Vous aimerez peut-être aussi

- Business Environment Assignment: Policy Decision Taken On Oil & Gas Exploration & Allied ServicesDocument2 pagesBusiness Environment Assignment: Policy Decision Taken On Oil & Gas Exploration & Allied ServicesAbhijit RoyPas encore d'évaluation

- Budget-Dtc-Tax Exemption IncomeDocument35 pagesBudget-Dtc-Tax Exemption IncomeAnkit MachharPas encore d'évaluation

- Current AfiarsDocument7 pagesCurrent AfiarsDr.V.Bastin JeromePas encore d'évaluation

- Oil and Natural Gas SectorDocument16 pagesOil and Natural Gas Sectorsmritim_3Pas encore d'évaluation

- Power SectorDocument3 pagesPower SectorVedant ThakkarPas encore d'évaluation

- 4th March 2010 Finance + BudgetDocument41 pages4th March 2010 Finance + BudgetNeha GargPas encore d'évaluation

- Research - Note - 2014 07 10 - 10 27 38 000000Document6 pagesResearch - Note - 2014 07 10 - 10 27 38 000000prateekramchandaniPas encore d'évaluation

- Project Report On Taxation News Analysis: Guided By: Prof. Anil GorDocument19 pagesProject Report On Taxation News Analysis: Guided By: Prof. Anil GorChirag PatelPas encore d'évaluation

- Union Budget 2010-2011: Symphony of Fiscal Consolidation and Continued GrowthDocument7 pagesUnion Budget 2010-2011: Symphony of Fiscal Consolidation and Continued GrowthChand AnsariPas encore d'évaluation

- KPMG Union Budget Energy and Natural Resources PoV 2015Document9 pagesKPMG Union Budget Energy and Natural Resources PoV 2015Mukul AzadPas encore d'évaluation

- Overview of The Union Financial Budget 2010-11: 1 ForewordDocument35 pagesOverview of The Union Financial Budget 2010-11: 1 ForewordCyril HopkinsPas encore d'évaluation

- Budget 2009-10Document10 pagesBudget 2009-10bhramaniPas encore d'évaluation

- Budget Presentation 2018/2019Document21 pagesBudget Presentation 2018/2019Abdul RahimPas encore d'évaluation

- Budget Red Eye 2013Document5 pagesBudget Red Eye 2013Envisage123Pas encore d'évaluation

- General: GDP Is Expected To Grow in The Region of 8.75% To 9.25%. The MinisterDocument5 pagesGeneral: GDP Is Expected To Grow in The Region of 8.75% To 9.25%. The MinisterSuraj NaikPas encore d'évaluation

- Finance Budget 2023Document4 pagesFinance Budget 2023SakshamPas encore d'évaluation

- Salient Features: Customs Budgetary Measures 2008-09Document16 pagesSalient Features: Customs Budgetary Measures 2008-09sadiajanPas encore d'évaluation

- Union Budget 2012-13 Review: Ansaf PMDocument21 pagesUnion Budget 2012-13 Review: Ansaf PMAnsaf MohdPas encore d'évaluation

- Salient Features: Customs Budgetary Measures 2007-08Document17 pagesSalient Features: Customs Budgetary Measures 2007-08sadiajanPas encore d'évaluation

- Interim Budget 2019: Proposed Amendments in Direct Tax ProvisionsDocument4 pagesInterim Budget 2019: Proposed Amendments in Direct Tax ProvisionsaaPas encore d'évaluation

- 9 January - 15 January, 2011: TH THDocument14 pages9 January - 15 January, 2011: TH THRamnaresh KabraPas encore d'évaluation

- Union Budget 2012: Industry, Infrastructure, Agriculture Group No. 3Document23 pagesUnion Budget 2012: Industry, Infrastructure, Agriculture Group No. 3Chetan PatilPas encore d'évaluation

- Budget - Sectors Which Got AffectedDocument8 pagesBudget - Sectors Which Got AffectedManikanta SatishPas encore d'évaluation

- Budget Analysis 2012Document26 pagesBudget Analysis 2012Rajpreet KaurPas encore d'évaluation

- Budget AnalysisDocument11 pagesBudget AnalysisvenkatpogaruPas encore d'évaluation

- 07 BE Week4 Shreyas Roll No 52Document4 pages07 BE Week4 Shreyas Roll No 52Shreyas RautPas encore d'évaluation

- Income Tax - Major Highlights of Union Budget - 2011-12: Prasad V Sawant Roll No:96 Tax AssignmentDocument5 pagesIncome Tax - Major Highlights of Union Budget - 2011-12: Prasad V Sawant Roll No:96 Tax AssignmentJohn DoinPas encore d'évaluation

