Vous aimerez peut-être aussi

- Best Practices For Supercritical PlantsDocument490 pagesBest Practices For Supercritical PlantsktsnlPas encore d'évaluation

- Bahrain Waste To Energy PDFDocument6 pagesBahrain Waste To Energy PDFs_kohli2000Pas encore d'évaluation

- CERC's Analysis Solar PV CostDocument3 pagesCERC's Analysis Solar PV Costs_kohli2000Pas encore d'évaluation

- 2 - 4.2 Wileman - Africa RegionDocument10 pages2 - 4.2 Wileman - Africa Regions_kohli2000Pas encore d'évaluation

- Goals SettingDocument11 pagesGoals Settings_kohli2000100% (1)

- Robinhood Case StudyDocument2 pagesRobinhood Case StudyUdaya ChoudaryPas encore d'évaluation

- Power Sector Development in MyanmarDocument27 pagesPower Sector Development in Myanmars_kohli20000% (1)

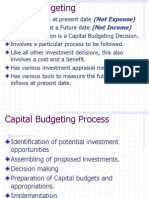

- Cash Outflow Cash Inflow: (Not Expense) (Not Income)Document15 pagesCash Outflow Cash Inflow: (Not Expense) (Not Income)s_kohli2000Pas encore d'évaluation

- Power Sector Retreat Presentations - Jan 20-21 2012 - NNPC GasDocument29 pagesPower Sector Retreat Presentations - Jan 20-21 2012 - NNPC Gass_kohli2000Pas encore d'évaluation

- Asia Pacific Partnership India Peer Review ParticipantsListDocument9 pagesAsia Pacific Partnership India Peer Review ParticipantsLists_kohli2000Pas encore d'évaluation

- Power Projects Seeking Gas AllocationDocument3 pagesPower Projects Seeking Gas Allocations_kohli2000Pas encore d'évaluation

- Top Plant: Amman East Power Plant, Al Manakher, Jordan: Owner/operator: AES Jordan PSCDocument3 pagesTop Plant: Amman East Power Plant, Al Manakher, Jordan: Owner/operator: AES Jordan PSCs_kohli2000Pas encore d'évaluation

- Upcoming GTPP / CCPP Opportunities For LIG & LII: Ason15 June 2009Document1 pageUpcoming GTPP / CCPP Opportunities For LIG & LII: Ason15 June 2009s_kohli2000Pas encore d'évaluation

- SEC Projects 2010 - 2018Document1 pageSEC Projects 2010 - 2018s_kohli2000100% (1)

- Japanese Companies in IndiaDocument18 pagesJapanese Companies in Indias_kohli2000Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- 2017 Directory of China's Natural Gas Pipelines PDFDocument12 pages2017 Directory of China's Natural Gas Pipelines PDFarapublicationPas encore d'évaluation

- The World Of: ADDINOL - Get Only Our Best! German Engine Oils Hit The Mark in RussiaDocument6 pagesThe World Of: ADDINOL - Get Only Our Best! German Engine Oils Hit The Mark in RussiaAna-Maria AncutaPas encore d'évaluation

- Pge 2017 Presentation Hydrogen Co Firing Larfeldt SiemensDocument13 pagesPge 2017 Presentation Hydrogen Co Firing Larfeldt SiemensAbd Elrahman UossefPas encore d'évaluation

- Applied Chemistry - Lecture 7Document57 pagesApplied Chemistry - Lecture 7Muhammad HusnainPas encore d'évaluation

- MWIDocument19 pagesMWIMehulkumar PatelPas encore d'évaluation

- Oxygen Plant Safety PrinciplesDocument10 pagesOxygen Plant Safety Principleshwang2Pas encore d'évaluation

- EGR With CO2 SequestrationDocument29 pagesEGR With CO2 SequestrationInnobaPlusPas encore d'évaluation

- Sensor Specifications and Cross-SensitivitiesDocument35 pagesSensor Specifications and Cross-SensitivitiesAndrew MillerPas encore d'évaluation

- Material Balance Project Styrene Manufacture: H CHCH H C CH CH H CDocument4 pagesMaterial Balance Project Styrene Manufacture: H CHCH H C CH CH H CMhd SakerPas encore d'évaluation

- LNG Process TrainDocument23 pagesLNG Process TrainMuhammad Shariq Khan100% (11)

- 0653 w15 Ms 33Document6 pages0653 w15 Ms 33yuke kristinaPas encore d'évaluation

- PPIS Annual 2020 21 Final CompressedDocument94 pagesPPIS Annual 2020 21 Final CompressedBilalPas encore d'évaluation

- Term Paper On Hydrogen Fuel A New HopeDocument15 pagesTerm Paper On Hydrogen Fuel A New Hopeprashant_cool_4uPas encore d'évaluation

- Chemical Process CalculationsDocument9 pagesChemical Process CalculationsYolandaPas encore d'évaluation

- Benefits of Integrating NGL Extraction and LNG RecoveryDocument8 pagesBenefits of Integrating NGL Extraction and LNG RecoveryEdgar HuancaPas encore d'évaluation

- Hollow Fiber MenbranesDocument15 pagesHollow Fiber MenbranespikipelukiPas encore d'évaluation

- Carbon Footprint of Poultry Production FarmsDocument7 pagesCarbon Footprint of Poultry Production FarmssanielPas encore d'évaluation

- CH215 Industrial Organic Chemistry II 24-12-2021Document229 pagesCH215 Industrial Organic Chemistry II 24-12-2021Fortune VushePas encore d'évaluation

- First Natcomindnc1Document292 pagesFirst Natcomindnc1lakshmeiyPas encore d'évaluation

- 2020 CHEE2001 Week 6 Tutorial SheetDocument2 pages2020 CHEE2001 Week 6 Tutorial SheetMuntaha ManzoorPas encore d'évaluation

- Paper 294326Document22 pagesPaper 294326kirandevi1981Pas encore d'évaluation

- Ayhan DemirbasDocument8 pagesAyhan DemirbasLalta PrasadPas encore d'évaluation

- Fossil FuelDocument44 pagesFossil FuelZay SalazarPas encore d'évaluation

- Space: Station ResistojetsDocument9 pagesSpace: Station ResistojetsAbhishek DadhwalPas encore d'évaluation

- About e WalletDocument22 pagesAbout e WalletsudheerPas encore d'évaluation

- CO2 Reforming of MethaneDocument8 pagesCO2 Reforming of Methanesorincarmen88Pas encore d'évaluation

- Detection Gas ListDocument1 pageDetection Gas ListZornica GospodinovaPas encore d'évaluation

- Dimensionless Steady-State Nsod Model: Carlo GualtieriDocument8 pagesDimensionless Steady-State Nsod Model: Carlo GualtieriPavel NevedPas encore d'évaluation

- Air Pollution Is The Introduction Of: Particulates Biological Molecules Earth's Atmosphere Natural Built EnvironmentDocument7 pagesAir Pollution Is The Introduction Of: Particulates Biological Molecules Earth's Atmosphere Natural Built EnvironmentAna Marie Besa Battung-ZalunPas encore d'évaluation

- 5 - Estimation - of - Greenhouse - Gas - Emissions - by - Household Energy - Consumption - Lahore - Pakistan PDFDocument19 pages5 - Estimation - of - Greenhouse - Gas - Emissions - by - Household Energy - Consumption - Lahore - Pakistan PDFSalman ShujaPas encore d'évaluation