Vous aimerez peut-être aussi

- Emerging Industrial Relation ScenariopptignouDocument27 pagesEmerging Industrial Relation ScenariopptignouvalarmathiyaPas encore d'évaluation

- 4 Motiv, Emot, Values Fall09Document35 pages4 Motiv, Emot, Values Fall09ziabuttPas encore d'évaluation

- Consumer Behavior Models in TourismDocument105 pagesConsumer Behavior Models in Tourismgprasadatvu0% (1)

- Cheat Sheets of Python Libraries TensorflowDocument3 pagesCheat Sheets of Python Libraries TensorflowgprasadatvuPas encore d'évaluation

- Ir & Emerging Socio Economic Scenario...Document8 pagesIr & Emerging Socio Economic Scenario...2ruchi889% (9)

- Bamber CH 13 India SlidesDocument25 pagesBamber CH 13 India SlidesAndrewVazPas encore d'évaluation

- Hall Ticket Cum Test Fee Receipt: Important InstructionsDocument1 pageHall Ticket Cum Test Fee Receipt: Important InstructionsgprasadatvuPas encore d'évaluation

- Human Resource Planning IGNOU All in OneDocument202 pagesHuman Resource Planning IGNOU All in OnegprasadatvuPas encore d'évaluation

- MIT6 006F11 Lec02 Orig PDFDocument9 pagesMIT6 006F11 Lec02 Orig PDFgprasadatvuPas encore d'évaluation

- RPubs - Text-Mining With Rvest and QdapDocument17 pagesRPubs - Text-Mining With Rvest and QdapgprasadatvuPas encore d'évaluation

- A Spell-Checker in R - AnrprogrammerDocument6 pagesA Spell-Checker in R - AnrprogrammergprasadatvuPas encore d'évaluation

- All Cheat Sheets PDFDocument6 pagesAll Cheat Sheets PDFgprasadatvuPas encore d'évaluation

- Regex - Extract Pattern From String, Strip Text, Convert To Numeric and Sum in R DataDocument2 pagesRegex - Extract Pattern From String, Strip Text, Convert To Numeric and Sum in R DatagprasadatvuPas encore d'évaluation

- IELTS Task 1 New Answer SheetDocument2 pagesIELTS Task 1 New Answer SheetChrisGovasPas encore d'évaluation

- Https Raw - Githubusercontent.com Joelgrus Data-Science-From-Scratch Master Code Natural Language ProcessingDocument5 pagesHttps Raw - Githubusercontent.com Joelgrus Data-Science-From-Scratch Master Code Natural Language ProcessinggprasadatvuPas encore d'évaluation

- Big-O Complexity Chart & Data Structure OperationsDocument2 pagesBig-O Complexity Chart & Data Structure OperationsDhruvaSPas encore d'évaluation

- Learning From Data - Online Course (MOOC)Document2 pagesLearning From Data - Online Course (MOOC)gprasadatvuPas encore d'évaluation

- HyDocument3 pagesHygprasadatvuPas encore d'évaluation

- Https Raw - Githubusercontent.com Joelgrus Data-Science-From-Scratch Master Code Natural Language ProcessingDocument5 pagesHttps Raw - Githubusercontent.com Joelgrus Data-Science-From-Scratch Master Code Natural Language ProcessinggprasadatvuPas encore d'évaluation

- List of Machine Learning Certifications and Best Data Science BootcampsDocument23 pagesList of Machine Learning Certifications and Best Data Science BootcampsgprasadatvuPas encore d'évaluation

- QDocument2 pagesQgprasadatvuPas encore d'évaluation

- Keras Cheat Sheet PythonDocument1 pageKeras Cheat Sheet PythonJohnPas encore d'évaluation

- Https Raw - Githubusercontent.com Joelgrus Data-Science-From-Scratch Master Code Working With DataDocument7 pagesHttps Raw - Githubusercontent.com Joelgrus Data-Science-From-Scratch Master Code Working With DatagprasadatvuPas encore d'évaluation

- ALGO-Merge-Sort-IntroDocument47 pagesALGO-Merge-Sort-IntrodPas encore d'évaluation

- Getting Data from APIs and Web ScrapingDocument4 pagesGetting Data from APIs and Web ScrapinggprasadatvuPas encore d'évaluation

- Top Cities and Other Demographics For Data Scientists - Data Science CentralDocument6 pagesTop Cities and Other Demographics For Data Scientists - Data Science CentralgprasadatvuPas encore d'évaluation

- Numpy-User-1 11 0 PDFDocument135 pagesNumpy-User-1 11 0 PDFDavid Corredor RamirezPas encore d'évaluation

- Machine Learning - Google DevelopersDocument47 pagesMachine Learning - Google DevelopersgprasadatvuPas encore d'évaluation

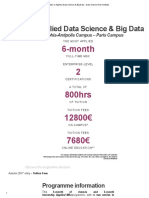

- MSc in Applied Data Science & Big DataDocument8 pagesMSc in Applied Data Science & Big DatagprasadatvuPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)