- 3M - 2010 - 3Q Press ReleaseDocument16 pages3M - 2010 - 3Q Press ReleaseallisonmurphyPas encore d'évaluation

- Macro Sessions 13-15Document123 pagesMacro Sessions 13-15Sawan AcharyPas encore d'évaluation

- Assignment ADocument6 pagesAssignment Acary_puyatPas encore d'évaluation

- Analysis of Musharraf Era 1999-2008Document37 pagesAnalysis of Musharraf Era 1999-2008Bushra NaumanPas encore d'évaluation

- Business Economics: Business Strategy & Competitive AdvantageD'EverandBusiness Economics: Business Strategy & Competitive AdvantagePas encore d'évaluation

- Trading Economics: A Guide to Economic Statistics for Practitioners and StudentsD'EverandTrading Economics: A Guide to Economic Statistics for Practitioners and StudentsPas encore d'évaluation

- Revised Admission ScheduleDocument1 pageRevised Admission SchedulePatrick AdamsPas encore d'évaluation

- DONE - Mahatma Gandhi Kashi Vidyapith, VaranasiDocument1 pageDONE - Mahatma Gandhi Kashi Vidyapith, VaranasiPatrick AdamsPas encore d'évaluation

- Done - List of Mentors Pa Da Institution WiseDocument1 pageDone - List of Mentors Pa Da Institution WisePatrick AdamsPas encore d'évaluation

- Theories of Punishments - LLB I YEARDocument12 pagesTheories of Punishments - LLB I YEARNaveen Kumar0% (1)

- LL.B. (I, II & III Year) : Chaudhary Charan Singh University, MeerutDocument1 pageLL.B. (I, II & III Year) : Chaudhary Charan Singh University, Meerutdevthakur_mbaPas encore d'évaluation

- DONE Exams NewsPaperDocument1 pageDONE Exams NewsPaperPatrick AdamsPas encore d'évaluation

- Most Recent US Arrival Date and in What StatusDocument2 pagesMost Recent US Arrival Date and in What StatusPatrick AdamsPas encore d'évaluation

- I Year LLB Exame Note For Constitution of IndiaDocument13 pagesI Year LLB Exame Note For Constitution of IndiaNaveen Kumar88% (33)

- MOP Final List of 32 Energy Consulting FirmsDocument9 pagesMOP Final List of 32 Energy Consulting FirmsPatrick AdamsPas encore d'évaluation

- Education Secretaries 10Document6 pagesEducation Secretaries 10Patrick AdamsPas encore d'évaluation

- Contract-I and Specific Relief ActDocument31 pagesContract-I and Specific Relief ActNaveen Kumar77% (22)

- INDIVIDUAL CUSTOMER's Account DetailsDocument36 pagesINDIVIDUAL CUSTOMER's Account DetailsPatrick AdamsPas encore d'évaluation

- Mhcci ListDocument1 074 pagesMhcci ListShaiwal Parashar57% (7)

- List of Network HospitalDocument80 pagesList of Network HospitalPatrick AdamsPas encore d'évaluation

- Done - Keonics Centre AddressDocument44 pagesDone - Keonics Centre AddressPatrick AdamsPas encore d'évaluation

- FrescoDocument106 pagesFrescoPatrick Adams100% (1)

- Delhi CBSE School Website and AddressDocument153 pagesDelhi CBSE School Website and AddressPatrick AdamsPas encore d'évaluation

- XAT 2014 SECTION C List of XAT Associate Member InstitutesDocument8 pagesXAT 2014 SECTION C List of XAT Associate Member InstitutesPatrick AdamsPas encore d'évaluation

- MbaDocument20 pagesMbaPatrick AdamsPas encore d'évaluation

- Crest ViewDocument69 pagesCrest ViewPatrick Adams67% (3)

- Customer List for Escape ProjectDocument9 pagesCustomer List for Escape ProjectPatrick AdamsPas encore d'évaluation

- Untitled 1Document230 pagesUntitled 1Sakunthala MuthuPas encore d'évaluation

- Contact List with AddressesDocument27 pagesContact List with AddressesPatrick AdamsPas encore d'évaluation

- ExquisiteDocument20 pagesExquisitePatrick Adams50% (2)

- Gardens IIDocument114 pagesGardens IIPatrick Adams0% (1)

- ResidencesDocument252 pagesResidencesPatrick Adams75% (16)

- BHEL Directory 2011Document128 pagesBHEL Directory 2011Ashok Kumar Meena100% (2)

- Delhi CBSE School Website and AddressDocument153 pagesDelhi CBSE School Website and AddressPatrick AdamsPas encore d'évaluation

- VSNDocument7 pagesVSNPatrick AdamsPas encore d'évaluation

- Alder GroveDocument45 pagesAlder GrovePatrick Adams75% (8)

- BIR Form 1700 - Income Tax Return FilingDocument1 pageBIR Form 1700 - Income Tax Return FilingMarriz Bustaliño TanPas encore d'évaluation

