Vous aimerez peut-être aussi

- Fafp Research PaperDocument11 pagesFafp Research PaperVivek Soni100% (1)

- FIDIC Red and Pink BookDocument6 pagesFIDIC Red and Pink Bookhmd rasika100% (2)

- INTERMEDIATE ACCOUNTING Vol. 1 (2021 Edition) - Valix, Peralta & Valix - XLSX Chapter 1Document7 pagesINTERMEDIATE ACCOUNTING Vol. 1 (2021 Edition) - Valix, Peralta & Valix - XLSX Chapter 1Rodolfo Manalac100% (2)

- Expert Fraud Investigation A Step by Step Guide PDFDocument2 pagesExpert Fraud Investigation A Step by Step Guide PDFNataliePas encore d'évaluation

- Fraud ScenariosDocument7 pagesFraud ScenariosElvisPresliiPas encore d'évaluation

- Fraud PoliciesDocument67 pagesFraud PoliciesNfareePas encore d'évaluation

- Fraud InvestigationDocument19 pagesFraud InvestigationTHANPas encore d'évaluation

- Manual On The Spot ChecksDocument113 pagesManual On The Spot ChecksEmilPas encore d'évaluation

- Askari Bank LTDDocument12 pagesAskari Bank LTDMuhammadAmmarKhalidPas encore d'évaluation

- Synopsis How Privatized Banking Really WorksDocument17 pagesSynopsis How Privatized Banking Really Worksjohan_lindstromPas encore d'évaluation

- Https Mail-Attachment - Googleusercontent.com Attachment U 0 Ui 2&ik 92fc937495&view Att&th 13f898b2a981773a&attid 0Document6 pagesHttps Mail-Attachment - Googleusercontent.com Attachment U 0 Ui 2&ik 92fc937495&view Att&th 13f898b2a981773a&attid 0epolPas encore d'évaluation

- Fraud Scheme - Singleton Edisi 3Document20 pagesFraud Scheme - Singleton Edisi 3AredheKurniawanPas encore d'évaluation

- Fraud Risk Assement For B BankDocument66 pagesFraud Risk Assement For B BankdbedadaPas encore d'évaluation

- Fraud Red FlagsDocument15 pagesFraud Red FlagsRatna Saridewi100% (1)

- Fraud Diamond Four Elements - CPAJ2004 PDFDocument5 pagesFraud Diamond Four Elements - CPAJ2004 PDFveranitaPas encore d'évaluation

- Internet Fraud 6monthreport 2000 ADocument14 pagesInternet Fraud 6monthreport 2000 AFlaviub23Pas encore d'évaluation

- Continuous Fraud DetectionDocument23 pagesContinuous Fraud Detectionbudi.hw748Pas encore d'évaluation

- TATA AIA - Anti Fraud PolicyDocument10 pagesTATA AIA - Anti Fraud PolicyAnurag JagnaniPas encore d'évaluation

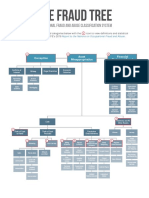

- Fraud-Tree SchemesDocument13 pagesFraud-Tree SchemessulthanhakimPas encore d'évaluation

- Payroll FraudDocument3 pagesPayroll FraudEBY TradersPas encore d'évaluation

- Tools and Techniques For Prevention of FraudsDocument12 pagesTools and Techniques For Prevention of Fraudsrahul kumarPas encore d'évaluation

- 15 Asset Misappropriation PDFDocument60 pages15 Asset Misappropriation PDFswathivishnuPas encore d'évaluation

- Introduction, Conceptual Framework of The Study & Research DesignDocument16 pagesIntroduction, Conceptual Framework of The Study & Research DesignSтυριd・ 3尺ㄖ尺Pas encore d'évaluation

- Procurement FraudDocument16 pagesProcurement FraudpauljayakarPas encore d'évaluation

- Content Fraud BrainstormingDocument6 pagesContent Fraud BrainstormingCreanga GeorgianPas encore d'évaluation

- Role of IT in Fraud DetectionDocument11 pagesRole of IT in Fraud DetectionYogeshPas encore d'évaluation

- Forensic Report 1Document10 pagesForensic Report 1a2zconsultantsjprPas encore d'évaluation

- Fraud IndicatorsDocument26 pagesFraud IndicatorsIena SharinaPas encore d'évaluation

- Online Transaction Fraud Detection Using Python & Backlogging On E-CommerceDocument6 pagesOnline Transaction Fraud Detection Using Python & Backlogging On E-CommerceThe Futura LabsPas encore d'évaluation

- Frauds in Indian Banking SectorDocument5 pagesFrauds in Indian Banking SectorPayal Ambhore100% (1)

- Content Fraud BrainstormingDocument6 pagesContent Fraud BrainstormingHaris BurneyPas encore d'évaluation

- Generic Definition: ": Manufacturing Inventory: Besides Finished Goods, Also Includes Raw Materials Used inDocument12 pagesGeneric Definition: ": Manufacturing Inventory: Besides Finished Goods, Also Includes Raw Materials Used inRosita BarcaloungerPas encore d'évaluation

