Vous aimerez peut-être aussi

- Income From BusinessDocument40 pagesIncome From BusinessSaqib MughalPas encore d'évaluation

- Financial StatementDocument15 pagesFinancial StatementPankaj SharmaPas encore d'évaluation

- Indirect Taxes-May 2011: FIRST OF ALL Read CarefullyDocument8 pagesIndirect Taxes-May 2011: FIRST OF ALL Read Carefully9811702789Pas encore d'évaluation

- EContent 3 2024 02 28 06 43 20 CAPITALGAINdocx 2024 02 20 11 29 41Document22 pagesEContent 3 2024 02 28 06 43 20 CAPITALGAINdocx 2024 02 20 11 29 41solanki YashPas encore d'évaluation

- Assignment CMA Nalanda 2016Document3 pagesAssignment CMA Nalanda 2016NishaTripathiPas encore d'évaluation

- Sales Tax Practice Questions With SolutionsDocument6 pagesSales Tax Practice Questions With Solutionshanif channa100% (1)

- Lecture 1 Sales TaxDocument42 pagesLecture 1 Sales TaxYanPing AngPas encore d'évaluation

- 3..sales Tax ProvisionsDocument82 pages3..sales Tax ProvisionsUmair GOLDPas encore d'évaluation

- Bba 2Document119 pagesBba 2Rajan SinghPas encore d'évaluation

- Loyola College (Autonomous), Chennai - 600 034.: First Semester - Nov 2005Document4 pagesLoyola College (Autonomous), Chennai - 600 034.: First Semester - Nov 2005Charles VinothPas encore d'évaluation

- Accounting Dec 2010Document2 pagesAccounting Dec 2010Faizal JohnPas encore d'évaluation

- 14 BBTX4203 T10Document23 pages14 BBTX4203 T10puvillanPas encore d'évaluation

- Taxation Pac Mock s13 PDFDocument3 pagesTaxation Pac Mock s13 PDFMuhammad Hassan AliPas encore d'évaluation

- Ms 4Document2 pagesMs 4Dickie SangmaPas encore d'évaluation

- Basic Accounting TermsDocument9 pagesBasic Accounting TermsPuru GuptaPas encore d'évaluation

- Final Acc-Numerical 1Document10 pagesFinal Acc-Numerical 1Rajshree BhardwajPas encore d'évaluation

- Bba 2012Document134 pagesBba 2012gbulani11Pas encore d'évaluation

- Test 1 QP Sir FRK CAME PREDocument3 pagesTest 1 QP Sir FRK CAME PREUmair GOLDPas encore d'évaluation

- Accounting and FinanceDocument14 pagesAccounting and FinanceJapjiv SinghPas encore d'évaluation

- FM12 Financial Management: Assignment No.IDocument3 pagesFM12 Financial Management: Assignment No.ISrajan KharePas encore d'évaluation

- A Overview of Maharashtra Value Added Tax: IndexDocument10 pagesA Overview of Maharashtra Value Added Tax: IndexAdnan ParkarPas encore d'évaluation

- B203B-Week 6 - (Accounting-3) Updated 31-10Document38 pagesB203B-Week 6 - (Accounting-3) Updated 31-10ahmed helmyPas encore d'évaluation

- Numerical SDocument11 pagesNumerical Sbarnwal_bikashPas encore d'évaluation

- Entrepreneurship DevelopmentDocument21 pagesEntrepreneurship DevelopmentAnkush YedaviPas encore d'évaluation

- MB0041 Financial and Management AccountingDocument12 pagesMB0041 Financial and Management AccountingDivyang Panchasara0% (2)

- Practice Questions - 08-06-2023Document2 pagesPractice Questions - 08-06-2023MUHAMMAD AHMEDPas encore d'évaluation

- Notes On Sales TaxDocument24 pagesNotes On Sales Taxsajjad_ym1100% (7)

- VAT MathDocument3 pagesVAT Mathtisha10rahman50% (4)

- AccountDocument2 pagesAccountnomaanahmadshahPas encore d'évaluation

- Business TaxationDocument3 pagesBusiness TaxationHannan UmerPas encore d'évaluation

- Tnvat Form WW Fy 15-16Document30 pagesTnvat Form WW Fy 15-16samaadhuPas encore d'évaluation

