Vous aimerez peut-être aussi

- 4a Bulk Water Meter Installation in Chamber DrawingPEWSTDAMI004 PDFDocument1 page4a Bulk Water Meter Installation in Chamber DrawingPEWSTDAMI004 PDFRonald ValenciaPas encore d'évaluation

- Sigma Levels CalculationsDocument31 pagesSigma Levels CalculationsPavas Singhal100% (1)

- 381Document8 pages381Nidya Wardah JuhanaPas encore d'évaluation

- D8 9M-2012PVDocument16 pagesD8 9M-2012PVvishesh dharaiya0% (4)

- Powertrain 2020Document42 pagesPowertrain 2020sadananda_pvcPas encore d'évaluation

- Opportunities in The Automotive Industry in EgyptDocument13 pagesOpportunities in The Automotive Industry in EgyptvruddhiPas encore d'évaluation

- Lexus Brand BrochureDocument40 pagesLexus Brand Brochurejammypops100% (1)

- Hyundai 091124091217 Phpapp02Document62 pagesHyundai 091124091217 Phpapp02mbogadhiPas encore d'évaluation

- Anti Take Over StrategiesDocument26 pagesAnti Take Over StrategiesPavas SinghalPas encore d'évaluation

- GEK 116403 Ge File. Performance TestsDocument54 pagesGEK 116403 Ge File. Performance TestsSulaiman JafferyPas encore d'évaluation

- Ashok LeylandDocument20 pagesAshok LeylandAbhishek Rawat67% (3)

- Acma & KPMGDocument28 pagesAcma & KPMGShivanshuPas encore d'évaluation

- Chap007 - Psy Cap - LuthansDocument32 pagesChap007 - Psy Cap - LuthansPavas SinghalPas encore d'évaluation

- Sample Detailed Estimates PDFDocument9 pagesSample Detailed Estimates PDFJj Salazar Dela CruzPas encore d'évaluation

- Practical Project Execution Alloy Wheels Manufacturing PlantDocument5 pagesPractical Project Execution Alloy Wheels Manufacturing PlantSanjay KumarPas encore d'évaluation

- 6.hydraulic Pressure SpesificationDocument3 pages6.hydraulic Pressure SpesificationTLK ChannelPas encore d'évaluation

- Policies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportD'EverandPolicies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportPas encore d'évaluation

- Automobile2006 12523356944579 Phpapp01Document23 pagesAutomobile2006 12523356944579 Phpapp01Ankit AgrawalPas encore d'évaluation

- Business Environment Assignment Submission: Semester-IIDocument13 pagesBusiness Environment Assignment Submission: Semester-IItanmay kalalPas encore d'évaluation

- Automobile MarketDocument3 pagesAutomobile Marketlalit_aglPas encore d'évaluation

- Automobile Industry FinalDocument24 pagesAutomobile Industry FinalanmolPas encore d'évaluation

- DPRDocument5 pagesDPRArjun KhoslaPas encore d'évaluation

- Vehicle Emission StandardsDocument22 pagesVehicle Emission StandardsalagurmPas encore d'évaluation

- Auto ComponentDocument12 pagesAuto ComponentLalsivaraj SangamPas encore d'évaluation

- BMS Auto Platform Automobile Industry-Key Market TrendsDocument8 pagesBMS Auto Platform Automobile Industry-Key Market TrendsMohnish HasrajaniPas encore d'évaluation

- Automobile 2006Document23 pagesAutomobile 2006Krishna ChaitanyaPas encore d'évaluation

- Tata Swot and PestelDocument7 pagesTata Swot and PestelKarthik K Janardhanan50% (2)

- Automobile Industry - Some Economic PoliciesDocument4 pagesAutomobile Industry - Some Economic PoliciesRenu PratapPas encore d'évaluation

- Automobile CommercialVehiclesDocument23 pagesAutomobile CommercialVehiclesPriya MehtaPas encore d'évaluation

- AutomobileDocument17 pagesAutomobileIha BansalPas encore d'évaluation

- Business Analysis of Auto IndusrtyDocument29 pagesBusiness Analysis of Auto IndusrtySaurabh Ambaselkar100% (1)

- Hindustan MotorsDocument57 pagesHindustan MotorsSwathi Velisetty100% (3)

- EU Automotive Investment in IndonesiaDocument16 pagesEU Automotive Investment in IndonesiaOPas encore d'évaluation

- Indian Real Driving Emission Reprort 2021Document40 pagesIndian Real Driving Emission Reprort 2021REX MATTHEWPas encore d'évaluation

- Auto o Neutr Ral: NAP P 2014 T Takes A BowDocument7 pagesAuto o Neutr Ral: NAP P 2014 T Takes A BowbijuePas encore d'évaluation