- Budget 2012-13 & It's Effect On Power and InfrastructureDocument27 pagesBudget 2012-13 & It's Effect On Power and InfrastructureHiren PatelPas encore d'évaluation

- Key Highlights of The Union Budget 2012-13: A Full Service Corporate Law FirmDocument5 pagesKey Highlights of The Union Budget 2012-13: A Full Service Corporate Law FirmCn NatarajanPas encore d'évaluation

- Background: Infrastructure DevelopmentDocument5 pagesBackground: Infrastructure DevelopmentvishwanathPas encore d'évaluation

- Presentationonbudget2023-24 RevisedDocument14 pagesPresentationonbudget2023-24 RevisedHyderali Mufazzal KantawalaPas encore d'évaluation

- IT&STDocument2 pagesIT&STPraveen DsouzaPas encore d'évaluation

- Ime AssignmentDocument18 pagesIme Assignmentsajalkhulbe23Pas encore d'évaluation

- Budget Analysis 2010-2011: Finance CommitteeDocument52 pagesBudget Analysis 2010-2011: Finance CommitteeSahil ShahaPas encore d'évaluation

- Intrim Union Budget 2019-20Document12 pagesIntrim Union Budget 2019-20Rukmani GuptaPas encore d'évaluation

- Budget 2012-13Document44 pagesBudget 2012-13Rashi AgrawalPas encore d'évaluation

- LA Presentation FinalDocument29 pagesLA Presentation FinalMadhu Mohan BhukyaPas encore d'évaluation

- 1206purl Weekly-6868Document17 pages1206purl Weekly-6868Harish SatyaPas encore d'évaluation

- Union Budget 2007Document5 pagesUnion Budget 2007Pawan LingayatPas encore d'évaluation

- Budget 2010 in Small Scale IndustriesDocument9 pagesBudget 2010 in Small Scale Industriesurz_spiderman2630Pas encore d'évaluation

- KPMG Union Budget TL PoV 2015Document9 pagesKPMG Union Budget TL PoV 2015Raghav KhileryPas encore d'évaluation

- Feb 2023Document55 pagesFeb 2023TirunamalaPhanimohanPas encore d'évaluation

- Budget 2010Document9 pagesBudget 2010Sartaj KhanPas encore d'évaluation

- Union Budget 2012Document23 pagesUnion Budget 2012Deepak Singh BishtPas encore d'évaluation

- Budget 2012-13 - Living Beyond The Means: March 2012Document8 pagesBudget 2012-13 - Living Beyond The Means: March 2012samri123Pas encore d'évaluation

- Background: GDP Wholesale Price Index Fiscal DeficitDocument5 pagesBackground: GDP Wholesale Price Index Fiscal Deficitdhimant_123Pas encore d'évaluation

- Budget NoteDocument4 pagesBudget NoteSunil SharmaPas encore d'évaluation

- Union Budget 2011: Tax Holiday For Power Sector Exended by One YearDocument12 pagesUnion Budget 2011: Tax Holiday For Power Sector Exended by One Yearvivek_sharma@live.inPas encore d'évaluation

- Presentationonbudget2023 24 230201200109 7a4f5a20Document15 pagesPresentationonbudget2023 24 230201200109 7a4f5a20harshitsingh.79835Pas encore d'évaluation

- Budget Sector Wise Analysis-BenchmarkersDocument4 pagesBudget Sector Wise Analysis-BenchmarkersnikircoolPas encore d'évaluation

- Budget 2011 Impact On Auto Sector: Cars and Bike Prices Won't Go UpDocument10 pagesBudget 2011 Impact On Auto Sector: Cars and Bike Prices Won't Go UpLigin MathewPas encore d'évaluation

- Budget Highlights KPRCDocument4 pagesBudget Highlights KPRCA & A AssociatesPas encore d'évaluation

- India: Budget 2015-16 - For The Corporates: Corporate Tax RateDocument4 pagesIndia: Budget 2015-16 - For The Corporates: Corporate Tax RateraghuPas encore d'évaluation

- Benefits For InfrastructureDocument13 pagesBenefits For InfrastructureashutoshmuglikarPas encore d'évaluation

- Central Taxes Replaced by GSTDocument6 pagesCentral Taxes Replaced by GSTBijosh ThomasPas encore d'évaluation

- Budget 2010: Impact On Sectors That Investors Need To FollowDocument33 pagesBudget 2010: Impact On Sectors That Investors Need To FollowNMRaycPas encore d'évaluation

- Category Current (RS) Proposed (RS) Savings P.A. (RS) : Direct TaxDocument16 pagesCategory Current (RS) Proposed (RS) Savings P.A. (RS) : Direct TaxshwetakuppanPas encore d'évaluation

- Union Budget 2013-14: Key Takeout's From The BudgetDocument4 pagesUnion Budget 2013-14: Key Takeout's From The BudgetFeedback Business Consulting Services Pvt. Ltd.Pas encore d'évaluation