- Practice Paper: Section "A" (Multiple Choice Questions) (20 Marks)Document3 pagesPractice Paper: Section "A" (Multiple Choice Questions) (20 Marks)Sameer Hussain100% (1)

- Ca FinalDocument11 pagesCa FinalHadia HPas encore d'évaluation

- SAMPLE PAPER - (Solved) : For Examination March 2017Document13 pagesSAMPLE PAPER - (Solved) : For Examination March 2017ankush yadavPas encore d'évaluation

- 53 Summary On Vat CST and WCTDocument16 pages53 Summary On Vat CST and WCTYogesh DeokarPas encore d'évaluation

- 11 La 402 BTDocument4 pages11 La 402 BTmuhzahid786Pas encore d'évaluation

- Chapter 3. Corporate Income TaxDocument90 pagesChapter 3. Corporate Income TaxVu Thi ThuongPas encore d'évaluation

- December 2002 ACCA Paper 2.5 QuestionsDocument11 pagesDecember 2002 ACCA Paper 2.5 QuestionsUlanda2Pas encore d'évaluation

- Questions & Solutions ACCTDocument246 pagesQuestions & Solutions ACCTMel Lissa33% (3)

- Approximately of 400 Words. Each Question Is Followed by Evaluation SchemeDocument2 pagesApproximately of 400 Words. Each Question Is Followed by Evaluation SchemeBadder DanbadPas encore d'évaluation

- Model Question Set 1Document2 pagesModel Question Set 1Destiny Tuition CentrePas encore d'évaluation

- CIN Overview: Accenture, Its Logo, and Accenture High Performance Delivered Are Trademarks of AccentureDocument24 pagesCIN Overview: Accenture, Its Logo, and Accenture High Performance Delivered Are Trademarks of AccenturecharanPas encore d'évaluation

- Central Sales Tax: BY Anil V Mcom 14PG01001Document12 pagesCentral Sales Tax: BY Anil V Mcom 14PG01001Anil vPas encore d'évaluation

- Click Here To View Interest RatesDocument13 pagesClick Here To View Interest RatesGunjan ShahPas encore d'évaluation

- KTTC1Document22 pagesKTTC1Trần Khánh VyPas encore d'évaluation

- VAT Week 2 and 3Document25 pagesVAT Week 2 and 3Ma.annPas encore d'évaluation

- Examination Paper-2010Document5 pagesExamination Paper-2010api-248768984Pas encore d'évaluation

- VAT GuideZRADocument56 pagesVAT GuideZRADaniel Glen-WilliamsonPas encore d'évaluation

- BBADocument138 pagesBBAAbhishek AgarwalPas encore d'évaluation

- Practice QuestionsDocument4 pagesPractice QuestionsMff DeadsparkPas encore d'évaluation

- If, Cost of Machine Rs.400, 000 Useful Life 5 Years Rate of Depreciation 40%Document13 pagesIf, Cost of Machine Rs.400, 000 Useful Life 5 Years Rate of Depreciation 40%Narang NewsPas encore d'évaluation

- ILLustrationsDocument23 pagesILLustrationsiframahmood026Pas encore d'évaluation

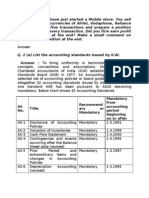

- Recommend Ary or Mandatory Mandatory From Accounting Period Beginning On or AfterDocument7 pagesRecommend Ary or Mandatory Mandatory From Accounting Period Beginning On or AfterdnbiswasPas encore d'évaluation

- Centeral Sales TaxDocument22 pagesCenteral Sales Taxrajivnair90Pas encore d'évaluation

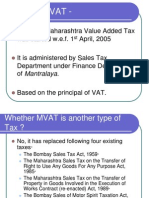

- A Brief Introduction of MVAT - : by Chinmay GangwalDocument28 pagesA Brief Introduction of MVAT - : by Chinmay GangwalAmolaPas encore d'évaluation

- Investment Banking: Valuation, Leveraged Buyouts, and Mergers and AcquisitionsD'EverandInvestment Banking: Valuation, Leveraged Buyouts, and Mergers and AcquisitionsÉvaluation : 5 sur 5 étoiles5/5 (2)