- ResearchDocument8 pagesResearchMohan DasPas encore d'évaluation

- A Presentation On "Landscape of Automobile Industry Sector": Consulting ClubDocument22 pagesA Presentation On "Landscape of Automobile Industry Sector": Consulting ClubaddyamitPas encore d'évaluation

- Automotive Australia ReportDocument39 pagesAutomotive Australia ReportshahraashidPas encore d'évaluation

- Auto Components SectorDocument23 pagesAuto Components SectorAnand PattabiramanPas encore d'évaluation

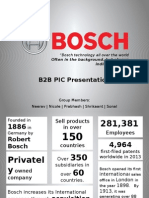

- B2B PIC Presentation: Often in The Background, But Always Indispensable."Document28 pagesB2B PIC Presentation: Often in The Background, But Always Indispensable."KiaraSinghPas encore d'évaluation

- The Automobile Industry in VietnamDocument20 pagesThe Automobile Industry in VietnamxuannamthanhthuyPas encore d'évaluation

- Electric Vehicle ReportDocument9 pagesElectric Vehicle ReportAnurag MishraPas encore d'évaluation

- Next-Generation Vehicle Plan 2010 (Outline)Document3 pagesNext-Generation Vehicle Plan 2010 (Outline)Leping HuangPas encore d'évaluation

- BS IV To BS VI Tata Motors PDFDocument3 pagesBS IV To BS VI Tata Motors PDFKaranPas encore d'évaluation

- LZ LUBEMagFeb2010 EORoleFuelEconomyDocument2 pagesLZ LUBEMagFeb2010 EORoleFuelEconomyMukul AzadPas encore d'évaluation

- Electric VehiclesDocument16 pagesElectric Vehiclesmail mePas encore d'évaluation

- ToyotaDocument27 pagesToyotaEeshal Mirza0% (1)

- Equity Research On Automobile Sector of IndiaDocument15 pagesEquity Research On Automobile Sector of IndiaHitesh Thapar50% (2)

- Chapter-4: Sector-Wise StrategiesDocument24 pagesChapter-4: Sector-Wise StrategiesAyoob AnsariPas encore d'évaluation

- Assignment No 2: Submitted byDocument7 pagesAssignment No 2: Submitted byBadal RathodPas encore d'évaluation

- E-Mobility in INDIA Challenges and Opportunities: Presented by Dr. Vikram KumarDocument90 pagesE-Mobility in INDIA Challenges and Opportunities: Presented by Dr. Vikram KumarBharath Raj100% (1)

- 1.1 Industry ProfileDocument55 pages1.1 Industry ProfileAnas AhmedPas encore d'évaluation

- Industry Analysis - Section C - Group 11Document9 pagesIndustry Analysis - Section C - Group 11Asif ShaikhPas encore d'évaluation

- Operation Strategy of Automobile Industry: - Tata - BajajDocument56 pagesOperation Strategy of Automobile Industry: - Tata - Bajajbaua30Pas encore d'évaluation

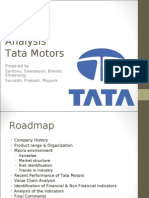

- Financial Analysis Tata Motors: Prepared by Santonu Swastayan Bharat Shreerang Saurabh Prakash MayankDocument35 pagesFinancial Analysis Tata Motors: Prepared by Santonu Swastayan Bharat Shreerang Saurabh Prakash Mayanksen_bitPas encore d'évaluation

- Prashaste - Indian Automotive Industry - 10 JanuaryDocument14 pagesPrashaste - Indian Automotive Industry - 10 JanuaryDeepakPahwaPas encore d'évaluation

- Climatic Change 2. Advances in Renewable Energy 3. Rapid Urbanization 4. Battery Chemistry 5. Energy SecurityDocument46 pagesClimatic Change 2. Advances in Renewable Energy 3. Rapid Urbanization 4. Battery Chemistry 5. Energy Securitymail mePas encore d'évaluation

- Factors Affecting Four Wheeler Industries in IndiaDocument54 pagesFactors Affecting Four Wheeler Industries in IndiaRitesh Vaishnav100% (2)

- Ca MGN 303 LpuDocument6 pagesCa MGN 303 LpuAvinash BeheraPas encore d'évaluation

- Application FOR Recharging Electric VehiclesDocument22 pagesApplication FOR Recharging Electric VehiclesJerry SinghPas encore d'évaluation

- Strategic ManagementDocument23 pagesStrategic ManagementVarun RamzaiPas encore d'évaluation

- Auto Service StationDocument8 pagesAuto Service StationHemanth Kumar RamachandranPas encore d'évaluation

- Project On (Tata Motors)Document61 pagesProject On (Tata Motors)SATYABRAT MAHALIK100% (1)

- Union Budget 2012: Industry, Infrastructure, Agriculture Group No. 3Document23 pagesUnion Budget 2012: Industry, Infrastructure, Agriculture Group No. 3Chetan PatilPas encore d'évaluation

