Vous aimerez peut-être aussi

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Investment Banking 2005doc669Document29 pagesInvestment Banking 2005doc669tiwariparveshPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Wells Fargo Everyday CheckingDocument3 pagesWells Fargo Everyday Checkingbaga ibakPas encore d'évaluation

- McKinsey ReportDocument58 pagesMcKinsey ReportSetiady MaruliPas encore d'évaluation

- Unit 4 - CH 15 - AdjustedDocument30 pagesUnit 4 - CH 15 - AdjustedNikulPas encore d'évaluation

- Unit 4 - CH 13 - AdjustedDocument34 pagesUnit 4 - CH 13 - AdjustedNikulPas encore d'évaluation

- Unit 3 - CH 11 - AdjustedDocument29 pagesUnit 3 - CH 11 - AdjustedNikulPas encore d'évaluation

- Unit 3 - CH 10 - AdjustedDocument46 pagesUnit 3 - CH 10 - AdjustedNikulPas encore d'évaluation

- Unit 3 - CH 09 - AdjustedDocument29 pagesUnit 3 - CH 09 - AdjustedNikulPas encore d'évaluation

- Unit 2 - CH 08 - AdjustedDocument34 pagesUnit 2 - CH 08 - AdjustedNikulPas encore d'évaluation

- Unit 2 - CH 05 - AdjustedDocument33 pagesUnit 2 - CH 05 - AdjustedNikulPas encore d'évaluation

- Chapter 4 SolutionsDocument7 pagesChapter 4 SolutionsNikulPas encore d'évaluation

- 1Document22 pages1NikulPas encore d'évaluation

- Chapter 8 SolutionsDocument4 pagesChapter 8 SolutionsNikulPas encore d'évaluation

- Haj Application - 2012 - (Print in Legal Size Only)Document6 pagesHaj Application - 2012 - (Print in Legal Size Only)Loved HerPas encore d'évaluation

- Schedule of Charges For Nri Accounts PrimeDocument4 pagesSchedule of Charges For Nri Accounts PrimeSonam SharmaPas encore d'évaluation

- Assignment of Mortgage Assignment OF MortgageDocument4 pagesAssignment of Mortgage Assignment OF MortgageHelpin HandPas encore d'évaluation

- Tudor Capital Europe LLP Pillar 3 Disclosure PDFDocument7 pagesTudor Capital Europe LLP Pillar 3 Disclosure PDFetravoPas encore d'évaluation

- Suggested Answer - Syl12 - Dec13 - Paper 14 Final Examination: Suggested Answers To QuestionsDocument18 pagesSuggested Answer - Syl12 - Dec13 - Paper 14 Final Examination: Suggested Answers To QuestionsMudit AgarwalPas encore d'évaluation

- Irda Forms - Ia / Ib / IcDocument15 pagesIrda Forms - Ia / Ib / IcSenthil KumarPas encore d'évaluation

- Your Vodafone Bill: Amount Due Rs 1178.82 Due Date 08 Jul 2019Document8 pagesYour Vodafone Bill: Amount Due Rs 1178.82 Due Date 08 Jul 2019vaibhavPas encore d'évaluation

- Design of Concrete Structures - : Eurocodes Versus British StandardsDocument2 pagesDesign of Concrete Structures - : Eurocodes Versus British StandardsnsureshbabuPas encore d'évaluation

- OpTransactionHistoryTpr17 09 2019 PDFDocument2 pagesOpTransactionHistoryTpr17 09 2019 PDFSonu DangiPas encore d'évaluation

- Maxi Cosi Mico Infant Car Seat 2010 Instruction Manual PDFDocument34 pagesMaxi Cosi Mico Infant Car Seat 2010 Instruction Manual PDFcarocaoPas encore d'évaluation

- Ad Code IiDocument70 pagesAd Code Iimayur sonawanePas encore d'évaluation

- Remedial Examination - BFIN2121Document21 pagesRemedial Examination - BFIN2121Almirah MakalunasPas encore d'évaluation

- Ace of Capital MarketsDocument4 pagesAce of Capital MarketsAmit GuptaPas encore d'évaluation

- FAQs On Cheque Collection PolicyDocument1 pageFAQs On Cheque Collection PolicyPrasant PrasadPas encore d'évaluation

- EX-99, Boise Inc-Carlson CapitalDocument17 pagesEX-99, Boise Inc-Carlson CapitalJake MannPas encore d'évaluation

- Inheritance Tax - Part 2: Relevant To Acca Qualification Paper F6 (Uk)Document13 pagesInheritance Tax - Part 2: Relevant To Acca Qualification Paper F6 (Uk)Shuja Muhammad LaghariPas encore d'évaluation

- Examples of Loan TransactionsDocument2 pagesExamples of Loan TransactionsVimal AnbalaganPas encore d'évaluation

- Full Download Book Financial Services PDFDocument41 pagesFull Download Book Financial Services PDFcalvin.williams888100% (13)

- List of World Bank MembersDocument4 pagesList of World Bank MembersUsman KhalidPas encore d'évaluation

- Banking Techniques ProjectDocument10 pagesBanking Techniques ProjectOana PredaPas encore d'évaluation

- Cif IndividualDocument2 pagesCif IndividualKeyla LumapasPas encore d'évaluation

- Singhi Advisors Corporate ProfileDocument27 pagesSinghi Advisors Corporate ProfilemarkelonnPas encore d'évaluation

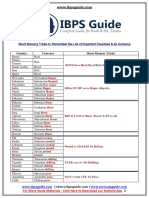

- Short TricksDocument2 pagesShort TricksAditi SaxenaPas encore d'évaluation

- Comprehensive NotesDocument13 pagesComprehensive NotesBelle Andrea GozonPas encore d'évaluation

- Promotion Test 2021-22 Study Material (2021) Based Mcqs SeriesDocument4 pagesPromotion Test 2021-22 Study Material (2021) Based Mcqs Seriesprashant singhPas encore d'évaluation

- TelPro 1101 Tele-Tower Operation ManualDocument20 pagesTelPro 1101 Tele-Tower Operation ManualDouglas Allen Hughes SrPas encore d'évaluation

- Intro ERP Using GBI Case Study FI (Letter) en v2.40Document22 pagesIntro ERP Using GBI Case Study FI (Letter) en v2.40meddebyounesPas encore d'évaluation