- SECURITIES INDUSTRY ESSENTIALS EXAM STUDY GUIDE 2023 + TEST BANKD'EverandSECURITIES INDUSTRY ESSENTIALS EXAM STUDY GUIDE 2023 + TEST BANKPas encore d'évaluation

- Fast-Track Tax Reform: Lessons from the MaldivesD'EverandFast-Track Tax Reform: Lessons from the MaldivesPas encore d'évaluation

- Mergers & Acquisitions: Crushing It as a Corporate Buyer in the Middle MarketD'EverandMergers & Acquisitions: Crushing It as a Corporate Buyer in the Middle MarketÉvaluation : 1 sur 5 étoiles1/5 (1)

- University of Mumbai RM Sem 4Document5 pagesUniversity of Mumbai RM Sem 4Deepika KalimuthuPas encore d'évaluation

- Final Projact of Cost ButgetDocument35 pagesFinal Projact of Cost ButgetDeepika KalimuthuPas encore d'évaluation

- Maharashtra Value Added Taxact, 2002 (Mvat) : Basic Concepts: Vivek College of CommerceDocument35 pagesMaharashtra Value Added Taxact, 2002 (Mvat) : Basic Concepts: Vivek College of CommerceDeepika KalimuthuPas encore d'évaluation

- Financial 1Document41 pagesFinancial 1Deepika KalimuthuPas encore d'évaluation

- University of Mumbai RM Sem 4Document5 pagesUniversity of Mumbai RM Sem 4Deepika KalimuthuPas encore d'évaluation

- Wipro's Audit Repo Add IntroDocument33 pagesWipro's Audit Repo Add IntroDeepika KalimuthuPas encore d'évaluation

- Projectonshampoo 101107134213 Phpapp01 DeepikaDocument30 pagesProjectonshampoo 101107134213 Phpapp01 DeepikaDeepika KalimuthuPas encore d'évaluation

- 634357469811641250Document23 pages634357469811641250Deepika KalimuthuPas encore d'évaluation

- FM Ratio ProjectDocument39 pagesFM Ratio ProjectDeepika KalimuthuPas encore d'évaluation

- Consumer Behaviour Towards Shampoos: Vivek College of CommersDocument37 pagesConsumer Behaviour Towards Shampoos: Vivek College of CommersDeepika KalimuthuPas encore d'évaluation

- Projectonshampoo 101107134213 Phpapp01 DeepikaDocument30 pagesProjectonshampoo 101107134213 Phpapp01 DeepikaDeepika KalimuthuPas encore d'évaluation

- Business Strategy For ITC LTDDocument32 pagesBusiness Strategy For ITC LTDDeepika KalimuthuPas encore d'évaluation

- Deepika ShampooDocument8 pagesDeepika ShampooThilaga Senthilmurugan100% (1)

- FM Ratio ProjectDocument39 pagesFM Ratio ProjectDeepika KalimuthuPas encore d'évaluation

- Finance PROJECT REPORT ON "COMPARATIVE STUDY OF TOP THREE BANKS OF INDIA"Document32 pagesFinance PROJECT REPORT ON "COMPARATIVE STUDY OF TOP THREE BANKS OF INDIA"Deepika KalimuthuPas encore d'évaluation

- Consumer Behaviour: Business PurposeDocument30 pagesConsumer Behaviour: Business PurposeDeepika KalimuthuPas encore d'évaluation

- Salary IncomeDocument8 pagesSalary IncomeAshis karmakarPas encore d'évaluation

- AccDocument35 pagesAccDeepika KalimuthuPas encore d'évaluation

- Tax ProDocument34 pagesTax ProDeepika KalimuthuPas encore d'évaluation

- 1Document1 page1Deepika KalimuthuPas encore d'évaluation

- UNIT II Tax RemediesDocument17 pagesUNIT II Tax RemediesAl BertPas encore d'évaluation

- Mary Florence D. Yap - Tax DigestsDocument16 pagesMary Florence D. Yap - Tax Digestsowl2019Pas encore d'évaluation

- Tax LawDocument3 pagesTax LawAnkit KumarPas encore d'évaluation

- National Income - Definitions - Lovish KakkarDocument2 pagesNational Income - Definitions - Lovish KakkarAjuni ShahPas encore d'évaluation