- The Role of Auditors in Fraud Detection and PreventionDocument9 pagesThe Role of Auditors in Fraud Detection and PreventionCharmaine Mapesho CharlottePas encore d'évaluation

- Phishing Fraud AnalysisDocument23 pagesPhishing Fraud AnalysisTejas ChokshiPas encore d'évaluation

- PPP - Research Paper - FafdDocument11 pagesPPP - Research Paper - Fafdharshita patniPas encore d'évaluation

- Fraud AuditingDocument38 pagesFraud AuditingTauqeer100% (3)

- 5 6318691500020466224-1Document5 pages5 6318691500020466224-1shuchim guptaPas encore d'évaluation

- Fraudulent DisbursementsDocument6 pagesFraudulent DisbursementsTrizzia Ann BantucanPas encore d'évaluation

- Controlling Credit Card FraudDocument4 pagesControlling Credit Card Fraudbalaji bysaniPas encore d'évaluation

- Intro To Fraud ExaminationDocument13 pagesIntro To Fraud ExaminationGladys CanterosPas encore d'évaluation

- Bank Employee FraudDocument52 pagesBank Employee FraudCharles B. HallPas encore d'évaluation

- Fraud TheoriesDocument24 pagesFraud TheoriesAlexMouraPas encore d'évaluation

- Common Fraud Scenarios GuideDocument10 pagesCommon Fraud Scenarios GuideGiancarlo Pajuelo CanccePas encore d'évaluation

- Fraud Risk MDocument11 pagesFraud Risk MEka Septariana PuspaPas encore d'évaluation

- Identity Fraud - Lillian FisherDocument5 pagesIdentity Fraud - Lillian Fisherapi-530231271Pas encore d'évaluation

- Anti Money LaunderingDocument41 pagesAnti Money LaunderingGagan GoelPas encore d'évaluation

- Data AlterationDocument13 pagesData AlterationVicky SharmaPas encore d'évaluation

- Telecommunication Fraud and Detection Techniques: A ReviewDocument3 pagesTelecommunication Fraud and Detection Techniques: A ReviewEditor IJRITCCPas encore d'évaluation

- Demat Account Fraud - How To Safeguard Against Demat Account FraudDocument2 pagesDemat Account Fraud - How To Safeguard Against Demat Account FraudJayaprakash Muthuvat100% (1)

- Cyber Crime in Banking SectorDocument86 pagesCyber Crime in Banking SectorAnand ChavanPas encore d'évaluation

- Forensic Audit Report of Club RainbowDocument10 pagesForensic Audit Report of Club RainbowA Kumar Legacy100% (1)

- Bounching Check LawDocument2 pagesBounching Check LawNeria SagunPas encore d'évaluation

- Citi Commercial Card Fraud FAQDocument3 pagesCiti Commercial Card Fraud FAQSajan JosePas encore d'évaluation

- Financial Remediation FrameworkDocument5 pagesFinancial Remediation FrameworkForeclosure FraudPas encore d'évaluation

- Fraud Pentagon Dalam Mendeteksi Financial Statement FraudDocument14 pagesFraud Pentagon Dalam Mendeteksi Financial Statement FraudChill GouvtfrondPas encore d'évaluation

- Highlights of A Forum Combating Synthetic Identity Fraud: Accessible VersionDocument33 pagesHighlights of A Forum Combating Synthetic Identity Fraud: Accessible VersionMista ManPas encore d'évaluation

- Anti Money Laundary Q and AnswerDocument5 pagesAnti Money Laundary Q and AnswerHassan MohamedPas encore d'évaluation

- Fraud 101: Techniques and Strategies for DetectionD'EverandFraud 101: Techniques and Strategies for DetectionPas encore d'évaluation

- FAFP Backgroud PDFDocument165 pagesFAFP Backgroud PDFRahul KhannaPas encore d'évaluation

- Picpa Davao - Coso Internal Control SlidesDocument86 pagesPicpa Davao - Coso Internal Control SlidesMariell Ann AbalosPas encore d'évaluation

- Fraud Awareness Training: Detection and PreventionDocument20 pagesFraud Awareness Training: Detection and PreventionDataMis EliosHealthCarePas encore d'évaluation

- January 2013 - Anti-Fraud and The IA FunctionDocument88 pagesJanuary 2013 - Anti-Fraud and The IA FunctionTARIQPas encore d'évaluation

- 196 407 1 SM PDFDocument15 pages196 407 1 SM PDFPrana Djati NingrumPas encore d'évaluation

- Itrac13london 23Document7 pagesItrac13london 23Prana Djati NingrumPas encore d'évaluation

- Struktur Dan Kinerja OrganisasiDocument118 pagesStruktur Dan Kinerja OrganisasiPrana Djati NingrumPas encore d'évaluation

- Do The Stupid Support The Dullest?Document3 pagesDo The Stupid Support The Dullest?Prana Djati NingrumPas encore d'évaluation

