Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Auditing Theory Answer Key (2011) by Salosagcol, Tiu, and HermosillaDocument1 pageAuditing Theory Answer Key (2011) by Salosagcol, Tiu, and HermosillaRJ Diana0% (1)

- SC Licensing HandbookDocument75 pagesSC Licensing HandbookYff DickPas encore d'évaluation

- Month Day Month Day: 526-1212, Extension 2403 / 8231-10-73 (Temporary)Document209 pagesMonth Day Month Day: 526-1212, Extension 2403 / 8231-10-73 (Temporary)Ivan ChiuPas encore d'évaluation

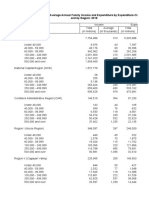

- Table 3 Total and Average Annual Family Income and Expenditure by Expenditure Class and by Region 2018Document8 pagesTable 3 Total and Average Annual Family Income and Expenditure by Expenditure Class and by Region 2018Ivan ChiuPas encore d'évaluation

- ABA - Annual Report 2017Document128 pagesABA - Annual Report 2017Ivan ChiuPas encore d'évaluation

- ABA - Annual Report 2018Document146 pagesABA - Annual Report 2018Ivan ChiuPas encore d'évaluation

- Table 2 Total and Average Annual Family Income and Expenditure by Income Class and by Region 2018Document8 pagesTable 2 Total and Average Annual Family Income and Expenditure by Income Class and by Region 2018Glenn GalvezPas encore d'évaluation

- Table 1 Number of Families, Total and Average Annual Family Income and Expenditure by Region 2018Document2 pagesTable 1 Number of Families, Total and Average Annual Family Income and Expenditure by Region 2018Ivan ChiuPas encore d'évaluation

- ABA - Annual Report 2019Document169 pagesABA - Annual Report 2019Ivan ChiuPas encore d'évaluation

- Table 7 Mean and Median Family Income and Expenditure by Per Capita Income Decile and by Region, 2018Document16 pagesTable 7 Mean and Median Family Income and Expenditure by Per Capita Income Decile and by Region, 2018Ivan ChiuPas encore d'évaluation

- 7 - BibliographyDocument4 pages7 - BibliographyIvan ChiuPas encore d'évaluation

- 6 - Summary, Conclusion and RecommendationDocument3 pages6 - Summary, Conclusion and RecommendationIvan ChiuPas encore d'évaluation

- 4 - MethodologyDocument6 pages4 - MethodologyIvan ChiuPas encore d'évaluation

- Table 5 Average Annual Family Income and Expenditure by Family Size, by Income Class and by Region, 2018Document10 pagesTable 5 Average Annual Family Income and Expenditure by Family Size, by Income Class and by Region, 2018Ivan ChiuPas encore d'évaluation

- 3 - Conceptual FrameworkDocument3 pages3 - Conceptual FrameworkIvan ChiuPas encore d'évaluation

- 5 - Results and DiscussionDocument5 pages5 - Results and DiscussionIvan ChiuPas encore d'évaluation

- Briefing On RA 10963: Tax Reform For Acceleration and Inclusion (TRAIN) - Power andDocument4 pagesBriefing On RA 10963: Tax Reform For Acceleration and Inclusion (TRAIN) - Power andIvan ChiuPas encore d'évaluation

- The Treasury Nominal Coupon-Issue (TNC) Yield Curve: 10-Year Average Spot Rates, PercentDocument9 pagesThe Treasury Nominal Coupon-Issue (TNC) Yield Curve: 10-Year Average Spot Rates, PercentIvan ChiuPas encore d'évaluation

- Bscs Se v2011 PDFDocument3 pagesBscs Se v2011 PDFBobPas encore d'évaluation

- Bachelor of Science in Computer ScienceDocument3 pagesBachelor of Science in Computer ScienceIvan ChiuPas encore d'évaluation

- Accounting For Branches and Combined FSDocument112 pagesAccounting For Branches and Combined FSMuhammad Fahad100% (2)

- 47.taxability of Productivity Incentive Bonuses.07.10.08.GACDocument2 pages47.taxability of Productivity Incentive Bonuses.07.10.08.GACEumell Alexis PalePas encore d'évaluation

- Operating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerDocument1 pageOperating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerIvan ChiuPas encore d'évaluation

- CSC 121Document8 pagesCSC 121Ivan ChiuPas encore d'évaluation

- Audit Internal ExternalDocument1 pageAudit Internal ExternalIvan ChiuPas encore d'évaluation

- Critique of Comtemporary Philippine FilmsDocument1 pageCritique of Comtemporary Philippine FilmsIvan ChiuPas encore d'évaluation

- CIMA ScenarioDocument10 pagesCIMA ScenarioPerfectionism FollowerPas encore d'évaluation

- Salosagcol Audit Theory Is The Mean Way To Financial Statement But Black Scholes Is The BestDocument1 pageSalosagcol Audit Theory Is The Mean Way To Financial Statement But Black Scholes Is The BestIvan ChiuPas encore d'évaluation

- Operating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerDocument1 pageOperating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerIvan ChiuPas encore d'évaluation