- BIR Form 1800 Donor's Tax ReturnDocument3 pagesBIR Form 1800 Donor's Tax ReturnHailin QuintosPas encore d'évaluation

- Bank Credit Card Usage Behavior of Individuals Are Credit Cards Considered As Status Symbols or Are They Really Threats To Consumers Budgets? A Field Study From Eskisehir, TurkeyDocument23 pagesBank Credit Card Usage Behavior of Individuals Are Credit Cards Considered As Status Symbols or Are They Really Threats To Consumers Budgets? A Field Study From Eskisehir, TurkeyMd Sakawat HossainPas encore d'évaluation

- Unit 4 Payment Systems PDFDocument48 pagesUnit 4 Payment Systems PDFmuskanPas encore d'évaluation

- Od 226140729696188000Document1 pageOd 226140729696188000abhinaygvsPas encore d'évaluation

- CCIT Module 2 - TAXES, TAX LAWS and TAX ADMINISTRATIONDocument15 pagesCCIT Module 2 - TAXES, TAX LAWS and TAX ADMINISTRATIONAngelo OñedoPas encore d'évaluation

- Annexure To Foreign ExchangeDocument2 pagesAnnexure To Foreign ExchangeAman DhootPas encore d'évaluation

- Application Form M3M IFCDocument38 pagesApplication Form M3M IFCDashmesh LandbasePas encore d'évaluation

- TestDocument4 pagesTestjasim khanPas encore d'évaluation

- CIR v. American Express International G.R. No. 152609, June 29, 2005Document2 pagesCIR v. American Express International G.R. No. 152609, June 29, 2005Susannie AcainPas encore d'évaluation

- Engineering Economic Analysis 11thDocument2 pagesEngineering Economic Analysis 11thJesus DunnPas encore d'évaluation

- Self-Assessment Questionnaire B: and Attestation of ComplianceDocument20 pagesSelf-Assessment Questionnaire B: and Attestation of Compliancemustafaanis786Pas encore d'évaluation

- Oasis Golf Club PDFDocument2 pagesOasis Golf Club PDFAtif JaveadPas encore d'évaluation

- ACT26 Ch05 Net-Taxable-EstateDocument7 pagesACT26 Ch05 Net-Taxable-EstateMark BajacanPas encore d'évaluation

- Vendor CA 587 - Non-ResidentDocument3 pagesVendor CA 587 - Non-ResidentЛена КиселеваPas encore d'évaluation

- Ads 2223 485683 PDFDocument3 pagesAds 2223 485683 PDFHarsh PatelPas encore d'évaluation

- Tax InterviewDocument1 pageTax InterviewGhayur HaiderPas encore d'évaluation

- Silkair (Singapore) Pte, LTD vs. CirDocument2 pagesSilkair (Singapore) Pte, LTD vs. CirMarylou Macapagal100% (2)

- Payment & Settlement SystemsDocument8 pagesPayment & Settlement SystemsAnshu GuptaPas encore d'évaluation

- Order Confirmation-OC3309Document1 pageOrder Confirmation-OC3309Chetan patilPas encore d'évaluation

- Utah Form TC-20 Tax Return and InstructionsDocument26 pagesUtah Form TC-20 Tax Return and InstructionsBrandonPas encore d'évaluation

- Answer Key On Comprehensive ExerciseDocument13 pagesAnswer Key On Comprehensive ExerciseErickaPas encore d'évaluation

- Prelim Examination Business TaxDocument16 pagesPrelim Examination Business Taxmikheal beyberPas encore d'évaluation

- Invoice: Payment Your SWIFT InvoiceDocument4 pagesInvoice: Payment Your SWIFT InvoiceClément MinougouPas encore d'évaluation

- Week 10 - Leasing (Part 1)Document1 pageWeek 10 - Leasing (Part 1)Vidya IntaniPas encore d'évaluation

- Proforma InvoiceDocument3 pagesProforma InvoiceSuresh KumarPas encore d'évaluation

- Shopping Vocabulary Esl Missing Letters in Words Worksheets For KidsDocument4 pagesShopping Vocabulary Esl Missing Letters in Words Worksheets For KidsKatrin PoluliakhPas encore d'évaluation