- Evolution and Critical Evaluation of Current Management PracticesDocument98 pagesEvolution and Critical Evaluation of Current Management PracticessirrhougePas encore d'évaluation

- Webcase 2: Human Resources Management and Small BusinessesDocument2 pagesWebcase 2: Human Resources Management and Small BusinessesPrana Djati NingrumPas encore d'évaluation

- Kd04 Atkisson A Review of Practical Sustainable DevelopmentDocument73 pagesKd04 Atkisson A Review of Practical Sustainable DevelopmentPrana Djati NingrumPas encore d'évaluation

- Public Speaking Tips For Business Leaders: By: Ike Janita DewiDocument22 pagesPublic Speaking Tips For Business Leaders: By: Ike Janita DewiPrana Djati NingrumPas encore d'évaluation

- A New Market in Germany: Corporate VenturingDocument6 pagesA New Market in Germany: Corporate VenturingPrana Djati NingrumPas encore d'évaluation

- Training and Developing Employees: Gary DesslerDocument42 pagesTraining and Developing Employees: Gary DesslerPrana Djati NingrumPas encore d'évaluation

- Employee Testing and Selection: Gary DesslerDocument52 pagesEmployee Testing and Selection: Gary DesslerPrana Djati NingrumPas encore d'évaluation

- Ubl History: 1. Karachi Dacca Lahore Lyallpur Chittagong NarayanganjDocument2 pagesUbl History: 1. Karachi Dacca Lahore Lyallpur Chittagong NarayanganjMuhammad Tayyab RazaPas encore d'évaluation

- Chapter 09 Risk Management: Asset-Backed Securities, Loan Sales, Credit Standbys, and Credit DerivativesDocument33 pagesChapter 09 Risk Management: Asset-Backed Securities, Loan Sales, Credit Standbys, and Credit DerivativesNway Moe Saung100% (2)

- Idioms BookDocument110 pagesIdioms BookCorneliu Meciu100% (1)

- Uralsib CSR Report 2009Document119 pagesUralsib CSR Report 2009api-115711968Pas encore d'évaluation

- Koito Case Questions 2,3,4Document2 pagesKoito Case Questions 2,3,4Simo RajyPas encore d'évaluation

- Financial Sector Liberalisation in JamaicaDocument97 pagesFinancial Sector Liberalisation in JamaicaAdrian KeysPas encore d'évaluation

- Banking Unbound Origins To The Digital FrontiersDocument229 pagesBanking Unbound Origins To The Digital FrontiersUmar WynePas encore d'évaluation

- Citibank v. SabenianoDocument5 pagesCitibank v. SabenianoBananaPas encore d'évaluation

- Do Ha Qatar FormDocument4 pagesDo Ha Qatar FormsajidPas encore d'évaluation

- Cashmanagement All Currencies en PDFDocument521 pagesCashmanagement All Currencies en PDFFausto RosaPas encore d'évaluation

- Credit Guarantee Fund Trust For Micro & Small EnterprisesDocument19 pagesCredit Guarantee Fund Trust For Micro & Small EnterprisesAnand SinghPas encore d'évaluation

- Birla Sun Life InsuranceDocument21 pagesBirla Sun Life Insurancecharu100% (3)

- Ashiq HossainDocument54 pagesAshiq HossainAshiq Hossain100% (1)

- Banking LiesDocument13 pagesBanking LiesJua89% (9)

- Regulations of Finance in EthiopiaDocument6 pagesRegulations of Finance in Ethiopiahiroyukisanada310Pas encore d'évaluation

- Unit - 20 - Banking Operations - NestoDocument4 pagesUnit - 20 - Banking Operations - NestoBarun Kumar SinghPas encore d'évaluation

- Abbott India: FY20 Performance Reflects Strength of Power BrandsDocument5 pagesAbbott India: FY20 Performance Reflects Strength of Power BrandspremPas encore d'évaluation

- Micro Finance Indian ScenarioDocument16 pagesMicro Finance Indian ScenarioKaran MehtaPas encore d'évaluation

- Electronic Funds Transfer Application: WWW - Rakbank.aeDocument2 pagesElectronic Funds Transfer Application: WWW - Rakbank.aeMehran KhanPas encore d'évaluation

- Namita Mams ResumeDocument33 pagesNamita Mams Resumesachin11hahaPas encore d'évaluation

- Merged Past Papers SuggestedDocument70 pagesMerged Past Papers Suggestedaditimujumdar2710Pas encore d'évaluation

- SSP Application GuideDocument10 pagesSSP Application GuideAnirudh IndanaPas encore d'évaluation

- Law SyllabusDocument157 pagesLaw SyllabusjiaorrahmanPas encore d'évaluation

- Thesiz Is FinalDocument56 pagesThesiz Is FinalZohra TanveerPas encore d'évaluation

- Mwananchi TheCitizenV3 PDFDocument1 pageMwananchi TheCitizenV3 PDFAnonymous FnM14a0Pas encore d'évaluation