Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Principles of Economics 10Th Edition Case Test Bank Full Chapter PDFDocument52 pagesPrinciples of Economics 10Th Edition Case Test Bank Full Chapter PDFmirabeltuyenwzp6f100% (8)

- Managerial Economics Syllabus GuideDocument30 pagesManagerial Economics Syllabus GuideAnonymous d3CGBMzPas encore d'évaluation

- Formula Sheet For IntermacroDocument6 pagesFormula Sheet For IntermacroHazirahPas encore d'évaluation

- Mind Map Money and CreditDocument1 pageMind Map Money and CreditMoin Ahmed100% (3)

- Central Banking & Monetary Policy SyllabusDocument3 pagesCentral Banking & Monetary Policy SyllabusCielo ObriquePas encore d'évaluation

- M12 Bade 9418 04 Ch10aDocument16 pagesM12 Bade 9418 04 Ch10aVanny Van Sneidjer100% (2)

- Corporate PlanningDocument22 pagesCorporate PlanningYumna HashmiPas encore d'évaluation

- SCDL Macroeconomics QuestionsDocument9 pagesSCDL Macroeconomics QuestionsAnusha NaiduPas encore d'évaluation

- Daily 14.11.2013Document1 pageDaily 14.11.2013FEPFinanceClubPas encore d'évaluation

- Dovish Vs HawkishDocument9 pagesDovish Vs Hawkisharti guptaPas encore d'évaluation

- The Role of Money in New-Keynesian Models: Banco Central de Reserva Del PerúDocument17 pagesThe Role of Money in New-Keynesian Models: Banco Central de Reserva Del PerúCristian Fernando Sanabria BautistaPas encore d'évaluation

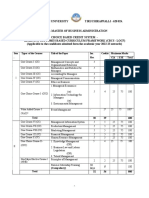

- MBA Syllabus 2022-23Document162 pagesMBA Syllabus 2022-23Trichy MaheshPas encore d'évaluation

- Pre-Board Papers With MS EconomicsDocument160 pagesPre-Board Papers With MS Economicsbksbharatkumar22005Pas encore d'évaluation

- Marxcism Milestone Activity 2Document3 pagesMarxcism Milestone Activity 2Delta OnePas encore d'évaluation

- Rolling and Fixed Planning Fixed PlanningDocument72 pagesRolling and Fixed Planning Fixed PlanningTesfaye GemechuPas encore d'évaluation

- History of Fiscal PolicyDocument13 pagesHistory of Fiscal PolicyYasmine AbdelbaryPas encore d'évaluation

- Subhash Deys Economics Xii Notes For 2024 ExamDocument3 pagesSubhash Deys Economics Xii Notes For 2024 Examkhandelwalkrishna8595Pas encore d'évaluation

- Exchange Rate: USD, EUR and Romanian LeuDocument11 pagesExchange Rate: USD, EUR and Romanian LeupofokanPas encore d'évaluation

- UntitledDocument87 pagesUntitledEtudiant ProPas encore d'évaluation

- Bretton Woods ConferenceDocument25 pagesBretton Woods ConferenceNikita MutrejaPas encore d'évaluation

- Quiz 1 - SolutionsDocument4 pagesQuiz 1 - Solutionsabijith taPas encore d'évaluation

- Central Superior Services (CSS) Examination, Pakistan - Causes of InflationDocument5 pagesCentral Superior Services (CSS) Examination, Pakistan - Causes of InflationAmeer KhanPas encore d'évaluation

- Spring 2014enstDocument9 pagesSpring 2014enstclopazanskiPas encore d'évaluation

- Mini Exam 2Document16 pagesMini Exam 2course101Pas encore d'évaluation

- Macro CH 7 & 8 PDFDocument26 pagesMacro CH 7 & 8 PDFAKSHARA JAINPas encore d'évaluation

- AP Macroeconomics Assignment: Apply Knowledge of UnemploymentDocument2 pagesAP Macroeconomics Assignment: Apply Knowledge of UnemploymentSixPennyUnicorn0% (1)

- Classical Economics: Say's LawDocument24 pagesClassical Economics: Say's LawARBAB RAJPUTPas encore d'évaluation

- Selected Answer: Answers:: 3 Out of 3 PointsDocument4 pagesSelected Answer: Answers:: 3 Out of 3 PointsLocklaim CardinozaPas encore d'évaluation

- If PPTSDocument31 pagesIf PPTSPriti BidasariaPas encore d'évaluation

- Micro and Macro EnvironmentDocument2 pagesMicro and Macro Environmentrhiju lamsalPas encore d'évaluation