- AcvdvdDocument4 pagesAcvdvdvivek kasamPas encore d'évaluation

- Credit Note: Reconnect Energy Solutions Pvt. LTDDocument1 pageCredit Note: Reconnect Energy Solutions Pvt. LTDVindyanchal KumarPas encore d'évaluation

- Credit Note: Reconnect Energy Solutions Pvt. LTDDocument1 pageCredit Note: Reconnect Energy Solutions Pvt. LTDVindyanchal KumarPas encore d'évaluation

- LQS ManualDocument38 pagesLQS ManualVindyanchal Kumar100% (1)

- Credit Note: Reconnect Energy Solutions Pvt. LTDDocument1 pageCredit Note: Reconnect Energy Solutions Pvt. LTDVindyanchal KumarPas encore d'évaluation

- Credit Note: Reconnect Energy Solutions Pvt. LTDDocument1 pageCredit Note: Reconnect Energy Solutions Pvt. LTDVindyanchal KumarPas encore d'évaluation

- Credit Note: Reconnect Energy Solutions Pvt. LTDDocument1 pageCredit Note: Reconnect Energy Solutions Pvt. LTDVindyanchal KumarPas encore d'évaluation

- User Guide E-Ticket BookingDocument6 pagesUser Guide E-Ticket BookingVindyanchal KumarPas encore d'évaluation

- International / NRI User RegistrationDocument5 pagesInternational / NRI User RegistrationVindyanchal KumarPas encore d'évaluation

- International / NRI User RegistrationDocument5 pagesInternational / NRI User RegistrationVindyanchal KumarPas encore d'évaluation

- User Guide E-Ticket BookingDocument6 pagesUser Guide E-Ticket BookingVindyanchal KumarPas encore d'évaluation

- User manual-REMC Forecasting and Scheduling ApplicationDocument145 pagesUser manual-REMC Forecasting and Scheduling ApplicationVindyanchal KumarPas encore d'évaluation

- User manual-REMC Forecasting and Scheduling ApplicationDocument145 pagesUser manual-REMC Forecasting and Scheduling ApplicationVindyanchal KumarPas encore d'évaluation

- LQS ManualDocument38 pagesLQS ManualVindyanchal Kumar100% (1)

- NIT - CJI5041P21 - OIl India TenderDocument84 pagesNIT - CJI5041P21 - OIl India TenderVindyanchal KumarPas encore d'évaluation

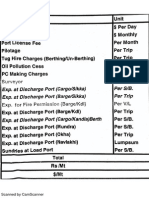

- Port ExpensesDocument1 pagePort ExpensesVindyanchal KumarPas encore d'évaluation

- NIT - CJI5041P21 - OIl India TenderDocument84 pagesNIT - CJI5041P21 - OIl India TenderVindyanchal KumarPas encore d'évaluation

- Xtra Power Fleet CardDocument16 pagesXtra Power Fleet CardVindyanchal KumarPas encore d'évaluation

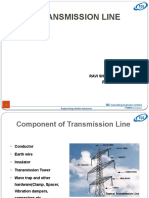

- Transmission Line: Ravi Shankar Singh (E6S304)Document44 pagesTransmission Line: Ravi Shankar Singh (E6S304)amit143263Pas encore d'évaluation

- Job Analysis Jan 14Document25 pagesJob Analysis Jan 14Vindyanchal KumarPas encore d'évaluation

- EdelweissDocument7 pagesEdelweissVindyanchal KumarPas encore d'évaluation

- Omega Renk - Registration CertificateDocument1 pageOmega Renk - Registration CertificateVindyanchal KumarPas encore d'évaluation

- Energy Derivatives: Sonal GuptaDocument48 pagesEnergy Derivatives: Sonal GuptaVindyanchal Kumar100% (1)

- New Microsoft PowerPoint PresentationDocument10 pagesNew Microsoft PowerPoint PresentationVindyanchal KumarPas encore d'évaluation

- Selection Feb 14Document36 pagesSelection Feb 14Vindyanchal KumarPas encore d'évaluation

- Questionaire: All Information Obtained Will Beused For Academic Purpose OnlyDocument3 pagesQuestionaire: All Information Obtained Will Beused For Academic Purpose OnlyVindyanchal KumarPas encore d'évaluation

- E-Commerce: Overview of Electronic CommerceDocument39 pagesE-Commerce: Overview of Electronic CommerceVindyanchal KumarPas encore d'évaluation

- Questioners: All Information Obtained Will Be Used For Academic Purpose OnlyDocument3 pagesQuestioners: All Information Obtained Will Be Used For Academic Purpose OnlyVindyanchal KumarPas encore d'évaluation