- Power of The MassesDocument1 pagePower of The MassesIvan ChiuPas encore d'évaluation

- It's Not About The Thing That Cats and Mouse Are Not in Harmony With Each Other. Alan Peter. and Cuaderno EstebanDocument1 pageIt's Not About The Thing That Cats and Mouse Are Not in Harmony With Each Other. Alan Peter. and Cuaderno EstebanIvan ChiuPas encore d'évaluation

- Block 1 The Digital World: TM111 Introduction To Computing and Information Technology 1Document328 pagesBlock 1 The Digital World: TM111 Introduction To Computing and Information Technology 1lamarosafranciscoPas encore d'évaluation

- Marc FaberDocument20 pagesMarc Faberapi-26094277Pas encore d'évaluation

- Management Term Paper On Al Arafah Bank's HR Practice Term PaperDocument25 pagesManagement Term Paper On Al Arafah Bank's HR Practice Term Paperratulbinmuzib100% (3)

- NRIHome Loan FormDocument4 pagesNRIHome Loan FormnirajmishraPas encore d'évaluation

- CURT-ALLEN: of The Family Byron V LOVICK, Et Al. - 1 - Complaint - Gov - Uscourts.wawd.166908.1.0Document7 pagesCURT-ALLEN: of The Family Byron V LOVICK, Et Al. - 1 - Complaint - Gov - Uscourts.wawd.166908.1.0Jack RyanPas encore d'évaluation

- Ipo OrderDocument252 pagesIpo Orderapi-3701467Pas encore d'évaluation

- Facts and Figures: DZ BANK in The Cooperative Financial NetworkDocument3 pagesFacts and Figures: DZ BANK in The Cooperative Financial NetworkDiego BrandeauPas encore d'évaluation

- Lakshmi RavindranDocument41 pagesLakshmi RavindranspcbankingPas encore d'évaluation

- Final Marchant BankingDocument42 pagesFinal Marchant BankingSupriya PatekarPas encore d'évaluation

- Bir Form 1600Document44 pagesBir Form 1600Jerel John CalanaoPas encore d'évaluation

- SYBMS Sem 3 SyllabusDocument7 pagesSYBMS Sem 3 SyllabusRavi KrishnanPas encore d'évaluation

- Credit SaraswatDocument77 pagesCredit Saraswatsahil1508Pas encore d'évaluation

- Leadership in Banking Presentation - Idris YakubuDocument37 pagesLeadership in Banking Presentation - Idris YakubuArindam BanerjeePas encore d'évaluation

- Director Structured Finance Credit in NYC Resume Mark DouglassDocument3 pagesDirector Structured Finance Credit in NYC Resume Mark DouglassMarkDouglassPas encore d'évaluation

- Monthly Portfolio Aug 18Document126 pagesMonthly Portfolio Aug 18Jennifer NievesPas encore d'évaluation

- Chit Fund CompanyDocument34 pagesChit Fund CompanyPARAS JAINPas encore d'évaluation

- Chapter 6. Prohibited Transactions (Enzo)Document14 pagesChapter 6. Prohibited Transactions (Enzo)Kyle DionisioPas encore d'évaluation

- Literature Review of Kotak Mahindra BankDocument6 pagesLiterature Review of Kotak Mahindra Bankc5p64m3t100% (1)

- Office Manuals - IXDocument8 pagesOffice Manuals - IXDileepoo7Pas encore d'évaluation

- Loan Application Form of DMI Housing Finance Pvt. Ltd.Document4 pagesLoan Application Form of DMI Housing Finance Pvt. Ltd.DMI HousingPas encore d'évaluation

- Exchange Control - Foreign Exchange Bureaux de Change - OrdeDocument9 pagesExchange Control - Foreign Exchange Bureaux de Change - OrdeKelvin RugonyePas encore d'évaluation

- Suhl Annual Report 2021 - FinalDocument226 pagesSuhl Annual Report 2021 - FinalDavis ManPas encore d'évaluation

- Bright Evans - Curriculum VitaeDocument4 pagesBright Evans - Curriculum VitaeFREDRICK MUSAWOPas encore d'évaluation

- Growth of Islamic Banking in PakistanDocument79 pagesGrowth of Islamic Banking in Pakistandawar33100% (1)

- Fundamentals of Economics and Financial MarketsDocument4 pagesFundamentals of Economics and Financial MarketsluluPas encore d'évaluation

- Evening Brach in Co Operative BankDocument28 pagesEvening Brach in Co Operative BankGreatway ServicesPas encore d'évaluation

- EmploymentFair14Booklet PDFDocument163 pagesEmploymentFair14Booklet PDFMoatasemMadianPas encore d'évaluation

- Santa-Ana Jerald Accounting For Cash Cash and Cash EquivalentsDocument11 pagesSanta-Ana Jerald Accounting For Cash Cash and Cash EquivalentsSanta-ana Jerald JuanoPas encore d'évaluation

- Regulation of The AuditorDocument20 pagesRegulation of The AuditorPhebieon MukwenhaPas encore d'évaluation