- EV Policies & InitiativesDocument94 pagesEV Policies & InitiativeskhannamoneyPas encore d'évaluation

- Pricing Strategy of Tata NexonDocument4 pagesPricing Strategy of Tata NexonSanJana NahataPas encore d'évaluation

- International Institutes and Trade ImplicationsDocument16 pagesInternational Institutes and Trade ImplicationsangelissssshhhPas encore d'évaluation

- Myanmar Transport Sector Policy NotesD'EverandMyanmar Transport Sector Policy NotesÉvaluation : 3 sur 5 étoiles3/5 (1)

- Definitions: Quality TermsDocument25 pagesDefinitions: Quality TermsPankaj KumarPas encore d'évaluation

- Making Capital Structure DecisionsDocument44 pagesMaking Capital Structure DecisionsPavas SinghalPas encore d'évaluation

- Theory of Capital Structure: How Do We Want To Finance Our Firm's Assets?Document54 pagesTheory of Capital Structure: How Do We Want To Finance Our Firm's Assets?Pavas SinghalPas encore d'évaluation

- Working Capital ManagementDocument34 pagesWorking Capital ManagementPavas SinghalPas encore d'évaluation

- Direct Current Generator ReviewerDocument16 pagesDirect Current Generator ReviewerCaitriona AngelettePas encore d'évaluation

- New Approach For The Measurement of Damping Properties of Materials Using The Oberst BeamDocument6 pagesNew Approach For The Measurement of Damping Properties of Materials Using The Oberst BeamMatnSambuPas encore d'évaluation

- Sand Reclamation - Standard Devices: Shake Out MachinesDocument2 pagesSand Reclamation - Standard Devices: Shake Out MachinesKaarthicNatarajanPas encore d'évaluation

- OpenJDK Vs Oracle JDKDocument2 pagesOpenJDK Vs Oracle JDKkuzzulonePas encore d'évaluation

- TEX20-NV: Technical and Maintenance ManualDocument110 pagesTEX20-NV: Technical and Maintenance Manualvasilikot50% (2)

- Data Structures OutlineDocument5 pagesData Structures Outlineshahzad jalbaniPas encore d'évaluation

- DPP Series 1 PDFDocument1 pageDPP Series 1 PDFsukainaPas encore d'évaluation

- Project Report JamiaDocument76 pagesProject Report JamiaShoaibPas encore d'évaluation

- Weatherford Artificial Lifts Reciprocating Rod Lift OverviewDocument7 pagesWeatherford Artificial Lifts Reciprocating Rod Lift OverviewKentodalPas encore d'évaluation

- IPCR Part 2 2017Document4 pagesIPCR Part 2 2017RommelPas encore d'évaluation

- Communication With Energy Meter and Field Devices Using PLCDocument3 pagesCommunication With Energy Meter and Field Devices Using PLCIJRASETPublicationsPas encore d'évaluation

- CRCCDocument13 pagesCRCCGalih SantanaPas encore d'évaluation

- Solution of Tutorial Sheet-3 (Three Phase Networks) : Ans. Given, - Vab - 45kV, ZL (0.5 + j3), Z (4.5 + j9)Document10 pagesSolution of Tutorial Sheet-3 (Three Phase Networks) : Ans. Given, - Vab - 45kV, ZL (0.5 + j3), Z (4.5 + j9)Shroyon100% (2)

- Kalkhoff Users ManualDocument148 pagesKalkhoff Users Manualanonms_accPas encore d'évaluation

- M403 DatasheetDocument2 pagesM403 DatasheetmichelerenatiPas encore d'évaluation

- KOSO-KI Vector-Disk Stack BrochureDocument11 pagesKOSO-KI Vector-Disk Stack Brochureनिखिल बायवारPas encore d'évaluation

- Fdot Precast Bent Cap Development and Implementation: AbstractDocument10 pagesFdot Precast Bent Cap Development and Implementation: AbstractCongOanh PHANPas encore d'évaluation

- Poly BoreDocument2 pagesPoly BoreMarian OpreaPas encore d'évaluation

- 00 Datasheet of STS-6000K-H1 For 185KTL 20200706Document2 pages00 Datasheet of STS-6000K-H1 For 185KTL 20200706Lindy PortsuPas encore d'évaluation

- Resume For FaisalDocument3 pagesResume For FaisalFaisal Zeineddine100% (1)

- An Introduction To Error-Correcting Codes: The Virtues of RedundancyDocument38 pagesAn Introduction To Error-Correcting Codes: The Virtues of RedundancyKrish Cs20Pas encore d'évaluation

- How To Configure A Wi-Fi Network How To Configure A RADIUS/EAP ServerDocument7 pagesHow To Configure A Wi-Fi Network How To Configure A RADIUS/EAP ServerSeluuunnnPas encore d'évaluation