- Knowlege Process OutsourcingDocument1 pageKnowlege Process OutsourcingVindyanchal KumarPas encore d'évaluation

- Hydrocarbon Vision 2020Document23 pagesHydrocarbon Vision 2020Vindyanchal KumarPas encore d'évaluation

- Content Problem Sets 4. Review Test Submission: Problem Set 08Document8 pagesContent Problem Sets 4. Review Test Submission: Problem Set 08gggPas encore d'évaluation

- Accounting ProjectDocument2 pagesAccounting ProjectAngel Grefaldo VillegasPas encore d'évaluation

- Primer On Islamic FInanceDocument31 pagesPrimer On Islamic FInanceGuiPas encore d'évaluation

- Public Private Partnership Booklet - enDocument28 pagesPublic Private Partnership Booklet - enJoePas encore d'évaluation

- Chapter 7 Risk and Return Question and Answer From TitmanDocument2 pagesChapter 7 Risk and Return Question and Answer From TitmanMd Jahid HossainPas encore d'évaluation

- Founders Equity AgreementDocument2 pagesFounders Equity AgreementrobogineerPas encore d'évaluation

- AXA Rosenberg Equity Alpha Trust September Interim 2017Document257 pagesAXA Rosenberg Equity Alpha Trust September Interim 2017Saluka KulathungaPas encore d'évaluation

- Iesco Online Billl PDFDocument2 pagesIesco Online Billl PDFAsad AliPas encore d'évaluation

- Fin 311 Chapter 02 HandoutDocument7 pagesFin 311 Chapter 02 HandouteinsteinspyPas encore d'évaluation

- Difference Between Ind As 16, As 10Document6 pagesDifference Between Ind As 16, As 10VivekPas encore d'évaluation

- Agrarian Crisis and Farmer SuicidesDocument38 pagesAgrarian Crisis and Farmer SuicidesbtnaveenkumarPas encore d'évaluation

- AccountingDocument5 pagesAccountingMaitet CarandangPas encore d'évaluation

- Hotel ProjectDocument38 pagesHotel ProjectMelat MakonnenPas encore d'évaluation

- Assertions of Compliance With Accountability RequirementsDocument2 pagesAssertions of Compliance With Accountability RequirementslouvellePas encore d'évaluation

- Wright National Flood Insurance Company A Stock Company PO Box 33003 St. Petersburg, FL, 33733 Office: 800.820.3242 Fax: 800.850.3299Document1 pageWright National Flood Insurance Company A Stock Company PO Box 33003 St. Petersburg, FL, 33733 Office: 800.820.3242 Fax: 800.850.3299ronaldo alvaradoPas encore d'évaluation

- Group Assignment Cover Sheet: Student DetailsDocument9 pagesGroup Assignment Cover Sheet: Student DetailsMinh DucPas encore d'évaluation

- 7th NFC Award 2010Document4 pages7th NFC Award 2010humayun313Pas encore d'évaluation

- DHL AWB Sweden2 30-4-21Document5 pagesDHL AWB Sweden2 30-4-21Ajay KumarPas encore d'évaluation

- GSRTCDocument1 pageGSRTCRaju PatelPas encore d'évaluation

- Chapter 12Document11 pagesChapter 12Kim Patrice NavarraPas encore d'évaluation

- L2 Business PlanDocument26 pagesL2 Business PlanMohammad Nur Hakimi SulaimanPas encore d'évaluation

- CAEmploymentGuide2014 PDF 23april2014Document156 pagesCAEmploymentGuide2014 PDF 23april2014Jessica100% (1)

- Decline of Spain SummaryDocument4 pagesDecline of Spain SummaryNathan RoytersPas encore d'évaluation

- Acct Statement XX5203 16122023Document3 pagesAcct Statement XX5203 16122023sa6307756Pas encore d'évaluation

- The Financial BehaviorDocument12 pagesThe Financial BehaviorAkob KadirPas encore d'évaluation

- Why Oil and Gas Development Company Limited (OGDCL) Should Not Be PrivatizedDocument11 pagesWhy Oil and Gas Development Company Limited (OGDCL) Should Not Be PrivatizedZohaib GondalPas encore d'évaluation

- Document 886483241Document38 pagesDocument 886483241Cirillo Mendes RibeiroPas encore d'évaluation

- Brand ExtensionDocument6 pagesBrand Extensionmukhtal8909Pas encore d'évaluation

- Syndicate 6 - Gainesboro Machine Tools CorporationDocument12 pagesSyndicate 6 - Gainesboro Machine Tools CorporationSimon ErickPas encore d'évaluation

- Chapter 6 Financial Statements Tools For Decision MakingDocument25 pagesChapter 6 Financial Statements Tools For Decision MakingEunice NunezPas encore d'évaluation