- NINJA Book Reg 1 EthicsDocument38 pagesNINJA Book Reg 1 EthicsJaffery143Pas encore d'évaluation

- All Contributions Noon 23Document23 pagesAll Contributions Noon 23Alexandria ShahabianPas encore d'évaluation

- SIM 337 ExxonMobilDocument13 pagesSIM 337 ExxonMobilHai Viet TrieuPas encore d'évaluation

- q22023 Macro-Outlook PortalDocument14 pagesq22023 Macro-Outlook PortalM. Fatah YasinPas encore d'évaluation

- f1040 2018 PDFDocument3 pagesf1040 2018 PDFSara HeadrickPas encore d'évaluation

- Roboforex StatementsDocument50 pagesRoboforex StatementsCarlosPas encore d'évaluation

- fs138 LiheapDocument3 pagesfs138 LiheapjspectorPas encore d'évaluation

- 2009 Tax Table 1040 1040NR For H1B, F1, J1, OPTDocument13 pages2009 Tax Table 1040 1040NR For H1B, F1, J1, OPTusvisataxesPas encore d'évaluation

- Wa0000.Document1 pageWa0000.tkduong889Pas encore d'évaluation

- Stock TickersDocument4 pagesStock TickerssmineshvPas encore d'évaluation

- Week 7 1 LookupsDocument18 pagesWeek 7 1 LookupsBəhmən OrucovPas encore d'évaluation

- CP575Notice 1605020544606Document2 pagesCP575Notice 1605020544606SMOOVE STOP PLAYIN RECORDSPas encore d'évaluation

- Bloomberg Businessweek 29.01.2024Document68 pagesBloomberg Businessweek 29.01.2024Nataraju NandihalliPas encore d'évaluation

- Individual Tax Returns - IRS 2009Document200 pagesIndividual Tax Returns - IRS 2009Steve EldridgePas encore d'évaluation

- r390 Production SummaryDocument2 pagesr390 Production SummarydulePas encore d'évaluation

- Non-Negotiable: 1033 Massachusetts Avenue 2nd Floor Cambridge, MA 02138Document1 pageNon-Negotiable: 1033 Massachusetts Avenue 2nd Floor Cambridge, MA 02138DearNoodlesPas encore d'évaluation

- FafsaDocument5 pagesFafsaCitystaticPas encore d'évaluation

- Schedule IN-119 Instructions Vermont Tax Adjustments and Nonrefundable Credits Line-by-Line InstructionsDocument4 pagesSchedule IN-119 Instructions Vermont Tax Adjustments and Nonrefundable Credits Line-by-Line Instructionsjim deeznutzPas encore d'évaluation

- The Politics of Mathematics Education in The US: Dominant and Counter Agendas Eric GutsteinDocument45 pagesThe Politics of Mathematics Education in The US: Dominant and Counter Agendas Eric Gutsteindavisfc50Pas encore d'évaluation

- Intrinsic Value Calculation Formula Sven CarlinDocument262 pagesIntrinsic Value Calculation Formula Sven CarlinMohamed Ali AmaraPas encore d'évaluation

- Application For Property Tax Reduction For 2017: L L L L L LDocument1 pageApplication For Property Tax Reduction For 2017: L L L L L LO'Connor AssociatePas encore d'évaluation

- Financial Coaching Business Plan TemplateDocument21 pagesFinancial Coaching Business Plan TemplatesolomonPas encore d'évaluation

- IEEE STD 1243-1997 - Lightning Performance For Trasnmission LinesDocument45 pagesIEEE STD 1243-1997 - Lightning Performance For Trasnmission LinesmilagrosPas encore d'évaluation

- The Revisionist - Journal For Critical Historical Inquiry - Volume 1 - Number 2 (En, 2003, 124 S., Text)Document124 pagesThe Revisionist - Journal For Critical Historical Inquiry - Volume 1 - Number 2 (En, 2003, 124 S., Text)hjuinixPas encore d'évaluation

- Vishay Library Components ListDocument55 pagesVishay Library Components ListCristian Alejandro Ayon TzintzunPas encore d'évaluation

- U.S. Individual Income Tax Return: John Public 0 0 0 0 0 0 0 0 0 Jane Public 0 0 0 0 0 0 0 0 1Document2 pagesU.S. Individual Income Tax Return: John Public 0 0 0 0 0 0 0 0 0 Jane Public 0 0 0 0 0 0 0 0 1Renee Leon100% (1)

- Matching Cost Against RevenueDocument1 pageMatching Cost Against Revenuejuliet_emelinotmaestroPas encore d'évaluation

- FOX & FRIENDS FIRST Advertising LogDocument25 pagesFOX & FRIENDS FIRST Advertising LogPrashant JhaPas encore d'évaluation

- CS Socialscience SMRDocument16 pagesCS Socialscience SMR_sumscribdPas encore d'évaluation